The hidden cost of working harder

There is a belief baked into American culture that the number of hours worked is the primary indicator of success and ambition. Tech titans brag about 120-hour weeks. Corporate managers reward employees who stay the latest. Entrepreneurs are told they must grind until the work is done. This mindset, however well-intentioned, contains a fatal flaw: it assumes a direct, unlimited relationship between hours and output — and the data says otherwise.

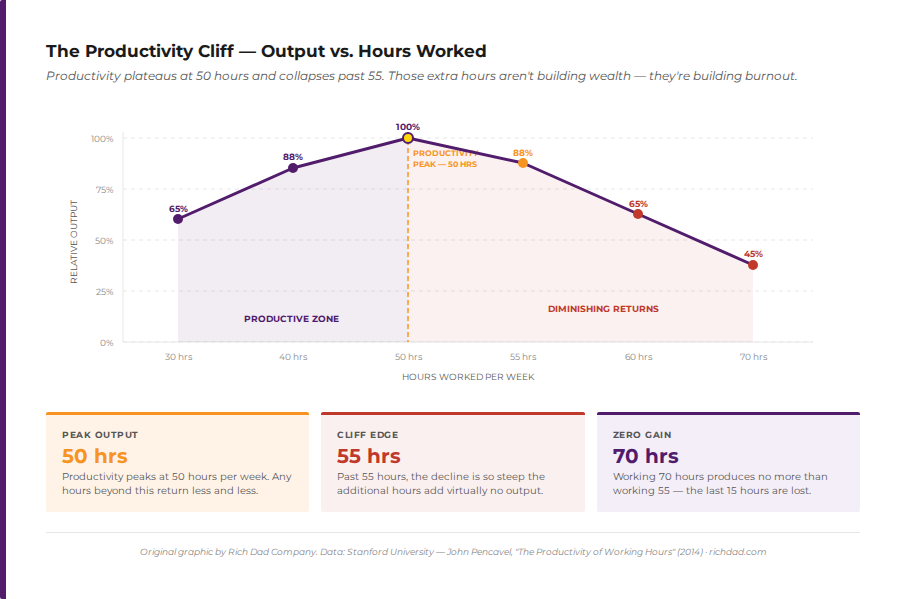

Researchers at Stanford University found that productivity falls sharply after 50 hours per week, and the decline becomes so steep past 55 hours that additional time produces virtually no additional output. An employee working 70 hours per week achieves roughly the same measurable output as one working 55. The last 15 hours are, statistically speaking, wasted. And those wasted hours carry a cost that goes beyond lost time: the World Health Organization links working 55+ hours per week to a 35% higher risk of stroke and a 17% higher risk of dying from heart disease compared to a standard workweek.

The richer insight, however, isn’t about what happens to productivity at 70 hours. It’s what doesn’t happen to wealth when time is the only tool being leveraged. No matter how many hours someone works, the income ceiling remains fixed at hours × wage. That ceiling is the rat race itself.

The real meaning of “work smarter, not harder”

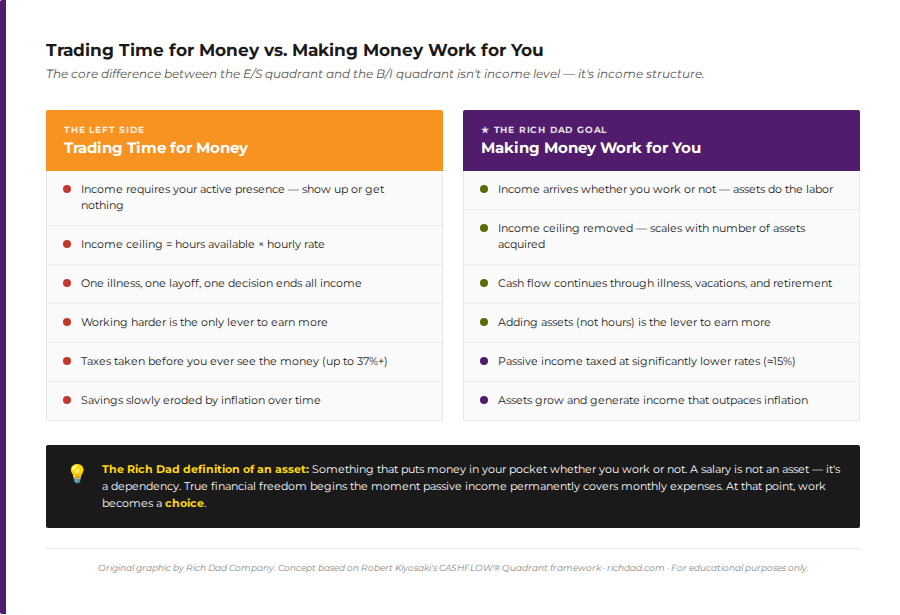

Most productivity advice interprets “work smarter” as a collection of workflow optimizations: prioritize tasks, batch your email, use the Pomodoro method. These tools are useful, but they don’t change the fundamental structure of how income is earned. A more efficient employee is still an employee. A more organized self-employed professional still stops earning the moment they stop working.

Robert Kiyosaki’s definition of working smarter is structural, not tactical. It appears throughout Rich Dad Poor Dad and the CASHFLOW Quadrant framework: true intelligence in wealth-building means moving income off the left side of the quadrant — where income is earned by trading time — and onto the right side, where income is generated by assets and systems.

The CASHFLOW Quadrant divides economic activity into four categories: Employee (E), Self-Employed (S), Business Owner (B), and Investor (I). The left side — E and S — is where most people spend their lives. The right side — B and I — is where financial freedom lives.The hidden cost of working harder

What happens to your income when you stop working?

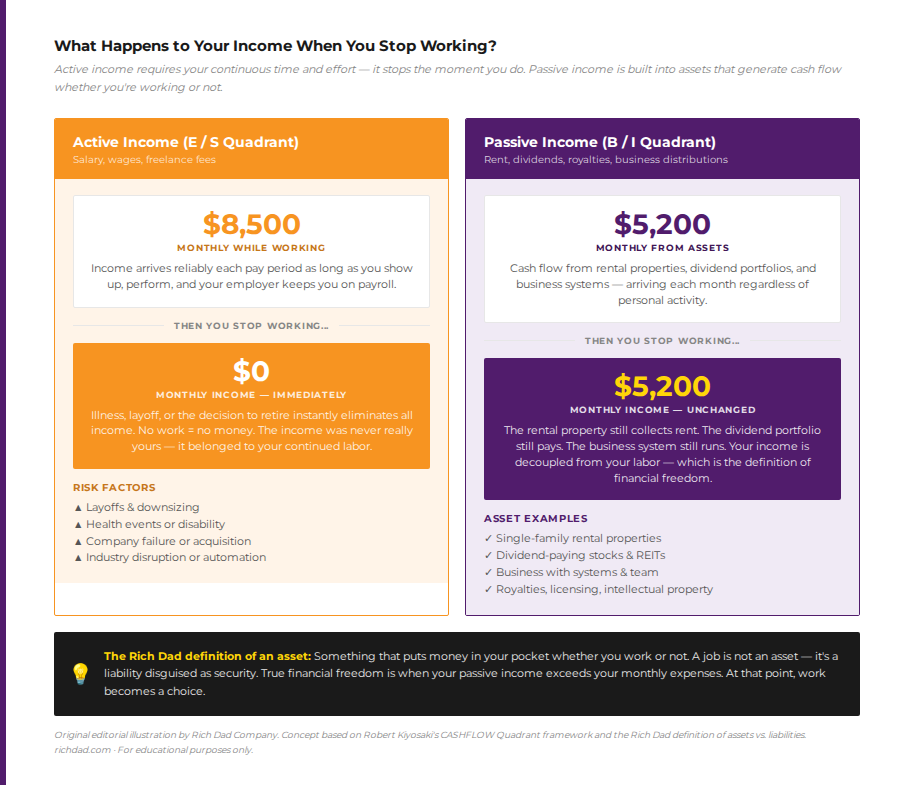

This is the question Robert argues everyone should ask themselves — and most people don’t like the answer. For the vast majority of Americans who depend on a salary or freelance work, income has a single point of failure: their own continued presence. A layoff, a health event, a disability, or simply the decision to retire eliminates all income immediately. As the “What Happens to Your Income When You Stop Working?” framework illustrates, the left-side worker who earns $8,500 per month goes to $0 the moment they stop. The investor who built $5,200 per month in passive income from rental properties, dividend portfolios, and business distributions continues receiving that income unchanged.

Working smarter, in this light, isn’t about doing fewer tasks. It’s about building an income structure that isn’t dependent on your daily effort. Every rental property acquired, every dividend-paying asset purchased, and every scalable business system built permanently extends the separation between your labor and your income — until the two are fully decoupled. That decoupling is the definition of financial freedom.The hidden cost of working harder

The 4 financial levers that replace hard work with smart work

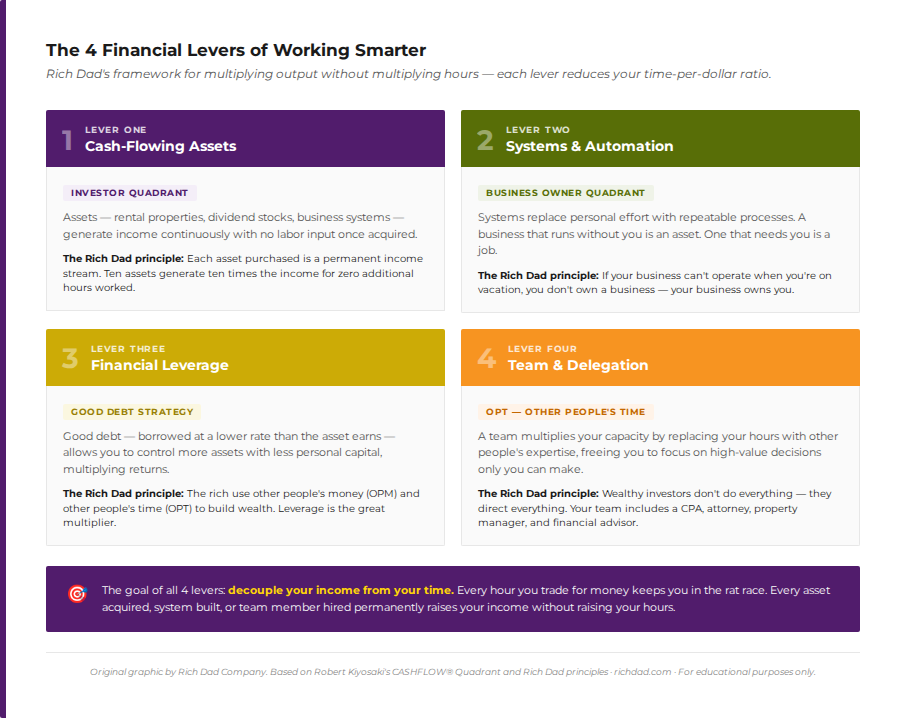

Translating the philosophy into practice requires understanding the four structural levers that allow income to grow independently of hours worked. These aren’t productivity hacks — they are the mechanisms wealthy investors use to compound returns without compounding effort.What happens to your income when you stop working?

Lever 1: Cash-flowing assets

The most direct form of working smarter is purchasing assets that generate income continuously. Real estate — particularly rental properties — is the cornerstone of this approach for Rich Dad. A single-family rental generates monthly cash flow every month, whether the owner works or rests. Dividend-paying stocks and paper assets provide another stream. Each asset acquired is a permanent, compounding income source added to the portfolio without requiring additional hours. Ten assets generate ten times the passive income for zero additional hours — which is the mathematical opposite of working harder.

Lever 2: Systems and automation

Robert’s rich dad made a clear distinction between the Self-Employed (S) quadrant and the Business Owner (B) quadrant: the self-employed person owns a job, and the business owner owns a system. A business that can operate without its owner’s daily presence is an asset. A business that collapses without the owner is a highly stressful, time-consuming job with no cap on the hours required. Systems — documented processes, automated workflows, trained teams, scalable delivery models — are what elevate a self-employed person to a true business owner.

The same principle applies to investing. An investor who manually manages every decision is still trading time. The investor who builds a systematized portfolio — automatic rebalancing, property management teams, financial advisors handling execution — has created a machine that works independently.

Lever 3: Financial leverage

There is a critical distinction between good debt and bad debt. Bad debt finances consumption — it costs money each month and builds no equity. Good debt finances assets that generate more income than the debt costs. A mortgage on a rental property that yields $450/month in net cash flow after all debt service is good debt — it allows the investor to control a $200,000 asset with $40,000 down, multiplying their return on invested capital without working additional hours.

Leverage is the financial equivalent of a lever in physics: a small force applied at the right point moves a much larger weight. The wealthy use other people’s money (OPM) to acquire income-producing assets far beyond what their own capital could purchase. This is a concept the traditional financial system rarely teaches, but one that defines the difference between the B/I quadrant and the E/S quadrant.

Lever 4: Team and delegation

Robert often says that sophisticated investors don’t do it alone — they build teams. A CPA who understands tax strategy, a real estate attorney who protects assets, a property manager who handles tenant relationships, and a financial advisor who executes investment decisions are not overhead expenses. They are leverage. Each team member multiplies the investor’s effective hours by handling execution while the investor focuses on strategy — the highest-value work only they can do.

This is why trying to do everything independently, whether in business or investing, is a form of working harder, not smarter. The ego-driven business owner who insists on being in every decision creates a ceiling: one person’s capacity. The team-leveraged investor multiplies capacity without multiplying hours.

Time is the scarcest resource — treat it like one

One of the most persistent traps in the E/S quadrant is the illusion of busy-ness. People who feel overextended rarely believe they have time to build passive income streams — and that perception keeps them exactly where they are. The excuse “I don’t have the time” almost always translates to “I haven’t made this a priority.” Priorities are chosen, not found.

Tim Ferriss, author of The 4-Hour Workweek, captured this in a conversation on the Rich Dad Radio Show: “How do you 10x your hourly output? That’s the question… You don’t have to work four hours a week, but the objective is always: how much can I get out of my hours?” The wealthy investor doesn’t ask how many hours to put in. They ask how to make each hour produce permanent, compounding returns — and then build the systems and assets that do exactly that.

The practical starting point is an honest audit of how time is currently allocated. Which hours generate active income that stops when work stops? Which hours — if redirected — could be invested in learning financial education, evaluating real estate deals, building business systems, or acquiring income-generating assets? Every hour redirected from the first category to the second permanently shifts the trajectory of wealth.

How to stop trading time for money: A practical starting framework

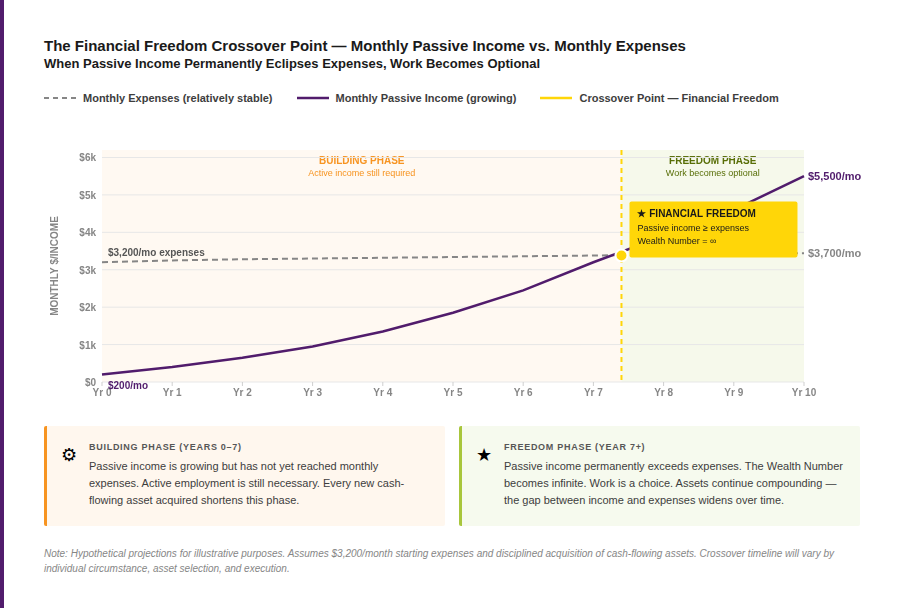

The transition from the left side of the CASHFLOW Quadrant to the right doesn’t happen overnight, and it doesn’t require quitting a job tomorrow. What it requires is beginning to allocate a portion of income and time toward assets and financial education consistently. The crossover point — where passive income permanently exceeds monthly expenses — is the moment work becomes optional. Getting there is a process, not an event.

Step 1: Audit your income mix

Add up all income from the last month. What percentage came from active labor — salary, freelance, consulting? What percentage came from assets — rent, dividends, royalties, business distributions? Most people will find they are 95–100% dependent on earned income. That number is the income mix target to reduce over time by systematically building passive income streams.

Step 2: Redirect a portion of each paycheck to assets

Before spending, before saving, redirect a percentage of each paycheck into income-producing assets. This doesn’t require a large initial sum. The principle is consistency: every dollar deployed into a cash-flowing asset permanently raises the passive income base. Dividend reinvestment, real estate down payment funds, and business investment all qualify. The key is that the money must go to work — not sit in a savings account losing to inflation.

Step 3: Invest in financial education first

Robert Kiyosaki is consistent on one point above all others: uneducated investing is risky; educated investing controls risk. Before deploying capital into real estate, stocks, or any other asset class, invest time in financial education. Learn the fundamentals of the asset class. Understand the tax implications. Build the advisory team. Financial intelligence — the ability to evaluate opportunities, manage risk, and structure investments tax-efficiently — is the highest-return investment available and the one most people skip entirely.

Working smarter, at its core, is about replacing labor with knowledge, systems, and capital. The hours spent in financial education today are the hours that eliminate labor requirements tomorrow. That compounding effect is what separates the wealthy from the overworked.

Why hustle culture is a poor mindset for building wealth

Hustle culture — the gospel of 80-hour weeks, 5 a.m. alarms, and perpetual grind — is not a wealth strategy. It is a labor strategy. The person working 80 hours per week is still selling time. The value of their time may be higher than someone working 40 hours, but the fundamental structure — trading hours for income — is identical. When those hours stop, the income stops.

There is nothing inherently wrong with working hard. In fact, building passive income streams and systems often requires substantial effort in the early stages. The critical distinction is the goal: are those hard hours building assets and systems that will eventually work independently, or are they simply producing more active income that vanishes when you take a day off? Working hard toward the right structure — toward the B and I quadrant — is smart work. Working hard to generate more earned income indefinitely is the rat race by another name.

The fear that drives overwork — fear of falling behind, fear of being seen as unproductive, fear that the business or career will collapse without constant attention — is worth examining honestly. Tim Ferriss’s “Fear Setting” exercise, discussed on the Rich Dad Radio Show, is a useful tool: write down every fear associated with stepping back, then identify what could go wrong, how to minimize each risk, and how to recover if it happens. Most people find their fears are far more imagined than real — and that the real risk is continuing to trade all of their time for income that stops the moment they do.

The smartest work is building systems that work without you

Working smarter, not harder, is not a productivity tip. It is a complete restructuring of how income is generated and how time is valued. The employee who works 70 hours per week and the investor who works 30 hours per week may have similar gross incomes — but the investor’s income compounds. It grows while they sleep, while they travel, and after they stop working entirely. The employee’s income stops the moment the relationship with the employer changes.

This path is not easy, and it is not fast. Building the financial education, acquiring the first assets, building the systems, and assembling the team takes time and discipline. But every step in that direction — every hour redirected from generating active income to building passive income — permanently improves the ratio of income to labor. That is the compounding power of working smarter.

Begin with the CASHFLOW Quadrant as a map. Identify which quadrant currently generates income. Then identify which quadrant to move toward. Every decision — where to invest, how to structure a business, whether to take on debt — should be evaluated through the lens of that goal. The question is never “how many hours am I willing to work?” The question is “how do I make the hours I work permanent?”

FAQs

Working smarter means shifting income from active sources — where you trade your time for money — to passive sources, where assets and systems generate income independently. It’s not about working fewer hours but about ensuring that the hours worked build structures that produce permanent, compounding returns rather than temporary earned income.

The CASHFLOW Quadrant divides income sources into four types: Employee (E), Self-Employed (S), Business Owner (B), and Investor (I). The left side — E and S — requires active labor for every dollar earned. The right side — B and I — generates income through systems and assets that work independently. Moving from the left to the right side is the structural definition of working smarter.

Rich Dad prioritizes real estate for cash flow and tax advantages, followed by dividend-paying stocks and paper assets, and scalable businesses with strong systems. Physical precious metals like gold and silver serve as wealth preservation rather than cash flow. The best asset is one the investor understands well enough to evaluate risk — which is why financial education precedes any investment decision.

Research consistently shows that more than 50% of U.S. workers log more than 40 hours per week, averaging closer to 46 hours. Stanford research demonstrates that productivity peaks at 50 hours and collapses past 55 — meaning that a substantial portion of those extra hours produces no measurable additional output.

The starting point is redirecting a consistent percentage of earned income into assets before any discretionary spending. Dividend reinvestment, REITs, and small-scale rental properties are accessible entry points. The more important investment, initially, is financial education — understanding how to evaluate assets, manage risk, and structure investments tax-efficiently before deploying capital.

Yes. The transition from the E quadrant to the B and I quadrant happens incrementally for most people. The starting point is using earned income — while still employed — to systematically build passive income streams. Each asset acquired reduces the percentage of income dependent on employment. The goal is reaching the crossover point where passive income exceeds monthly expenses, at which point employment becomes optional rather than required.