Why Most People Only Ever Learn One Type of Income

When Robert Kiyosaki was a child, he spent hours playing Monopoly® with his rich dad, trading four green houses for one red hotel. Buried inside that simple formula was a lesson Robert carried into adulthood: the value of cash flow. Monopoly® teaches players to buy an asset, collect rent, and reinvest the proceeds into bigger assets — the exact mechanics behind passive income in the real world.

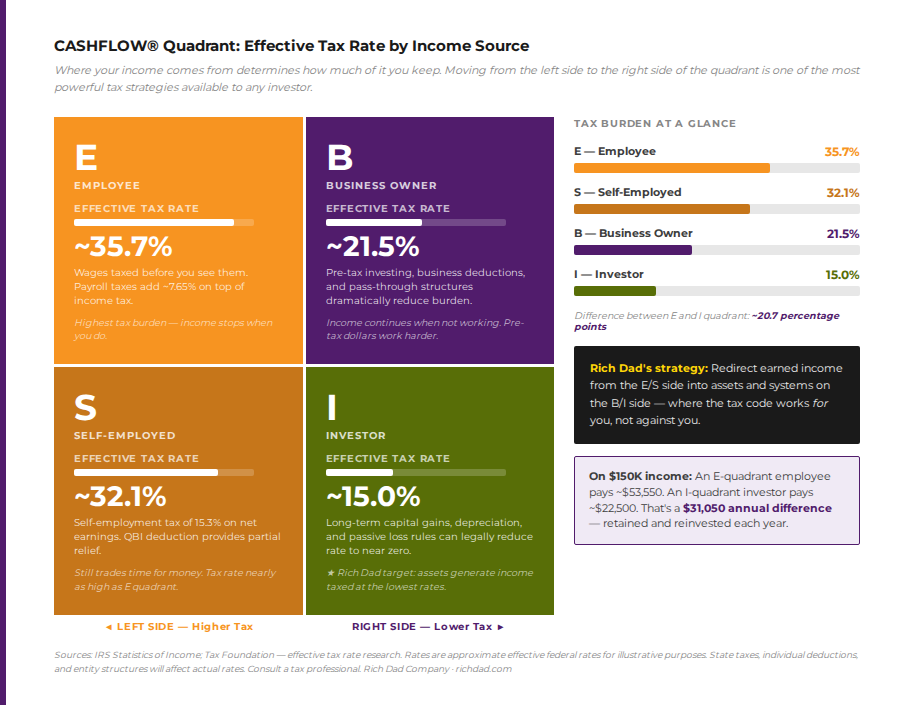

Most people never receive that lesson. Traditional schooling teaches people to get a job, and most financial advice stops there. But a job produces only one of three possible types of income, and it happens to be the one taxed the hardest and the one most exposed to layoffs, automation, and economic downturns. Building real financial education starts with understanding that earned income, portfolio income, and passive income are not interchangeable — they carry different risks, different tax treatment, and different long-term ceilings. The CASHFLOW® Quadrant is the simplest way to see how the shift works: Employees (E) and Self-employed (S) people earn active income on the left side, while Business owners (B) and Investors (I) build wealth through income that doesn’t require their direct labor.

Error: Campaign not found.

The First Type of Income: Earned Income

What Counts as Earned Income

If a person has a job and receives a paycheck, they’re making money through earned income — also called active income. A web designer, a grocery store cashier, and a small business owner who works in their own shop are all trading a set amount of time (Y) for a set amount of money (X). In the United States, that exchange rate is negotiated between employee and employer, and the standard unit of time is the 40-hour work week.

Why Earned Income Is the Riskiest Wealth-Building Tool

Earned income is simple, which is exactly why it appeals to people with a low financial IQ: do the job, get paid. In a stable economy, it feels secure, and a strong performance often earns a raise. But that sense of security is largely an illusion. If the economy contracts or a company is mismanaged, a job can disappear overnight — something millions of workers learned the hard way during recent economic shocks, and many of those positions never came back. For most employees and self-employed workers, earned income covers monthly expenses with little left to invest, which is why so many people live paycheck to paycheck no matter how much they earn. And on top of the risk, earned income is taxed at the highest rate of the three types of income — a cost most people never stop to calculate.

The Second Type of Income: Portfolio Income

How Portfolio Income Is Made

Where earned income comes from trading time for money, portfolio income comes from capital gains — buying an asset at one price and selling it at a higher one. Someone who buys a stock at $10 and sells it at $40 has captured a $30 capital gain. House flipping works the same way: buy a run-down property, invest in improvements, and hope the market allows a profitable sale. Both are classic examples of portfolio income, and both depend entirely on price movement rather than ongoing cash flow.

Why Portfolio Income Is a Bet, Not a Strategy

Portfolio income can produce fast, dramatic gains when the market is hot, which is part of why it’s so tempting. But it’s also speculation, and speculation without financial education is gambling with better math. Investors who buy in late — after a price has already been driven up by momentum or hype — can be badly burned once the trade reverses, as many retail traders learned firsthand during the 2021 GameStop frenzy, when plenty of latecomers absorbed steep losses once the price collapsed. Portfolio income is also tied to the broader economy: many house flippers who were mid-renovation when the 2008 housing market collapsed couldn’t sell fast enough to avoid losses, since real estate is a comparatively illiquid asset. And despite the risk, portfolio income still doesn’t enjoy the lowest tax treatment of the three — that distinction belongs to passive income.

Error: Campaign not found.

The Third Type of Income: Passive Income

What Makes an Asset “Passive”

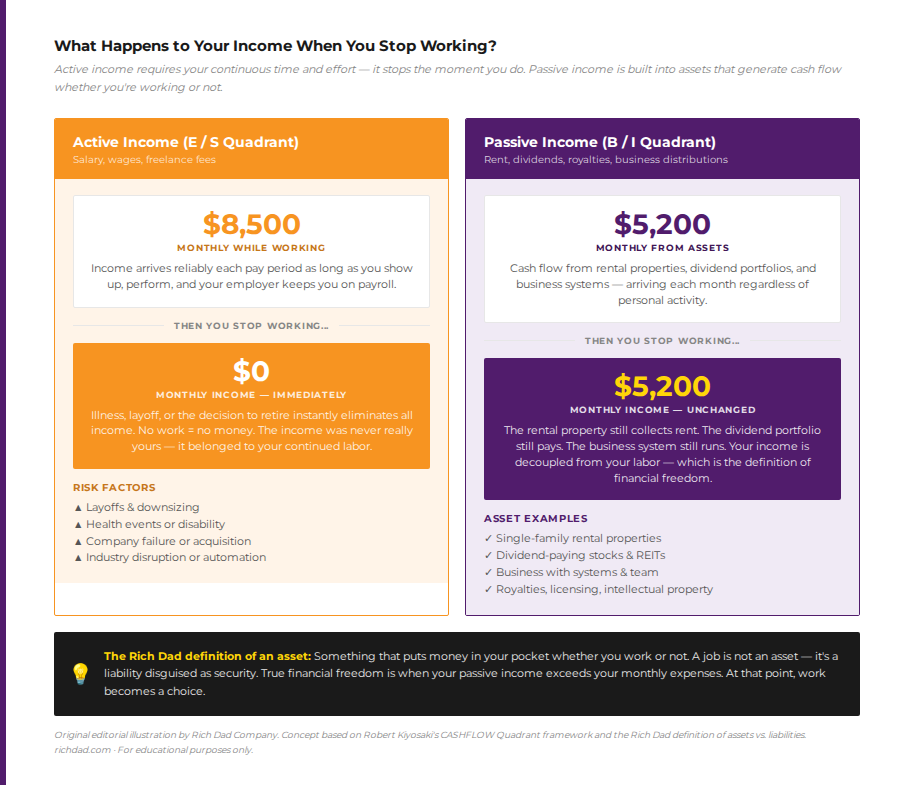

Rich dad’s own formula — four green houses, one red hotel — describes exactly how passive income works. Referencing the CASHFLOW Quadrant again, Business owners (B) and Investors (I) on the right side make money by acquiring assets that produce consistent cash flow. In Rich Dad Poor Dad, Robert Kiyosaki defines an asset simply: something that puts money in your pocket whether you work or not. Rental properties that pay monthly rent, a profitable business, or a book or game that pays ongoing royalties are all textbook examples.

Why the Tax Code Rewards Passive Income

The best advantage of passive income is that it keeps paying whether the owner is working or not — freeing up time to acquire more cash-flowing assets. Profits from one asset can be reinvested into the next without ever giving up the original, creating a compounding effect that neither earned nor portfolio income can match. And remarkably, passive income is taxed the lightest of the three. It almost seems like the tax code wants people to invest this way — and in a sense, it does, since business owners and investors create the jobs and housing the economy depends on.

It takes a high financial IQ and patience to invest successfully for passive income — two things most people were never taught. Most people were told to get a secure job, invest for the long term in a diversified portfolio, and treat their home as an asset. That last belief cracked in 2008, when homeowners across the country watched home values collapse almost overnight and realized their house wasn’t an asset at all — it was a liability, since it took money out of their pocket every month in the form of a mortgage, taxes, and upkeep, rather than putting money in.

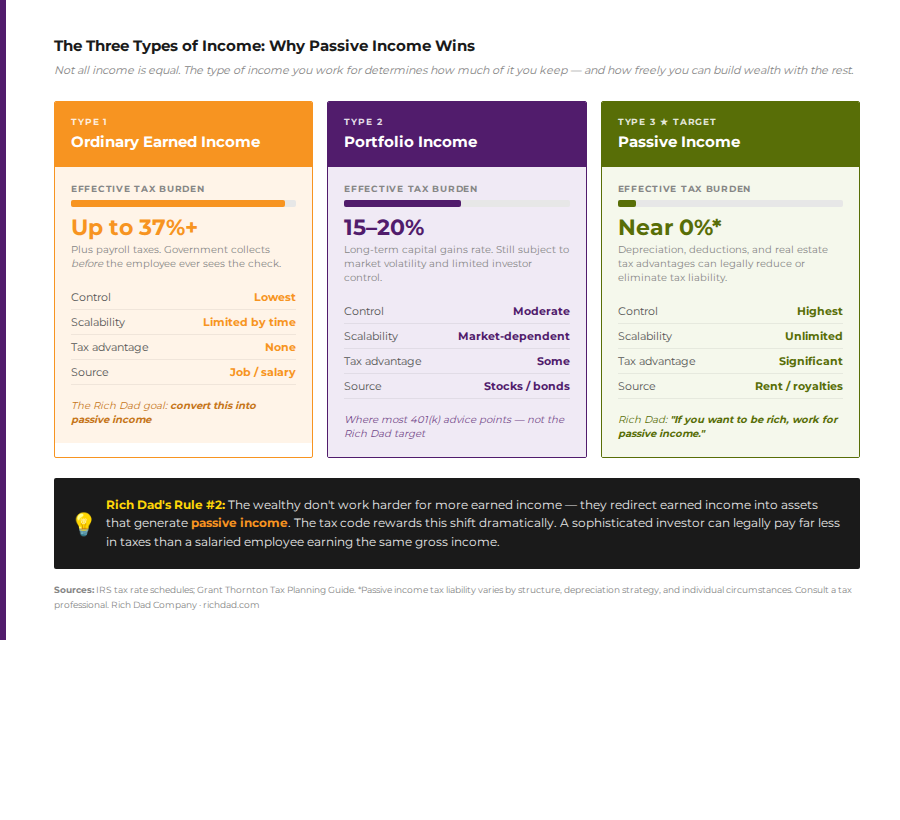

How Taxes Treat the 3 Types of Income Differently

Taxes are the single biggest expense for most people, and it’s not the mortgage, the car payment, or the credit card bill that costs Employees and the Self-employed the most — it’s the tax bill itself. Ordinary earned income is taxed at the highest federal rates, currently topping out at 37% before payroll taxes are even added on. Portfolio income fares somewhat better: long-term capital gains and qualified dividends are taxed at preferential rates, generally capped well below ordinary income rates. So, using the earlier example, buying 1,000 shares at $10 and selling at $40 produces a $30,000 profit — but roughly 20% goes to capital gains tax, leaving $24,000.

Passive income sits in a different category altogether. Depreciation, real estate deductions, and pass-through business structures allow investors and business owners to legally reduce their effective tax rate far below what an employee pays on the same gross income — a gap confirmed by IRS data on effective tax rates by income source and by independent analysis from the Tax Foundation. This isn’t a loophole; it’s a deliberate incentive built into the tax code to reward the people who create jobs and housing.

Once a person invests in their financial education and starts earning passive income, they’re not just learning to make money without a job — they’re keeping more of every dollar they make.

What Happens to Each Type of Income When You Stop Working

The clearest way to see the difference between the three types of income is to ask a simple question: what happens the day someone stops working? Earned income answers immediately — it stops. No shift, no paycheck. Portfolio income depends on timing and market conditions; there’s no guarantee a position can be sold favorably the moment it’s needed. Passive income is built to answer differently: rent still gets collected, dividends still get paid, and business systems still run, whether or not the owner shows up.

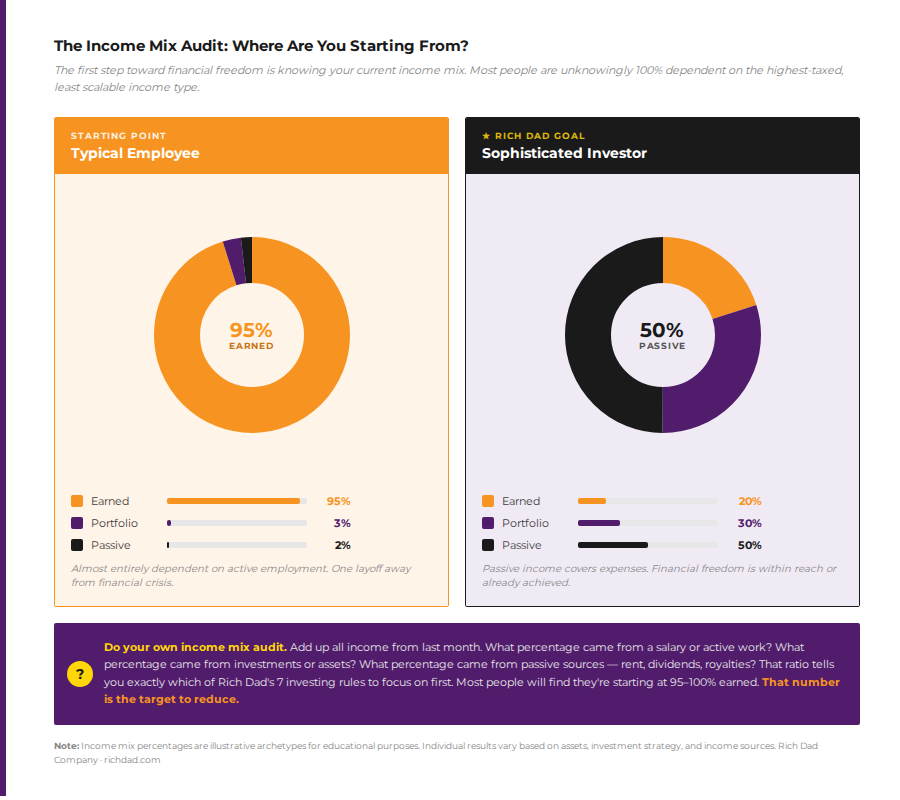

Auditing Your Own Income Mix

Most people have never actually calculated their own income mix — the percentage of last month’s money that came from a paycheck versus an investment versus a cash-flowing asset. It’s a five-minute exercise with an uncomfortable result for most: the overwhelming majority of people are close to 100% dependent on earned income, which means they’re one layoff away from a financial crisis and paying the government’s highest tax rate on every dollar they bring in.

Running this audit isn’t about judgment — it’s about a baseline. Add up every dollar that came in over the last month, then sort it into the three buckets. That single number becomes the starting point for a plan, and it’s usually the clearest argument for why building real estate or business income matters more than chasing another raise.

Moving From Earned Income Toward Passive Income

The purpose of understanding the three types of income isn’t to declare one morally superior — earned income pays the bills while a person builds toward something bigger, and portfolio income has its place for investors with real market expertise. But for anyone working toward financial freedom, the goal is the same: reduce dependence on the highest-taxed, least scalable income source, and increase the share of income that keeps flowing whether or not they’re working.

That shift usually starts small: acquiring a single rental property, starting a side business, or learning to evaluate dividend-paying stocks for cash flow rather than short-term price swings. It also starts with practice. One low-risk way to build the instincts investors need is to play CASHFLOW® Classic for free and pay attention to the choices made along the way — are small, safe deals (green houses) more appealing, or is the goal to swing for bigger plays (red hotels)? The answer often points toward which type of income is worth pursuing first.

Error: Campaign not found.

Conclusion

Earned, portfolio, and passive income all provide cash flow, but they are not created equal — in risk, in reliability, or in how the tax code treats them. Earned income is the easiest to start and the most fragile. Portfolio income can create fast gains but carries real speculative risk. Passive income takes the most financial education to acquire but is the only one of the three designed to outlast the work that created it. Understanding the difference is the foundation every other Rich Dad strategy builds on.

FAQs

The three types of income are earned income (wages and salaries from a job), portfolio income (capital gains from buying and selling assets like stocks or property), and passive income (ongoing cash flow from assets such as rental real estate, royalties, or a business that runs without the owner’s daily involvement).

Passive income generally carries the lowest effective tax rate of the three, thanks to depreciation, real estate deductions, and pass-through business structures built into the tax code. Earned income is typically taxed the highest, and portfolio income falls in between at preferential capital gains rates.

Not entirely — most passive income sources require real effort and financial education to set up, whether that means researching a rental market, vetting a business partner, or learning how a dividend-paying company generates its cash flow. The “passive” part refers to the income continuing to arrive without ongoing labor once the asset is in place, not to the process of acquiring it.

Yes. A landlord who actively manages tenants and repairs may be generating income that behaves more like earned income, while the same rental held with a property manager can function as passive income. The line often depends on how involved the owner remains in the day-to-day operation.

Most people start with a single cash-flowing asset — a rental property, a dividend-paying stock position, or a small business system — funded by redirecting a portion of earned income. The bigger first step is usually education: learning to evaluate an asset’s cash flow before acquiring it, rather than speculating on price appreciation alone.