The numbers don’t lie: Employment is the riskiest position

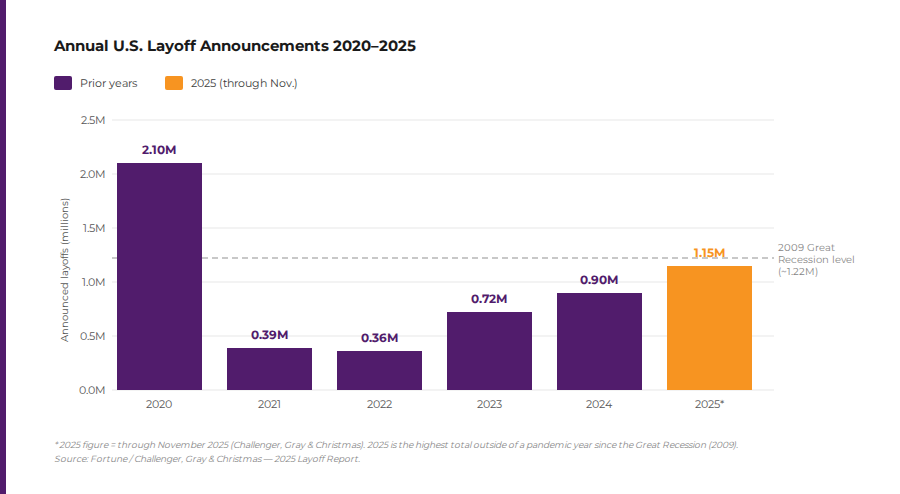

The emotional appeal of job security is understandable. Consistent paychecks, employer benefits, and the appearance of stability make employment feel safe. But the data tells a different story. In 2025, U.S. layoff announcements tracked by Challenger, Gray & Christmas exceeded 1.15 million through November — approaching levels not seen outside a pandemic year since the 2009 Great Recession. Amazon, UPS, General Motors, and Paramount were among the major employers eliminating tens of thousands of positions.

A 2025 survey by Clarify Capital found that one in three Americans carries significant “layoff anxiety” — even among workers who describe themselves as currently secure. Nearly a third said they’d accept a 10–20% pay cut just to reduce the probability of being let go. That is not a population that feels safe. That is a population in a state of chronic financial precarity, dressed up in the language of a stable career.No raises for you

The Bureau of Labor Statistics reports the median employee tenure at just 3.9 years. This is what “job security” actually means in practice: a temporary arrangement that changes hands, on average, every four years. Building a financial future on that foundation is structurally unsound.

AI is accelerating the end of employment-based security

Automation and artificial intelligence have long been discussed as future threats to employment. They are now present-tense realities. According to the World Economic Forum’s 2025 Future of Jobs Report, 41% of employers worldwide intend to reduce their workforces in the next five years due to AI automation — and the same report notes that many have already begun. Since 2023, employers have explicitly attributed more than 70,000 U.S. job cuts to AI adoption.

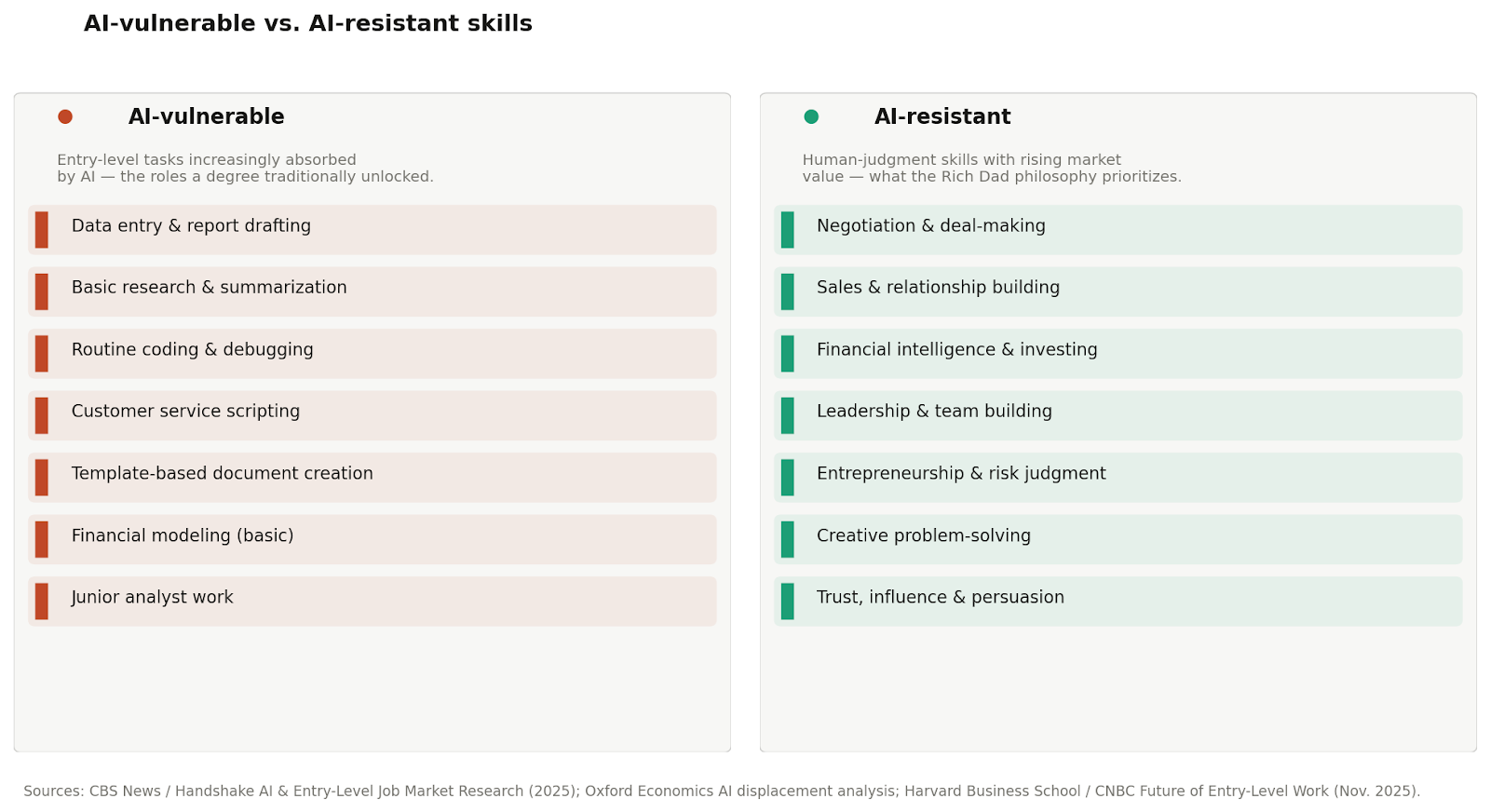

The disruption is not limited to factory floors and call centers. Bloomberg research indicates AI could replace 53% of market research analyst tasks and 67% of sales representative tasks. Anthropic CEO Dario Amodei has projected that AI could eliminate half of all entry-level white-collar jobs within five years. These are roles that college graduates were explicitly told to pursue for stability.

This accelerates the long argued, and undeniable timeline: the skills that make someone a valuable employee are increasingly the skills most vulnerable to automation. The skills that resist AI displacement — negotiation, financial intelligence, relationship-building, entrepreneurial judgment — are the skills the right side of the CASHFLOW Quadrant requires.

The employee risk profile: Four numbers that change the conversation

Before exploring the alternative, it’s worth grounding the problem in data. These four statistics reframe what “job security” actually means for most working Americans.

These numbers point to the same conclusion: employment income is deeply fragile. It requires continuous personal activity to exist, stops instantly when that activity stops, and can be eliminated by decisions made in boardrooms workers never enter. It is not security — it is a temporary agreement, renewable at the employer’s discretion.

The “good grades, good job” promise has expired

For generations, the prescribed path was consistent: study hard, earn a degree, and secure a stable career. As recently as 2015, this formula had real-world validity. In 2025, the formula has broken down in measurable ways.

Data from the U.S. Bureau of Labor Statistics shows long-term unemployed individuals — those out of work for more than six months — now make up nearly 26% of all unemployed workers, the highest share in years. One-third of that group are college graduates. A decade ago, graduates made up only one-fifth of long-term unemployed. The degree advantage has narrowed dramatically, eroded by AI-driven hiring filters, mass tech layoffs, and a structural shift in what employers actually need.

Entry-level job listings have declined steadily since 2022, even as graduate unemployment for workers aged 22–27 has climbed toward 6%. The graduating class of 2025 is entering one of the weakest entry-level markets in recent memory, carrying an average of $39,375 in student loan debt — and being told, once again, that employment is the secure choice.

Robert Kiyosaki’s poor dad — a man of genuine intelligence and strong credentials — believed in the security of employment. His advice was sincere. But it was built for an economy that no longer exists. The right lesson isn’t “get better credentials.” It’s to understand that no credential confers the kind of security that assets provide.

What “secure” employees are actually trading away

The illusion of job security has a cost that most employees never fully calculate. When someone accepts employment as their financial foundation, they also accept a specific set of constraints:

- The highest effective tax rate

Employees pay up to 35.7% effective federal tax rates — the worst position in the CASHFLOW Quadrant. Wages are taxed before the employee ever sees them. Business owners and investors access the tax code’s most powerful deductions before paying income taxes. - An income ceiling

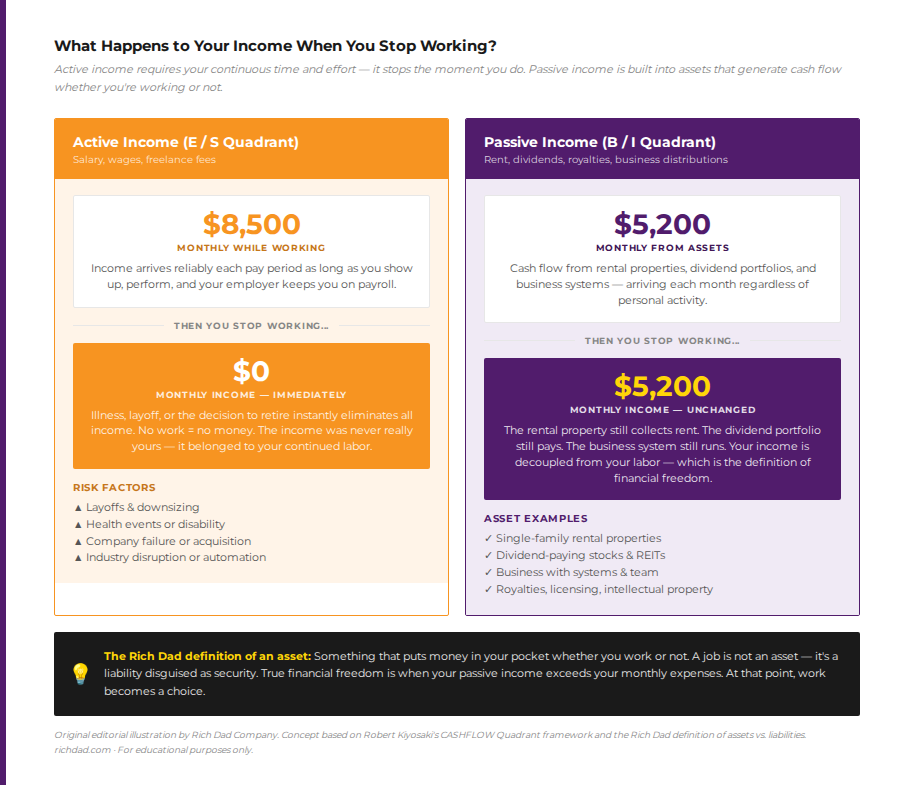

Employee income is capped at hours × wage. There is no mechanism to scale income without trading proportionally more time. Business owners and investors have no such ceiling — their income scales with systems and assets, not personal hours. - Income that stops immediately. A layoff, an illness, a disability — any of these ends the income stream instantly. Passive income from assets doesn’t stop because the owner stopped working. That distinction is the entire foundation of financial freedom.

- Zero control. The employer sets the hours, assigns the projects, approves the raises, and decides when the arrangement ends. An employee’s financial trajectory is largely determined by decisions made by other people.

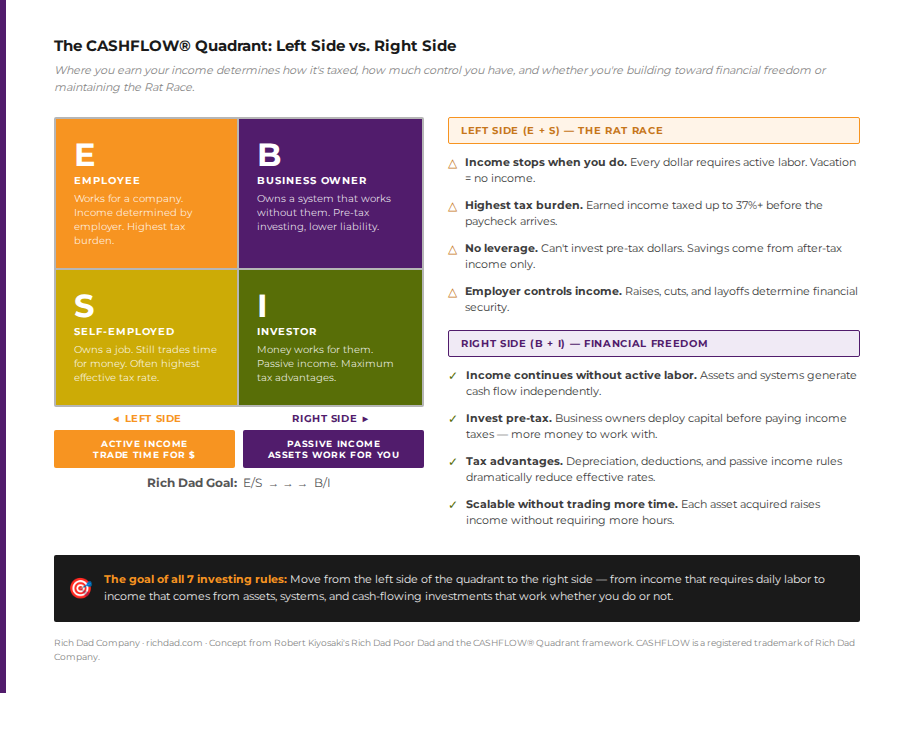

The CASHFLOW Quadrant: Where real security lives

Robert Kiyosaki’s CASHFLOW Quadrant divides income earners into four categories: Employee (E), Self-Employed (S), Business Owner (B), and Investor (I). The left side of the quadrant — E and S — depends entirely on personal labor. The right side — B and I — generates income from systems and assets that operate independently.

Most people assume the left side is safer because it feels familiar. But the data above challenges that intuition. Left-side income stops when labor stops. It carries the heaviest tax burden. It has no scalability. And it is, by design, contingent on another party’s approval.

The right side carries a different kind of risk — the risk of learning, of building, of making early-stage mistakes. But that risk is limited and diminishing. As financial education deepens and as systems mature, risk on the right side decreases while income increases. On the left side, risk is perpetual and governed by forces outside the individual’s control.

The goal of the Rich Dad philosophy is not to condemn employment — it is to recognize employment for what it is: a starting point, not a destination. The transition from the left side to the right side begins with financial education, continues with the acquisition of cash-flowing assets, and culminates when passive income exceeds monthly expenses.

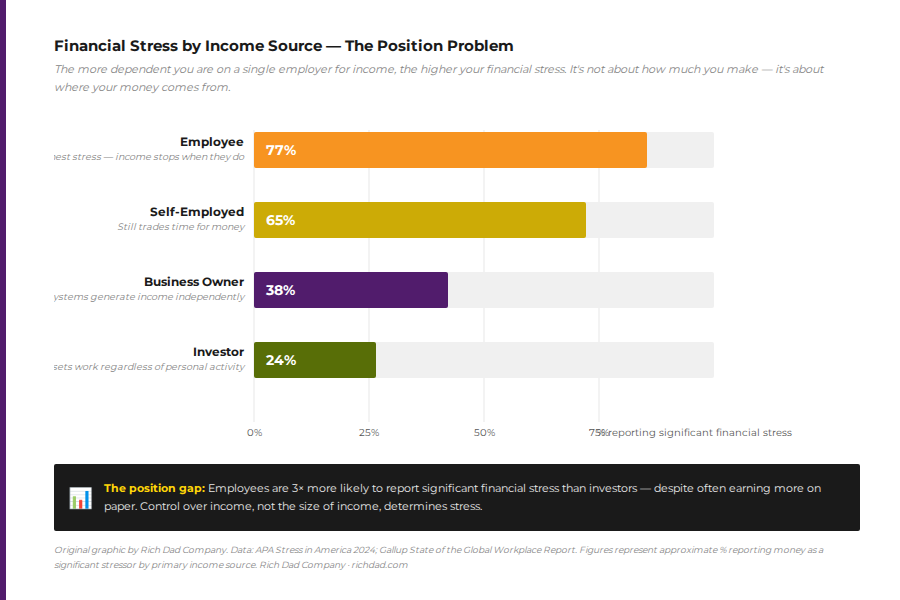

Why income source matters more than income size

One of the most revealing findings in financial stress research is that financial anxiety correlates more strongly with income source than income size. Research drawing on APA “Stress in America” data and Gallup’s Global Workplace Report shows that employees report significant financial stress at nearly three times the rate of investors — even when controlling for income level.

The reason is control. An investor’s income continues whether they show up or not. An employee’s income is contingent on daily performance, employer stability, and macroeconomic conditions none of them control. The salary may be similar; the security is categorically different.

Build real financial security — starting today

The question isn’t whether to pursue the right side of the CASHFLOW Quadrant — the data makes the case. The question is how to begin. Here is a clear framework:

- Increase financial education. Understanding how money works — how assets are defined, how taxes function, how leverage operates — is the prerequisite for everything else. The CASHFLOW game exists precisely to build this fluency in a safe environment.

- Acquire cash-flowing assets. An asset is something that puts money in your pocket — a rental property, a dividend-paying stock position, a business with systems. Every cash-flowing asset acquired reduces dependence on the next paycheck.

- Build income that doesn’t require your presence. The goal is the financial freedom crossover point — the moment when passive income exceeds monthly expenses. At that point, work becomes a choice rather than a requirement. That is job security worth having.

- Use employment income as fuel, not a destination. There is nothing wrong with earning a paycheck while building assets on the side. The mistake is treating the paycheck as the end goal. Every paycheck is an opportunity to acquire another income-producing asset — to convert temporary earned income into permanent passive income.

A job gives you income. An asset gives you freedom. The goal is to accumulate enough assets that their combined cash flow exceeds your expenses — permanently. That is the only definition of security worth building toward.

~ Rich Dad philosophy, based on Robert Kiyosaki’s CASHFLOW Quadrant framework

The real risk is staying where you are

There is a pervasive myth that entrepreneurship and investing are the risky choices. The data has never supported this. What is risky is building an entire financial life on a single income stream that can be eliminated in a meeting the employee never attends. What is risky is entering retirement with a savings account instead of a portfolio of income-producing assets. What is risky is assuming that loyalty to an employer translates into financial protection.

The current environment — rising layoffs, AI-driven displacement, declining real wages, and surging financial anxiety — is not an anomaly. It is the structural reality of employment-based income made visible. The smart response is not to negotiate a better employment arrangement.

The following message has not changed in 25 years: move from the left side of the CASHFLOW Quadrant to the right side. Not because employment is without value, but because it is insufficient as a financial foundation. Begin with education. Build with assets. And define security on your own terms — not someone else’s payroll.

FAQs

It is structurally a myth. Even in strong labor markets, the average employee stays with one employer for fewer than four years. Job security implies a durable arrangement — but employment is an at-will relationship in most U.S. states, subject to layoffs, restructuring, automation, and economic downturns at any time. What exists is temporary income, not security.

Real financial security, in Rich Dad terms, is the point at which passive income from assets permanently exceeds monthly living expenses. At that point, a layoff, a recession, or an industry disruption does not threaten your standard of living. You have built income streams that operate independently of your continued employment.

The transition begins with financial education — understanding assets, liabilities, cash flow, and taxes. From there, the goal is to redirect earned income into cash-producing assets: rental real estate, dividend stocks, a business with systems. Each asset acquired reduces reliance on the next paycheck. The Rich Dad philosophy is not anti-employment; it is pro-asset.

It is safer in the long run, though it carries more short-term uncertainty. Employees face permanent external risk — layoffs, automation, economic downturns — that they cannot control. Entrepreneurs and investors face risks they can learn to manage. Risk managed through knowledge is fundamentally different from risk entirely outside your control.

Start with financial education — specifically, learning to distinguish assets from liabilities and understanding how the tax code treats different types of income. The CASHFLOW game is designed to build this fluency in a practical, engaging way. From there, begin acquiring your first cash-flowing asset, even a small one. The first asset is the most important one — it proves the concept and builds the mindset.