What investment planning actually means, and where most people go wrong

Standard investment planning advice from mainstream financial institutions typically follows a familiar script: determine a retirement goal, calculate how much to save each month, select an asset allocation mix based on age and risk tolerance, and trust compound interest to do the rest. It is not bad advice — but it is incomplete advice.

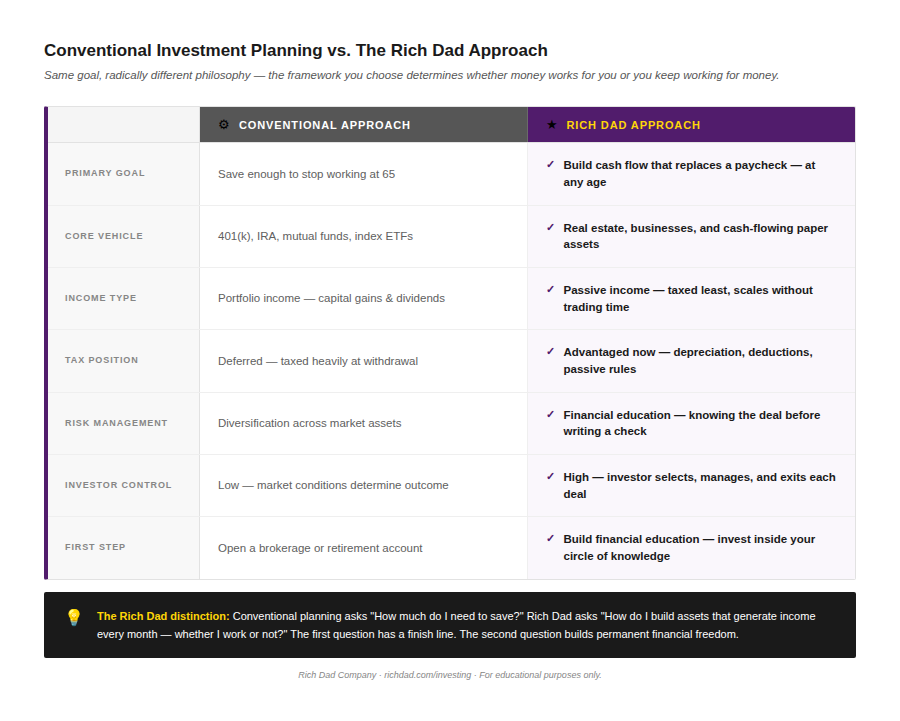

The core problem is this: conventional investment planning is designed around accumulation. The Rich Dad model is built around cash flow. An accumulation plan asks, “How much do I need to save?” A cash flow plan asks, “How do I build assets that generate income every month, whether I work or not?” One has a finish line. The other creates permanent financial freedom.

Robert Kiyosaki first encountered this distinction not in a textbook but through a painful early lesson. In 1974, he purchased a small condominium on the outskirts of Waikiki for $56,000. His real estate agent assured him that property appreciation would eventually justify a negative monthly cash flow. Rich dad — his best friend’s father and lifelong financial mentor — took a different view. “Why would you invest in something that knowingly loses money each month?” he asked. Then he began asking the questions Robert had never thought to ask: What was the cap rate? What vacancy factor had been applied? Had HOA assessment history been reviewed? Were management and repair costs factored in? That conversation changed everything. Robert renegotiated the deal and turned it into a property generating $80 per month in positive cash flow. More importantly, he learned the first real rule of investment planning: financial education comes before financial decisions.

The five investment principles every investor needs to know

Step 1: Arm yourself with financial education before you invest

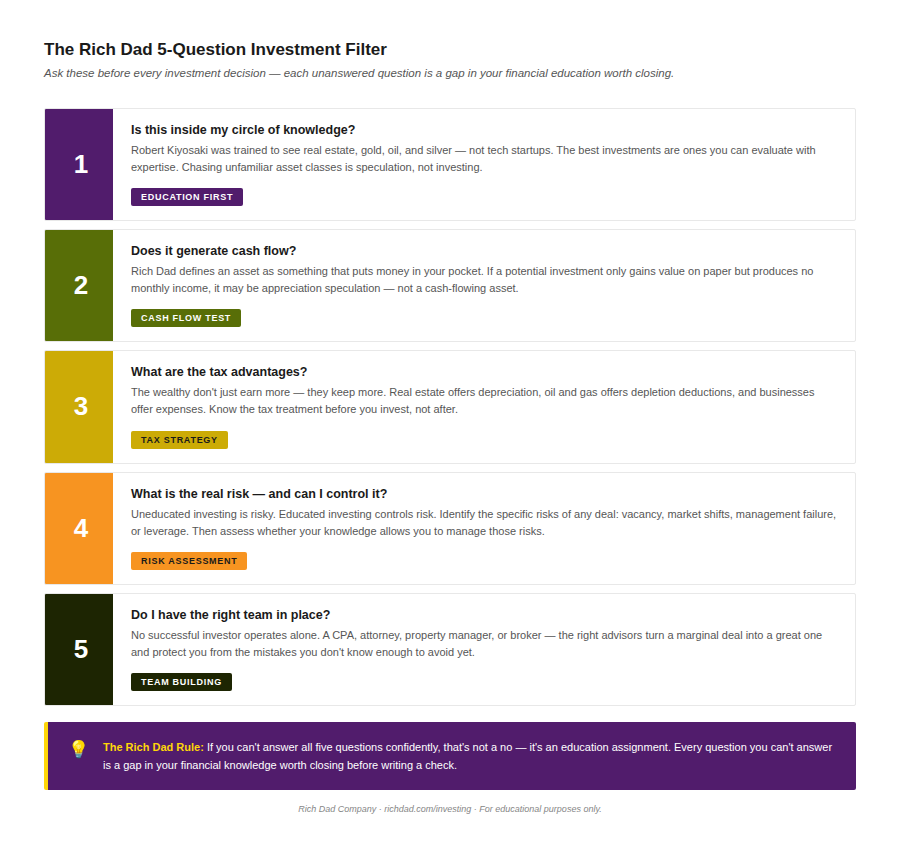

Every investment begins as a financial education problem. The investor who buys a rental property without understanding cap rates is speculating. The investor who puts money into a stock without understanding how to evaluate a company’s cash flow is gambling. The definition of financial education is not academic — it is the ability to read financial statements, evaluate deals, ask the right questions, and understand how money moves in and out of an asset.

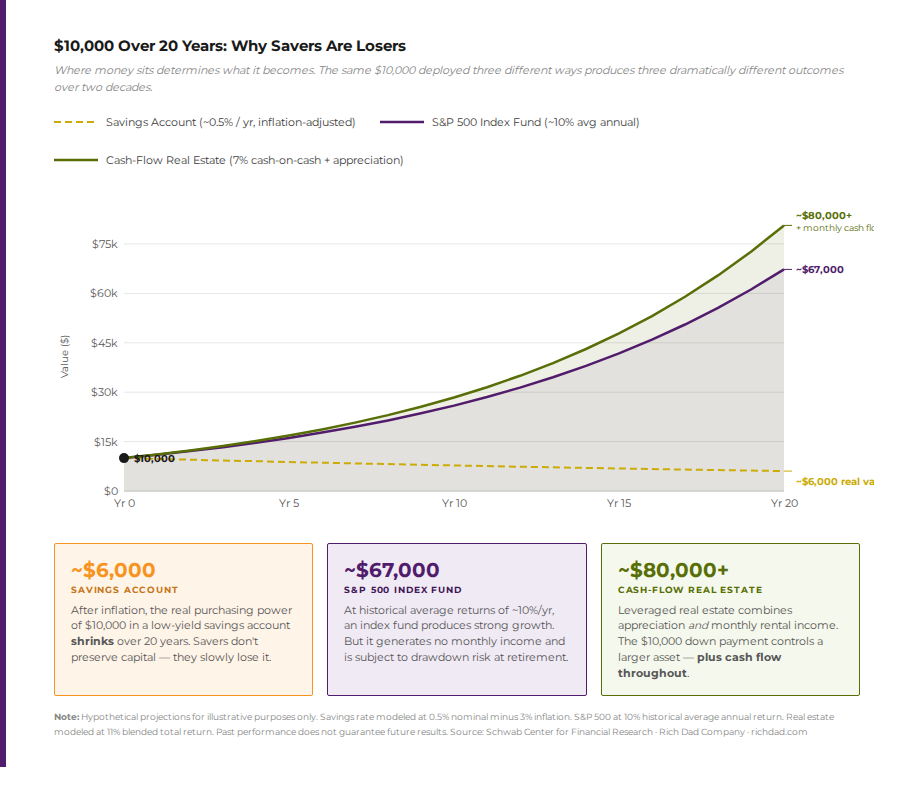

Error: Campaign not found.

The right questions before any investment should include: Does this asset generate cash flow? What is the tax treatment of that income? What are the real risks — and can I manage them with my current level of knowledge? Do I have the right advisors in place? An unanswered question is not a reason to pass on a deal — it is an education assignment. The goal is to close that knowledge gap before writing a check.

Step 2: Understand assets vs. liabilities — The foundation of every investment plan

Rich Dad’s most fundamental principle is also the one most consistently misunderstood: an asset puts money in your pocket; a liability takes money out of it. A house that generates monthly rental income is an asset. A personal residence that requires mortgage payments, property taxes, insurance, and maintenance every month — while producing no income — is a liability. A business system that generates revenue without requiring the owner’s daily presence is an asset. A job that stops paying the moment the employee stops showing up is not an asset — it is a source of earned income that disappears the moment it is no longer worked.

Understanding this distinction transforms how an investor evaluates every opportunity. The question shifts from “Will this go up in value?” to “Does this generate cash flow?” Capital gains depend on someone else being willing to pay more later. Cash flow arrives every month, regardless of market conditions, regardless of whether the owner is present, and regardless of what interest rates are doing. To explore the relationship between assets, liabilities, and personal financial planning, Rich Dad’s full framework starts with the balance sheet — not the brokerage account.

Step 3: Start small, make mistakes early, and learn from both

The second rule of effective investment planning is closely related to the first: get in the game before the stakes are too high. Kim Kiyosaki’s first investment was a rental property that she thought was a step forward. After the first tenant moved out, she assumed the market would support a $35 rent increase — without checking comparable rents in the neighborhood. The house sat vacant for three months. Instead of a small profit, she absorbed a $1,500 loss.

That mistake cost a manageable amount. It bought something far more valuable: real knowledge that no textbook can provide. She went on to own thousands of units. The early mistakes paid for themselves many times over — precisely because they were made on small positions, before significant capital was at stake.

Don’t be afraid of making mistakes. Be afraid of not learning from them. The investor who fails small and learns fast will always outperform the investor who waits until conditions are perfect — because perfect conditions never arrive.

Starting small also means something more specific: putting actual money on the line, not just studying deals in theory. As rich dad told Robert after his near-disastrous Waikiki condo: “I’m glad you took action. Most people think, but never do. If you do something, you make mistakes, and it’s from our mistakes that we learn the most.”

There is a direct neurological effect to having skin in the game. The investor who has money on the line pays attention in a fundamentally different way. That attention accelerates education in ways that passive study cannot replicate.

Step 4: Choose the right income type — Why passive income changes everything

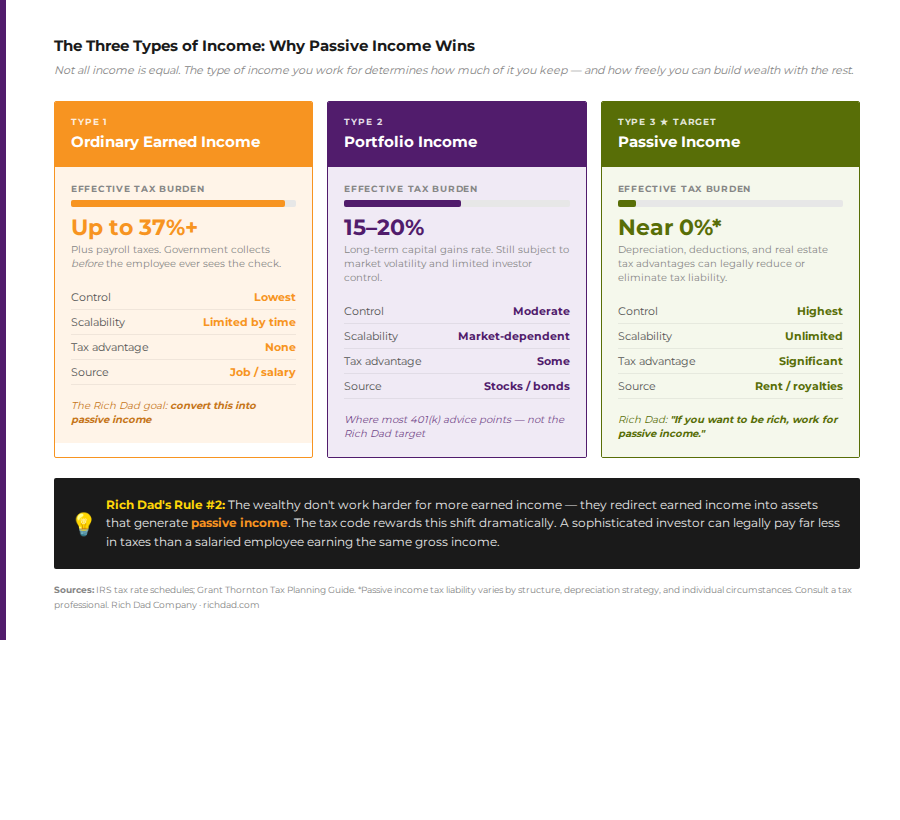

Not all income is equal — not in terms of how much of it remains after taxes, and not in terms of what it can build. There are three types of income: ordinary earned income (salary, wages), portfolio income (capital gains, stock dividends), and passive income (rental income, business distributions, royalties). Of the three, passive income is the most powerful — and the most tax-advantaged. An employee earning $150,000 in ordinary income faces an effective federal tax rate of roughly 35.7%, including payroll taxes. An investor earning the same $150,000 through passive real estate income can often reduce that rate to near zero through depreciation, deductions, and passive loss rules. That difference — compounded over years — is the mechanism by which the wealthy build wealth while the working class treads water.

Conventional investment planning rarely addresses income type. It focuses on portfolio size and asset allocation without distinguishing between the tax treatment of different income streams or the level of investor control each provides. Rich Dad’s investment framework centers on building passive income as the primary objective — not a retirement number, not a portfolio balance, but a monthly cash flow that exceeds monthly expenses. That is the crossover point. That is financial freedom.

Step 5: Stay inside your circle of knowledge — Avoid the hot-tip trap

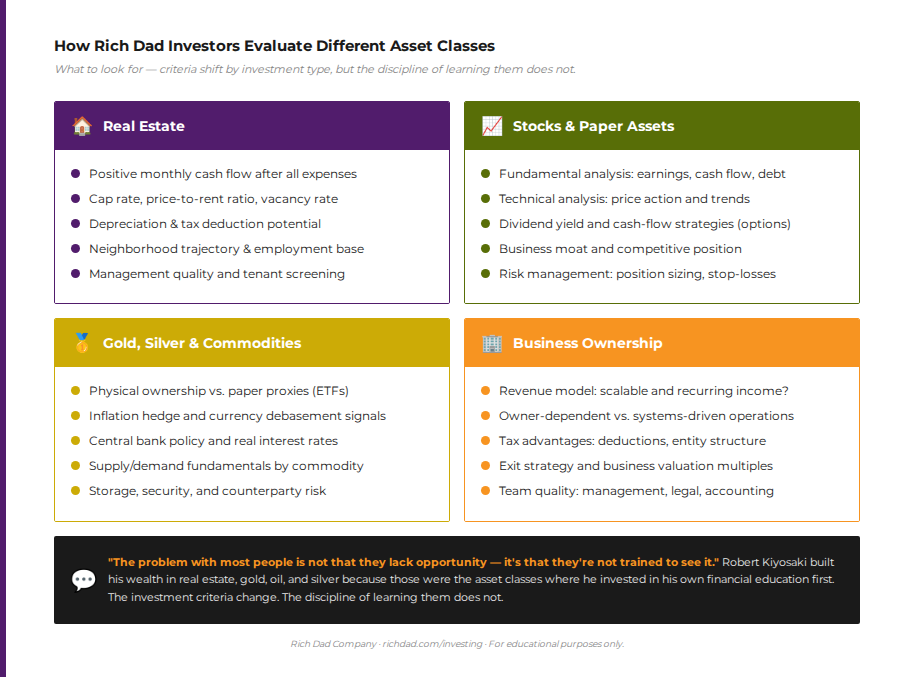

Every experienced investor has a version of the same warning: do not chase what you do not understand. The principle of staying close to home is not geographic — it is epistemic. It means investing in asset classes and deals within the investor’s existing circle of knowledge, rather than leaping toward whatever the market is currently celebrating.

This principle is what separates investing from speculation. Robert Kiyosaki’s investments have centered on real estate, oil and gas, gold, and silver — asset classes he studied deeply before committing capital. Andy Tanner, Rich Dad’s paper assets advisor, built his expertise in options strategies before trading them with real money. Kim Kiyosaki focused on residential rental properties before expanding into commercial. In every case, the investor’s education preceded the investment.

Error: Campaign not found.

The alternative — acting on a hot tip, chasing an unfamiliar asset class, or investing based on someone else’s conviction — removes the investor’s most important risk management tool: their own informed judgment. Uneducated investing is genuinely risky. Educated investing manages risk by replacing ignorance with knowledge.

This also means building and relying on a strong financial advisor team: a CPA who understands investment tax strategy, a real estate attorney who specializes in asset protection, a property manager who knows the local market, and a network of experienced investors. No successful investor operates alone. The right team turns marginal deals into great ones and flags the deals that should be avoided.

Why conventional investment planning leaves most people short

The fundamental critique of conventional investment planning is not that 401(k) plans are worthless or that diversification is wrong. It is that these tools are designed for a specific outcome: accumulating enough capital to draw down in retirement, typically over a fixed period of 20 to 30 years. However, the Federal Reserve’s 2024 Economic Well-Being Report found that 30% of Americans cannot cover three months of expenses by any means. These are not people who failed to save enough — they are people whose financial strategy was never designed to give them control.

The core of the problem, is not a savings shortfall — it is a financial education deficit. A population that understood the difference between assets and liabilities, that knew how passive income was taxed, and that had been taught to evaluate deals rather than delegate all investment decisions to Wall Street would look dramatically different from the one these statistics describe.

The Rich Dad investment planning checklist: What to ask before every investment

This investment framework reduces to a series of questions that every investor should be able to answer before committing capital. Each unanswered question is not a reason to walk away — it is an education assignment.

- Is this inside my circle of knowledge? If not, what would I need to learn to evaluate this deal confidently?

- Does it generate cash flow? How much, after all expenses — including vacancy, maintenance, management, and financing costs?

- What are the tax advantages? Does this asset offer depreciation, deductions, or passive income treatment that reduces my effective tax rate?

- What is the real risk — and can I control it? What are the specific failure modes, and does my knowledge allow me to manage them?

- Do I have the right team in place? CPA, attorney, property manager, broker — who is on my side before this deal closes?

These five questions form the basis of Robert Kiyosaki’s approach to every investment opportunity and align directly with the Rich Dad 5-Question Investment Filter taught across Rich Dad’s financial education programs. If any of the five cannot be answered confidently, the deal should wait — or the education should accelerate.

Investment planning is an education problem first

The most effective investment plan is not the one with the most sophisticated asset allocation or the highest projected return. It is the one built on a foundation of financial intelligence — the ability to evaluate deals, identify real assets, manage real risk, and build income streams that continue whether the investor is working or not.

Robert Kiyosaki’s near-failure in Waikiki in 1974 is not a cautionary tale. It is a blueprint. The mistake was manageable. The lesson was priceless. The questions it generated became the framework for every successful investment that followed. That same process — make a small move, learn from what goes wrong, build the knowledge that informs the next move — is available to any investor willing to prioritize education over excitement.

Rich Dad’s full library of investing resources, personal finance education, and entrepreneurship guidance exists for exactly this purpose: to give every investor the financial intelligence to ask better questions, make better decisions, and build the kind of wealth that lasts.

FAQs

Investment planning is the process of selecting and managing assets to generate returns aligned with specific financial goals. Financial planning is broader — it includes budgeting, debt management, insurance, and estate planning. Rich Dad’s approach treats investment planning as the core of any financial plan, with the primary goal being to build passive income streams rather than simply accumulate a retirement balance.

The first step is financial education — specifically, learning the difference between an asset and a liability, understanding the three types of income, and becoming able to evaluate an investment deal before committing capital. Opening a brokerage account or choosing an asset class before that foundation is in place turns investing into speculation.

Conventional investment planning focuses on accumulation — saving enough in tax-deferred accounts to draw down in retirement. Rich Dad’s approach focuses on cash flow — building assets that generate monthly passive income that replaces earned income. The key distinctions are: income type (passive over portfolio), tax position (advantaged now versus deferred), and control (investor-managed versus market-dependent).

No. Rich Dad identifies five main asset classes: real estate, paper assets (stocks, options, bonds), businesses, and commodities (gold, silver, oil), and cryptocurrency. The key is not which asset class an investor chooses but whether that investor has the financial education to evaluate deals within their chosen class and whether those assets generate genuine cash flow.

Tax strategy is inseparable from investment planning in the Rich Dad framework. The tax code treats different income types very differently: ordinary earned income faces the highest effective rates, while passive income from real estate — with depreciation, deductions, and passive loss rules — can often be reduced to near zero. Building an investment plan without understanding the tax treatment of each asset class means leaving a significant portion of returns on the table.

Start small, starting within an area of existing knowledge, and accepting that early mistakes are part of the education. Kim Kiyosaki’s first rental property produced a $1,500 loss — and became the foundation of a portfolio of thousands of units. The key discipline is to make mistakes when the stakes are low, extract every possible lesson, and apply that learning to progressively larger positions as financial intelligence grows.

Financial freedom in the Rich Dad model occurs at the crossover point: when monthly passive income from assets permanently exceeds monthly living expenses. At that point, active employment becomes optional — not because a large retirement account has been amassed, but because income-generating assets continue producing cash flow regardless of whether the owner goes to work. That is the goal of Rich Dad’s investment planning framework, and it can be achieved long before traditional retirement age.