What is an investment risk management plan?

Investing in the stock market can build real wealth, but it comes with risk that never fully disappears. An investment risk management plan is a written, repeatable process for identifying the risks tied to a specific investment, sizing those risks against the potential reward, and deciding in advance how to respond if the trade moves the wrong way.

This is a central pillar of Andy Tanner’s teaching inside Zero to Cash Flow curriculum. Tanner has spent decades teaching investors that the stock market rewards preparation, not prediction. A real risk management plan doesn’t try to eliminate risk — that’s impossible. It tries to make sure risk is measured, priced, and survivable before a single dollar is committed.

Financial education and research are the foundation everything else in this article is built on. Nothing can substitute for a genuine understanding of financial markets, investment products, and the economic forces that move them. Research means digging into a company’s earnings reports, balance sheet, cash flow statement, competitive position, and industry trends — not just to find a reason to buy, but to find every reason an investment might go wrong. The goal isn’t only spotting opportunities; it’s understanding the specific risks attached to it, so disruptions can be anticipated instead of survived by accident.

The two types of investment risk your plan has to cover

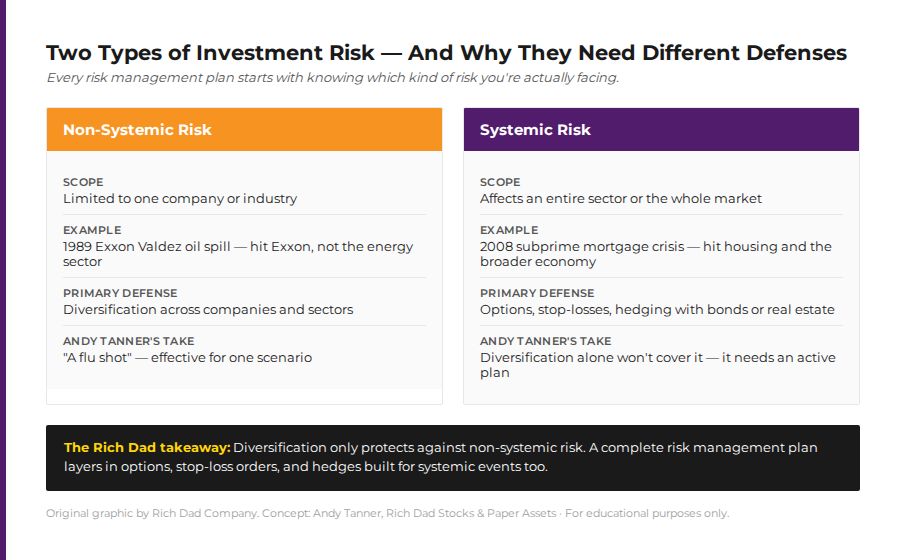

Every risk management plan starts with a simple distinction: is this risk specific to one company, or is it a risk to the whole market?

Non-systemic risk (also called unsystematic or diversifiable risk) is contained to a single company or industry. The 1989 Exxon Valdez oil spill is the classic example — it battered Exxon’s stock and its balance sheet, but it didn’t threaten the energy sector as a whole, and it certainly didn’t threaten the rest of the market. An investor holding Exxon without a plan could have taken a serious loss; an investor holding a competitor at the same time barely noticed.

Systemic risk is different. It’s a risk that can drag down an entire sector or the market as a whole. The 2008 subprime mortgage crisis is the textbook case: it didn’t just hurt a handful of poorly run banks — it took the housing market and the broader economy down with it. Investors researching the difference between the two will find the same conclusion taught here: non-systemic risk can be diversified away; systemic risk has to be actively managed, because it can’t.What is an investment risk management plan?

Why diversification is only half a risk management plan

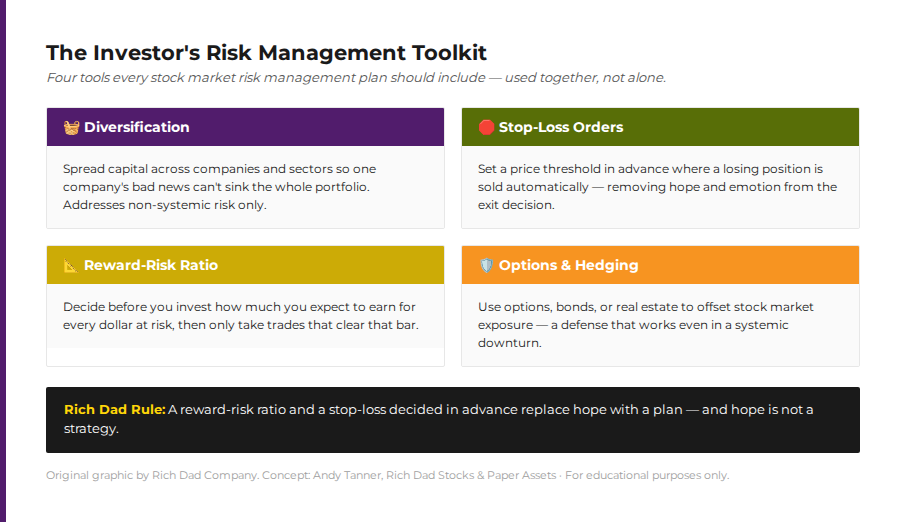

Diversification — spreading capital across different companies, sectors, or asset classes — is the risk management strategy most investors are taught first, and often the only one they’re taught. The logic holds up: a portfolio of many investments will, on average, be less exposed to any single company’s bad news than a portfolio concentrated in one stock.

The problem is that diversification only protects against non-systemic risk. It does nothing to protect a portfolio from inflation, political instability, a change in tax policy, or a recession like 2008 — the risks that hit every holding in a portfolio at the same time. Andy Tanner has a memorable way of putting this: diversification is a flu shot. It’s genuinely useful, but it only protects against the flu. It won’t do anything for heart disease, diabetes, or cancer.

That’s why a complete risk management plan looks beyond diversification to include options, stop-loss orders that automatically sell a position at a predetermined price, and hedges using other asset classes such as bonds or real estate. These tools don’t eliminate systemic risk — nothing can — but they give an investor a way to respond to it instead of simply absorbing it.

Building the risk management toolkit: Stop-losses, reward-risk ratios, and options

A risk management plan is only useful if it’s decided in advance, before emotion enters the picture. Three tools do most of the work.

Reward-risk ratio

This is the amount an investor expects to earn for every dollar put at risk, set before the trade is placed. If a position doesn’t clear that bar, it isn’t worth the risk.

Stop-loss order

A standing instruction to sell automatically once a position falls to a specific price. It replaces hope with a rule — and hope is not a strategy.

Options

These let an investor hedge a position by buying or selling the right to buy or sell a stock at a set price within a set window. Used well, options cap the potential loss on a position while leaving room for the upside.

Managing the emotional side of risk: Fear, greed, and bias

Even a well-built risk management plan fails if emotion is allowed to override it. Fear and greed are the two most damaging forces in an investor’s decision-making — fear drives investors to sell at a loss during a downturn, while greed drives them to over-invest during a rally, right before a correction wipes out the gains. Behavioral finance research shows investors feel the pain of a loss roughly twice as intensely as the pleasure of an equivalent gain, which helps explain why so many investors end up buying high and selling low — the opposite of what they set out to do.

Bias compounds the problem. Confirmation bias pushes investors to seek out information that supports what they already believe, while ignoring anything that contradicts it. Herd mentality is even more costly: by the time a crowd of investors moves into a trade, the smart money is usually already moving out. Robert has long cautioned against following the herd for exactly this reason — the herd is often being led to slaughter.

The fix isn’t willpower. It’s a plan that removes the decision from the moment of maximum emotion: clear investment goals, a defined risk tolerance, a reward-risk ratio set before the trade, and a stop-loss that executes automatically rather than waiting on a gut call in the middle of a downturn.

Risk management in action: Two real-world case studies

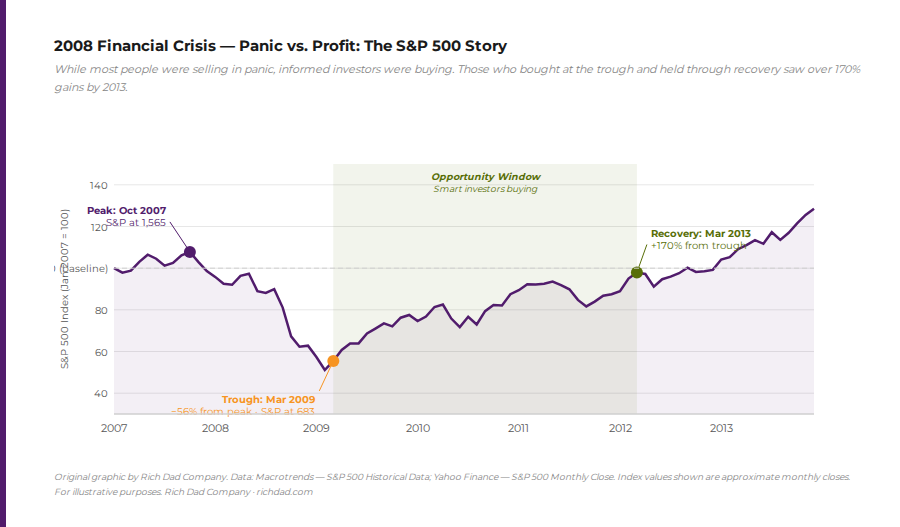

Real events make the theory concrete. The 1989 Exxon Valdez oil spill is a clean example of non-systemic risk: it hit Exxon’s stock hard, but investors who had researched the company’s underlying financial strength recognized the business had the resilience to recover — and those who held on, or bought the dip, were rewarded when the stock rebounded.

The 2008 housing crisis is the systemic-risk case study. It wasn’t contained to one company or even one industry — it took the housing market and the broader economy down with it. Most investors without a systemic-risk plan took the full hit. A smaller number, including hedge fund manager John Paulson, who built a research-driven short position against the subprime mortgage market, turned that same systemic risk into one of the largest single-year profits in Wall Street history. He wasn’t guessing, and he wasn’t following the herd.

“Defend your chart”: Andy Tanner’s risk management mantra

Andy Tanner sums up his entire approach to risk management in three words: defend your chart. Risk management isn’t just about anticipating what could go wrong — it’s about having a plan ready for when it does.

That starts with paying attention to what the market is actually doing. Technical analysis — studying price and volume trends — helps an investor decide whether to go long into an uptrend or protect a position as a downtrend develops. Layering options on top of that analysis gives an investor a way to cap potential losses without having to correctly predict every twist in the market. Together, research, technical analysis, and options form a plan that can adjust as conditions change, instead of one that only works if the market cooperates.

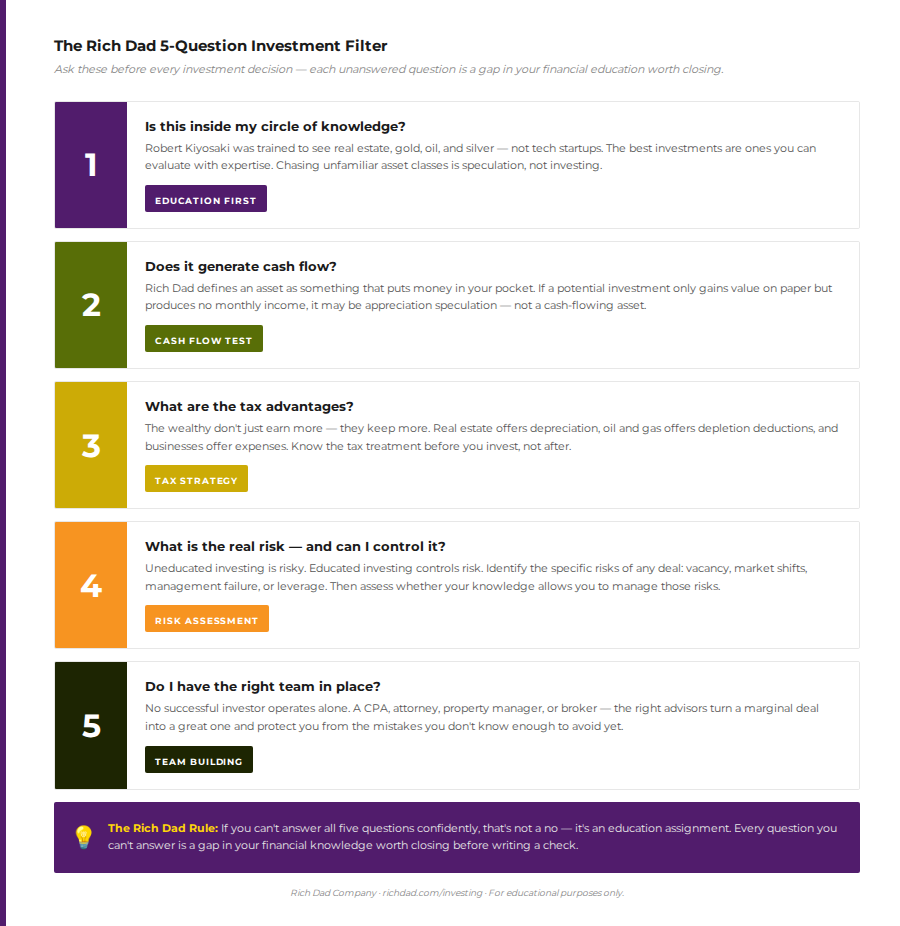

A 5-question filter to pressure-test any investment

Before committing capital to any investment — stocks, real estate, a business, or gold — run through five questions that double as a risk management checklist:

- Is this inside my circle of knowledge?

- Does it generate cash flow?

- What are the tax advantages?

- What is the real risk, and can I control it?

- And do I have the right team in place?

A question that can’t be answered with confidence isn’t a reason to walk away — it’s a gap in financial education worth closing before writing a check.

Building your own investment risk management plan

Putting all of this together, a genuine risk management plan includes: ongoing financial education and company-specific research; a clear read on whether a given risk is non-systemic or systemic; diversification for the risks it can actually cover; stop-losses, reward-risk ratios, and options for the risks it can’t; a plan for managing fear, greed, and bias before they take over; and the discipline to revisit and adjust the plan as market conditions and personal circumstances change.

None of this eliminates risk. Investing in the stock market always carries some. But an investor who has done the work — who has a plan built and in place before the first dollar goes in — is the investor who defends the chart, instead of getting run over by it. For a deeper walkthrough of these tools, visit Rich Dad’s Investing hub or explore Andy Tanner’s strategies on Rich Dad’s StockCast.

FAQs

A risk management plan is a written, repeatable process for identifying, sizing, and preparing a response to the risks tied to an investment — including how much to invest, when to sell, and which tools (stop-losses, options, or diversification) will limit losses if the trade moves the wrong way.

Non-systemic (or unsystematic) risk is limited to a single company or industry and can largely be managed through diversification. Systemic risk affects an entire sector or the whole market — such as a recession or a subprime mortgage crisis — and requires active tools like options, stop-losses, and hedging, since it can’t be diversified away.

Not on its own. Diversification reduces exposure to company-specific problems, but it does very little to protect a portfolio during a systemic event like a market-wide crash, since nearly every holding is affected at the same time.

A reward-risk ratio is the amount an investor expects to earn for every dollar put at risk, decided before the investment is made. Setting this ratio in advance — along with a stop-loss price — helps remove emotion from the decision to exit a losing position.