The Two Dads — and Two Completely Different Outcomes

Robert Kiyosaki’s poor dad was, by conventional standards, a success. He earned multiple advanced degrees, climbed the ladder of the Hawaii public school system to become its superintendent, and worked hard his entire career. He was proud of his job — and with good reason. By the metrics society uses to measure success, he had earned it.

Yet poor dad died with very little to his name. In his later years, he rarely talked about his career achievements. What weighed on him was that he had nothing to leave his children. Decades of hard work, consistent employment, and a respected professional title had not translated into financial independence. Every raise he received moved him into a higher tax bracket. Every financial emergency depleted the savings he had carefully built. He was always busy, always working, and always one unexpected expense away from starting over.

Rich dad never held a conventional job. He dropped out of school as a kid to help run his family’s store. He learned about money through real-world experience, eventually building a real estate portfolio and a series of businesses that generated income whether he was working or not. He taught Robert and his son Mike the simple formula: build assets, minimize taxes legally, and make money work for you. By the time Robert was an adult, rich dad was genuinely wealthy — not because he worked harder than poor dad, but because he operated by different financial rules.

The contrast between these two men is not a story about luck or special talent. It is a story about the CASHFLOW Quadrant — the framework Kiyosaki developed to explain why people in different income categories live under fundamentally different financial conditions. The quadrant has four positions: Employee, Self-Employed, Business Owner, and Investor. Poor dad spent his life in the E quadrant. Rich dad built his wealth from the B and I quadrants. The rules — especially the tax rules — are not the same.

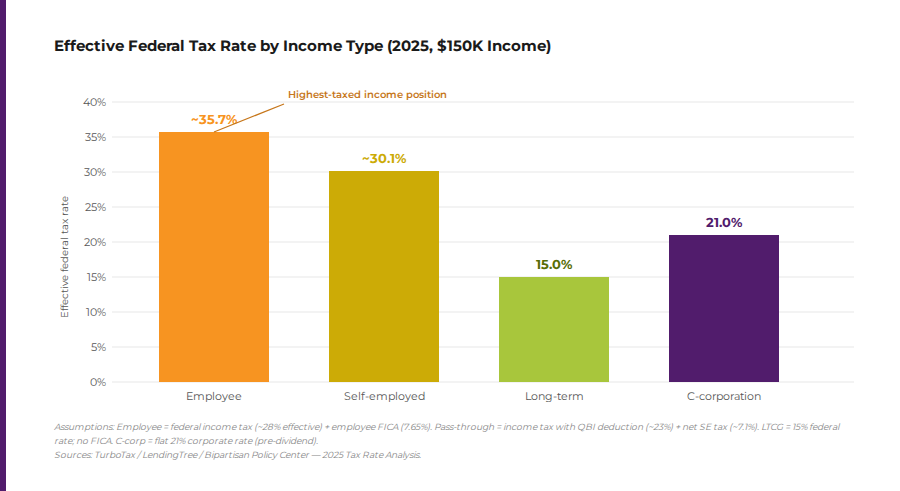

Why Employment Is the Highest-Taxed Income Position

The tax code in the United States was not designed to reward employment. It was designed — intentionally — to reward entrepreneurs and investors who create jobs and grow the economy. Understanding this is not a cynical observation about the system. It is a practical financial fact that shapes the lifetime wealth potential of everyone who earns a paycheck.

For 2025, the top federal income tax bracket for individuals is 37% on earned income. That is the rate applied to wages — the primary income source for employees. On top of federal income tax, employees pay FICA taxes: Social Security and Medicare, totaling 15.3% of gross wages, with the employee’s share at 7.65% (the employer pays the other half). The combined burden means a high-earning employee can see an effective federal tax rate well above 30% before state taxes are factored in.

Business owners and investors operate under fundamentally different rules. Pass-through business owners — sole proprietors, S-corp owners, and partners — qualify for the Qualified Business Income (QBI) deduction, which reduces their effective top rate to approximately 29.6% on business income. C-corporations pay a flat 21% corporate tax rate. And investors earning long-term capital gains pay a maximum federal rate of 20% — nearly half the top rate on employee wages. Beyond tax rates, business owners and investors have access to a wide range of deductions unavailable to employees: office expenses, vehicle use, equipment, business travel, and retirement contributions far larger than those available through employer plans. The practical result is that a business owner or investor paying a lower effective tax rate on income that is also structured to grow — through assets, compounding, and leverage — accumulates wealth at a fundamentally different trajectory than an employee earning a comparable gross income and paying taxes first.The job security myth: What the numbers actually show

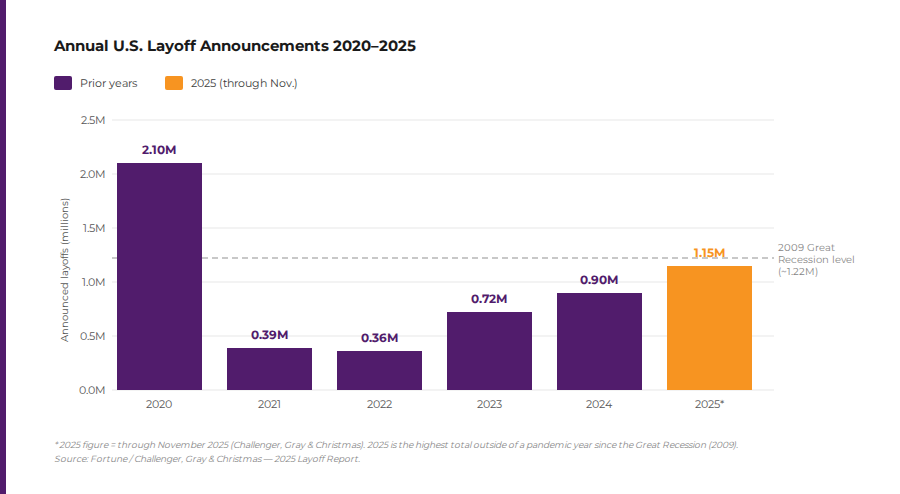

The job security myth

Perhaps the most deeply held belief supporting the “get a good job” narrative is security. A steady paycheck, employer-provided benefits, and the predictability of a salary feel safer than the volatility of entrepreneurship or investing. This perception has always been somewhat fragile. In 2025, it has become demonstrably untrue.

According to Challenger, Gray & Christmas, more than 1.1 million layoffs were announced through November 2025 — the highest total since the pandemic year of 2020, and before that, the depths of the Great Recession in 2009. Technology, government contracting, finance, and professional services all saw significant cuts. A new pattern identified by workplace analysts has been labeled the “forever layoff”: smaller, continuous rounds of cuts that never make headlines but create a persistent atmosphere of anxiety throughout the workforce.

A survey by Clarify Capital found that 1 in 3 Americans reported “layoff anxiety” heading into 2025. Nearly one-third said they would accept a 10–20% pay cut just to feel more secure in their positions. Among those who had already been laid off, 1 in 10 had no confidence they could find comparable work within three months. These are not the sentiments of people who feel financially secure.

The asymmetry at the heart of employment is exactly what rich dad understood and poor dad missed. When a company needs to cut costs — whether due to economic pressure, AI adoption, restructuring, or changing market conditions — the owner’s interests and the employee’s interests are directly opposed. The owner preserves the business by eliminating positions. The employee, with no ownership stake and no independent income, absorbs the full consequence. As rich dad observed: the most secure position in any economic cycle is on the ownership side of the equation, not the payroll side.Why Employment Is the Highest-Taxed Income Position

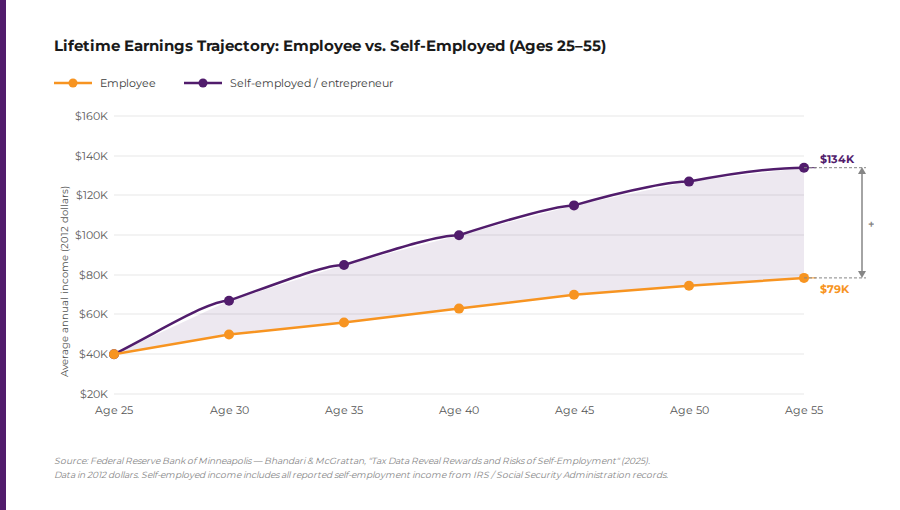

The wealth gap between employees and entrepreneurs

The long-term financial difference between staying in the employee quadrant and moving toward business ownership or investing is not abstract — it is documented.

Research drawing on IRS and Social Security Administration data, published by the Federal Reserve Bank of Minneapolis, found that while self-employed workers and employees start with comparable earnings at age 25, by age 55 the average self-employed individual earns nearly twice as much as their employed counterpart: $134,000 versus $79,000 annually (in 2012 dollars). The divergence is not primarily about working harder — it reflects the compounding structural advantages of asset ownership, tax treatment, and the ability to build equity rather than simply exchanging time for wages.

The same research noted that self-employment income is heavily skewed toward the top, with 80% of all self-employment income earned by those making more than $100,000 per year. This reflects a reality the Rich Dad philosophy has always acknowledged: the entrepreneurial path carries real risk, especially early on. But for those who commit to financial education, build the right skills, and learn to operate in the B and I quadrants of the CASHFLOW framework, the long-term financial outcome is substantially different from a career spent earning wages.The job security myth

Changing your mindset: from employee to owner

The most important shift the Rich Dad philosophy advocates is not a change in income — it is a change in thinking. Poor dad was not a failure. He was a highly educated, genuinely accomplished man who operated from a mindset shaped entirely by the employee quadrant. He worked hard for money because that is what he had been taught to do. The idea of making money work for him — through real estate, stocks and paper assets, or business ownership — was not part of his framework.

Transitioning from the E quadrant to the B or I quadrant does not require quitting a job tomorrow. It requires three things: financial education that changes the way income, expenses, assets, and liabilities are understood; the development of skills that can generate income outside of employment; and the patience to build assets over time rather than consuming all earned income as expenses. This is exactly the progression that the Rich Dad philosophy has described since Rich Dad Poor Dad was first published.

The starting point is understanding the difference between an asset and a liability — one of the most fundamental distinctions in the Rich Dad framework. An asset puts money in a pocket. A liability takes money out. A job, under this definition, is not an asset. It is a source of income that stops the moment employment ends. A rental property, a business that operates without the owner’s constant presence, or a portfolio of cash-flowing paper assets continues generating income regardless of whether the owner shows up. Building toward that kind of financial structure — even while maintaining employment — is what separates the financial trajectories of those who build wealth and those who remain trapped in the cycle of earning and spending.

AI, automation, and the new employment reality

There is one dimension of the “get a good job” narrative in 2025 that adds urgency to the Rich Dad argument: artificial intelligence is systematically eliminating the white-collar, knowledge-based work that employment was once assumed to provide indefinitely.

According to a Stanford Digital Economy Lab study, early-career workers aged 22 to 25 in AI-exposed roles — software development, customer service, data analysis — have seen steep declines in employment since late 2022. Since 2023, employers have attributed more than 70,000 announced job cuts explicitly to AI adoption. A survey by IDC and Deel found that 66% of global enterprises plan to cut entry-level hiring due to automation.

The skills that AI cannot easily replicate — negotiation, relationship-building, financial judgment, entrepreneurial decision-making — are precisely the skills the Rich Dad philosophy has always emphasized. This is not coincidence. The ability to read a market, build a business, manage cash flow, and create value through human judgment has always been more durable than any specific technical skill. In the AI era, this distinction becomes even more consequential.

The choice is not between a job and unemployment. It is between building financial intelligence and assets that generate income independent of any single employer — or remaining entirely dependent on a paycheck that can be eliminated at any moment. For more on how AI is reshaping the career landscape, the Rich Dad perspective on entrepreneurship and financial education offers a framework for navigating the transition.

The real scam–and the real alternative

The “get a good job” scam is not malicious. Most people who pass it along — parents, teachers, well-meaning advisors — genuinely believe it. But belief does not change the structural reality: employment is the highest-taxed income position, the least protected in economic downturns, and the least likely to generate the kind of compounding wealth that produces financial freedom.

Poor dad worked hard his entire life and died with regrets. Rich dad worked smart, built assets, and understood the tax code. The difference was not effort — it was education. The financial education that schools do not teach, that most employers have no incentive to provide, and that the conventional “get a good job” narrative actively discourages.That education is available. It begins with understanding the CASHFLOW Quadrant, learning the difference between good debt and bad debt, and developing the financial intelligence to begin moving income away from the most heavily taxed, least secure position in the economy — and toward assets that generate cash flow. The question is not whether the current system is fair. The question is whether to understand it well enough to operate by its actual rules — the same ones the wealthy have always used.The wealth gap between employees and entrepreneurs

FAQs

Because it frames employment as the path to financial security when the structure of employment — high taxes, no ownership, total dependence on an employer’s continued willingness to pay — actively works against long-term wealth building. The scam is not the job itself; it is the belief that a job alone is sufficient. For a deeper look at the tax math, see the Rich Dad overview of personal tax strategies.

No. Employment is a starting point — it is how most people begin their financial lives. The Rich Dad philosophy encourages people to use employment as a platform: work to learn skills, build relationships, and generate income that can be directed toward assets. The problem is treating a job as a destination rather than a vehicle. Even while employed, anyone can begin developing financial intelligence and acquiring assets on the side.

Employees pay income tax on every dollar earned before they can spend or invest it. Business owners pay many legitimate expenses before calculating taxable income — meaning they pay taxes on profits, not gross revenue. Investors earning long-term capital gains pay a maximum federal rate of 20%, compared to 37% on wages. Pass-through business owners with the QBI deduction face an effective top rate closer to 29.6%. The structural advantage compounds over a career. More detail is available through these tax education resources.

Building assets — investments, businesses, and income streams that generate cash flow independent of employment. This begins with financial education: understanding the CASHFLOW Quadrant, the difference between assets and liabilities, how real estate and paper assets generate passive income, and how to use the tax code strategically. The transition does not require quitting a job immediately — it requires beginning to think and act like an investor and business owner, regardless of current employment status.

AI is eliminating the entry-level and mid-tier knowledge work that once made white-collar employment feel secure. Tens of thousands of layoffs in 2025 were directly attributed to AI adoption by employers. This accelerates the Rich Dad argument: skills and assets that AI cannot replicate — judgment, relationship capital, financial intelligence, entrepreneurship — become more valuable precisely as AI commoditizes technical skills. The full picture is explored through the Rich Dad entrepreneurship hub.

The Rich Dad philosophy recommends starting with financial education rather than action. Read, study, and build the conceptual framework first. The CASHFLOW game is designed specifically to simulate the mechanics of moving from employee to investor in a low-risk environment. From there, exploring real estate strategies, stock market cash flow, and entrepreneurship as parallel tracks — alongside employment, not instead of it — is the practical starting point.