The Game Has Rules — Most Players Don’t Know Them

There is a reason professional traders consistently outperform retail investors over long time horizons. It is rarely superior market knowledge. More often, the gap comes down to process — specifically, a disciplined approach to managing the mental traps that cause ordinary investors to buy high, sell low, and make decisions based on the most recent headline rather than the underlying fundamentals.

Robert Kiyosaki has long described financial intelligence not as a measure of what you know about markets, but as a measure of how well you understand money itself — and how clearly you can see your own blind spots. In that framework, learning to think like an investor is less about acquiring data and more about upgrading the mental operating system through which all financial decisions are processed.

Error: Campaign not found.

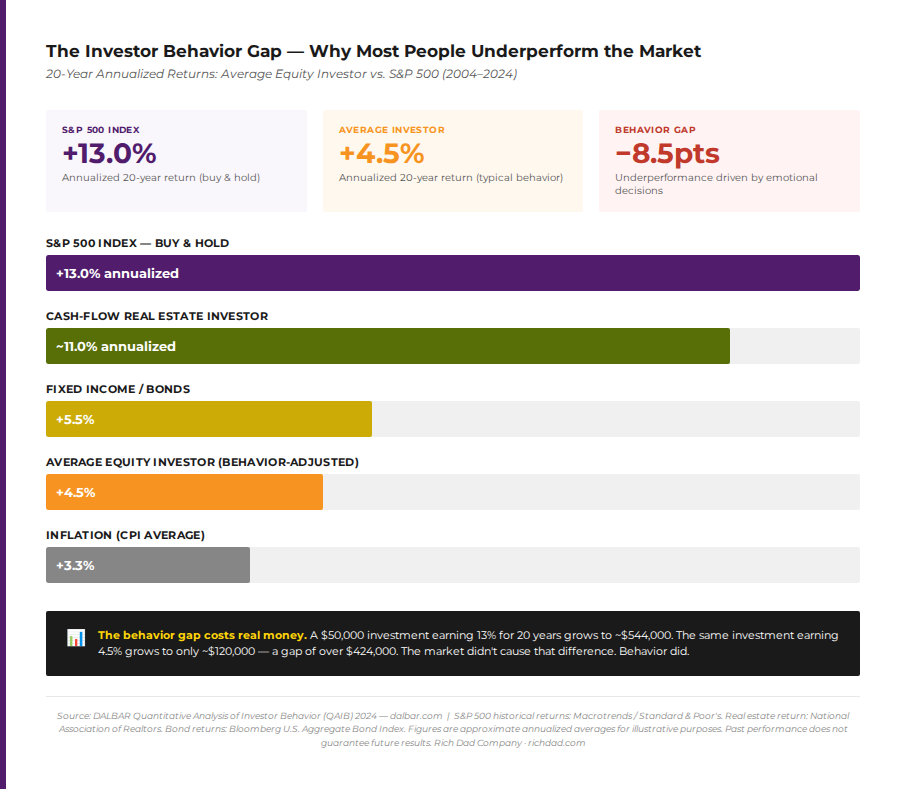

Markets reward this kind of thinking disproportionately. According to DALBAR’s Quantitative Analysis of Investor Behavior, the average equity investor lagged the S&P 500 by 848 basis points in 2024 alone — a gap driven almost entirely by behavioral patterns rather than asset selection. Understanding those patterns is where the game actually begins.

Level 1: The Biases That Cost Investors Money

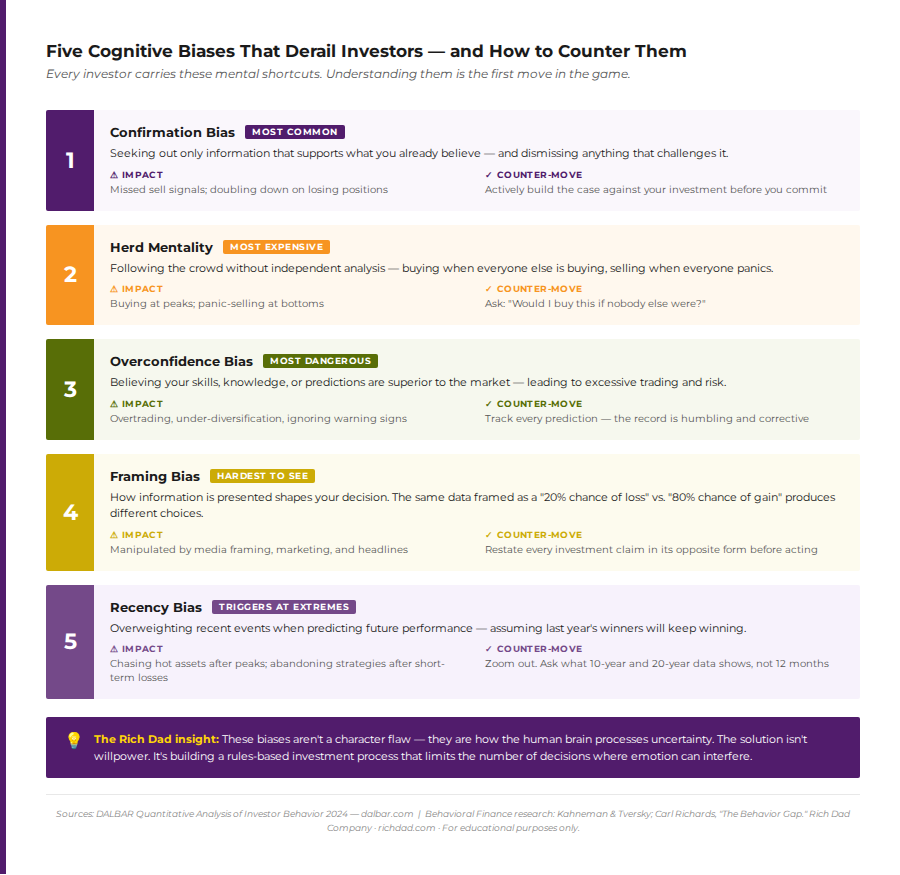

Every investor carries mental shortcuts the brain uses to process information quickly. In everyday life, these shortcuts are efficient. In financial markets, they are expensive. The most common cognitive biases in investing are well-documented — and awareness is the first line of defense against them.

Confirmation Bias: Only Seeing What You Want to See

Confirmation bias is the tendency to seek out and give weight to information that confirms what you already believe — while dismissing evidence that contradicts it. In investing, this manifests as holding on to a deteriorating position because the investor keeps finding reasons to stay, while ignoring the warning signs accumulating on the other side of the ledger.

The fix is disciplined inversion. Before committing to any investment, build the strongest possible case against it. Seek out credible analysts who disagree with your thesis. If those arguments cannot be answered, the thesis isn’t ready.

Herd Mentality: Following the Crowd Into Crowded Trades

Herd behavior is what happens when the fear of missing out overrides independent analysis. It drives retail investors into overvalued assets at the top of market cycles — and out of undervalued assets at the bottom. A 2024 study found that investors who followed upward social comparisons (observing top-performing traders on social platforms) increased risky asset allocations by 20% — amplifying the very risk they were trying to reduce.

The crowd is not always wrong. But when the crowd is also the price, following it eliminates the margin of safety that makes an investment sound.

Overconfidence: The Most Dangerous Form of Ignorance

Overconfidence leads investors to trade too frequently, size positions too large, and ignore risk management because they believe their analysis is better than it is. Studies consistently show that overconfident investors underperform — not because their ideas are wrong, but because their conviction prevents them from updating when evidence changes.

Error: Campaign not found.

The antidote is a simple practice: track every prediction in writing. The record is almost always humbling — and that humility is worth more than most investment courses.

Framing Bias: How Information Is Packaged Changes Decisions

Framing bias describes how the presentation of identical information produces different decisions. Investors told a stock has a “20% chance of loss” respond differently than investors told the same stock has an “80% chance of gain” — even though the data is exactly the same. Financial media, product marketing, and brokerage communications are expertly designed to frame information in ways that produce action. Recognizing this is a competitive edge.

Level 2: Navigating the Information Age Without Getting Buried

The democratization of financial information was supposed to level the playing field between institutional investors and individuals. In many ways it has. But democratized information also means democratized misinformation — and the cognitive load of processing an endless stream of financial news, social media commentary, and expert analysis creates its own set of problems.

Information overload does not make investors better informed. It tends to do the opposite — pushing most people back toward the handful of sources that confirm what they already believe, and leaving them more susceptible to the biases described above, not less.

The Signal-to-Noise Problem

The challenge in today’s financial environment is not finding information — it’s distinguishing signal from noise. Most financial content is produced to generate engagement, not to help investors make better decisions. Breaking news, hot takes, and dramatic market commentary all drive clicks and views. Slow, patient, fundamentals-based analysis does not trend on social media.

Rich Dad has always emphasized building financial intelligence as a foundation before consuming financial commentary. Without that foundation, investors have no framework through which to evaluate what they’re reading — and everything sounds equally authoritative.

How to Filter Effectively

Practical information hygiene for investors follows a few principles:

- Prioritize sources that challenge your current thinking over sources that validate it.

- Separate the framing from the underlying data — find the original research, not the editorial summary.

- Apply the Rich Dad investing filter: Does this investment generate cash flow? Is it inside your circle of knowledge? What are the tax implications? If any of those questions cannot be answered confidently, that’s an education assignment before it’s an investment.

- Deliberately seek out a different financial perspective each week — one that disagrees with your current portfolio positioning.

Level 3: How Contrarian Thinking Separates Good Investors from Great Ones

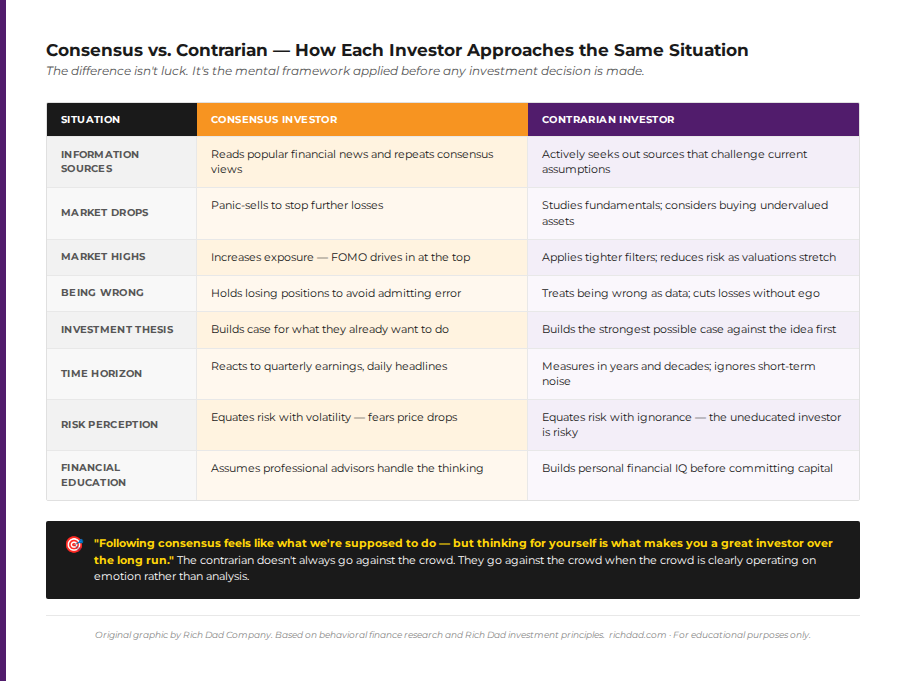

Contrarian investing is frequently misunderstood as simply doing the opposite of whatever the market is doing. That is not what it means. A genuine contrarian investor is not reflexively pessimistic or perpetually skeptical. They are independently analytical — willing to reach conclusions that differ from consensus when the evidence supports it, and humble enough to agree with consensus when the evidence supports that instead.

The key insight is that markets are driven by sentiment as much as by fundamentals. When sentiment and fundamentals diverge — when assets are priced as if the good news will last forever, or as if the situation is irredeemably bad — that divergence represents an opportunity for investors who have maintained their analytical discipline.

What Contrarian Thinking Actually Looks Like in Practice

Contrarian thinking is not a personality trait. It is a set of habits built into the investment process:

- Before any investment, build the bear case first — the strongest possible argument that the investment will fail.

- When market news is universally negative and panic is widespread, study fundamentals rather than react to headlines.

- When market news is universally positive and FOMO is driving inflows, apply tighter entry criteria rather than chasing momentum.

- Read sources that disagree with your current thesis. If they raise points you cannot refute, treat that as important new information.

- Deliberately vary the media, analysts, and information sources you consume — the same diet creates the same blind spots.

As Kiyosaki has observed, the investors who profited most from the 2008 financial crisis were not the ones with the best predictions. They were the ones who had studied financial history, understood the mechanics of the housing market, and held positions built on analysis — not emotion — when panic gripped everyone else. The 2008 S&P 500 trough offered entry prices that produced over 170% gains by 2013 for those who stayed the course.

The Rich Dad Edge: Financial Education as the Unfair Advantage

Every framework discussed in this article — bias recognition, information filtering, contrarian analysis — requires one foundational asset to be useful: financial education. Without it, an investor has no basis for distinguishing sound analysis from persuasive noise, or for applying the contrarian framework to anything other than instinct.

Rich Dad defines financial intelligence as the ability to solve financial problems — to look at an asset, understand its cash flow dynamics, evaluate its tax treatment, assess its risk profile, and make an independent decision. That kind of intelligence is not innate. It is built through deliberate study, and it compounds over time exactly the way investments do.

Error: Campaign not found.

This is why the Rich Dad approach to stocks and paper assets centers not on stock-picking but on building the four pillars of investment competence: fundamental analysis, technical analysis, cash flow generation, and risk management. These pillars convert market volatility from a threat into a source of opportunity — but only for investors who have done the foundational work.

The Role of Financial Team-Building

Even the most financially educated investor does not operate alone. Rich Dad consistently emphasizes the value of building a team of advisors — accountants, attorneys, property managers, and brokers who extend the investor’s capabilities beyond their individual knowledge base. A question you cannot answer is not a reason to miss an investment. It is a signal to add the right person to your team.

The CASHFLOW game was designed precisely to accelerate this education in a low-stakes environment — giving players the experience of evaluating real financial decisions, building income streams, and managing liabilities before any actual capital is at risk. It is one of the most efficient ways to develop the pattern recognition that takes years to build through direct market experience alone.

The Playbook: Practical Steps to Upgrade Your Investor Mindset

Understanding these principles conceptually is different from making them operational. The following practices translate investor psychology from theory into habit:

- Audit your information diet

Write down the five financial sources you consumed most in the last 30 days. Ask: do these sources challenge my current beliefs, or reinforce them? If it’s mostly reinforcement, add one source per week that approaches investing from a different perspective. - Track your predictions in writing

Keep a running log of investment theses — the reasoning behind each position, and the conditions under which you would change your mind. Review quarterly. The gap between what you predicted and what happened is the most honest financial education available. - Build the bear cast first

Before any investment decision, write out the strongest argument against making it. This practice directly counters confirmation bias and forces engagement with the real risks — not just the upside narrative. - Apply a standard filter to every opportunity

Use a consistent set of questions before committing capital. Rich Dad’s investment framework asks five questions: Is this inside my circle of knowledge? Does it generate cash flow? What are the tax advantages? Can I identify and manage the real risk? Do I have the right team? An investment that cannot answer all five confidently is an education assignment first. - Invest in your financial education before your next deal

The highest-return investment most people can make is in their own financial literacy. Every concept learned reduces the probability of an expensive mistake — and increases the number of legitimate opportunities visible within any given market. The market does not reward ignorance. But it generously rewards the investor who has done the work.

Conclusion

The game of investing does have rules. They are just not the ones most people are taught. The rules of markets, asset allocation, and diversification are well-publicized. The rules of investor psychology — the mental operating system that determines whether those strategies are ever executed correctly — rarely make the front page.

Recognizing cognitive biases, developing a disciplined approach to information, and thinking independently from the consensus are not advanced concepts reserved for professional fund managers. They are foundational skills accessible to any investor willing to examine their own thinking with the same rigor they apply to balance sheets and cash flow statements.

Rich Dad’s core insight applies here as much as anywhere: the investor is the asset. Build that asset first.

FAQs

Confirmation bias is widely considered the most pervasive. It causes investors to seek out information that validates what they already believe and dismiss contradictory evidence — leading to prolonged holding of deteriorating positions and missed warning signs. Building the opposing case before any investment is the most effective counter-strategy.

Contrarian investing is the practice of reaching conclusions that differ from the market consensus when evidence supports doing so. It is not reflexively doing the opposite of the crowd. It is maintaining analytical independence — particularly valuable when market sentiment has pushed prices significantly away from underlying fundamentals, either on the upside or the downside.

According to DALBAR’s 2024 Quantitative Analysis of Investor Behavior, the average equity investor underperformed the S&P 500 by 848 basis points in 2024. Over 20 years, the compounding effect of this behavioral gap is substantial — the difference between a $50,000 investment growing to $120,000 versus $544,000, with behavior being the primary variable.

Rich Dad defines financial education as the practical ability to solve financial problems — to evaluate assets, understand cash flow, manage tax implications, and assess risk based on your own analysis rather than delegating all thinking to advisors. It is not academic knowledge about markets. It is applied financial intelligence, developed through deliberate study and hands-on experience.

Start with three habits: (1) track your financial predictions in writing and review them regularly; (2) build the bear case before every investment decision; and (3) deliberately add one information source per week that challenges your current financial worldview. These practices alone — sustained over months — produce measurable changes in decision quality.