Having money ≠ financial freedom

It is one of the most common refrains in financial conversations: “If I just had a million dollars, I’d be set.” Or: “Once I get that promotion, the money problems go away.” The assumption buried in both statements is that financial freedom is a function of income or net worth. It is not — and the evidence is everywhere.

Ed McMahon, the longtime television personality, faced foreclosure on his Beverly Hills home near the end of his life despite decades of high earnings. Nicole Murphy, ex-wife of actor Eddie Murphy, spent a $15 million divorce settlement in under four years. These are not isolated cases of bad luck. They are illustrations of a principle Robert Kiyosaki has taught for decades: having money and being financially free are two entirely different things. You can have one without the other. And without financial education, most people who earn a lot will never achieve the second.

According to a 2024 survey by Bankrate, nearly 59% of Americans say they are uncomfortable with their level of emergency savings. And the Federal Reserve’s 2023 Report on Economic Well-Being found that 37% of adults would struggle to cover an unexpected $400 expense. These numbers point to the same reality: for the majority of people, money is a source of anxiety rather than freedom — regardless of how much they earn.

This is the problem Rich Dad Company was built to solve.

What financial freedom really means

The conventional definition of financial freedom — having enough savings to retire — is not wrong, exactly. It is just incomplete, and it sets a moving target that most people never reach. Rich Dad offers a more precise and more empowering definition, grounded in the philosophy Robert Kiyosaki developed over decades of investing and financial education:

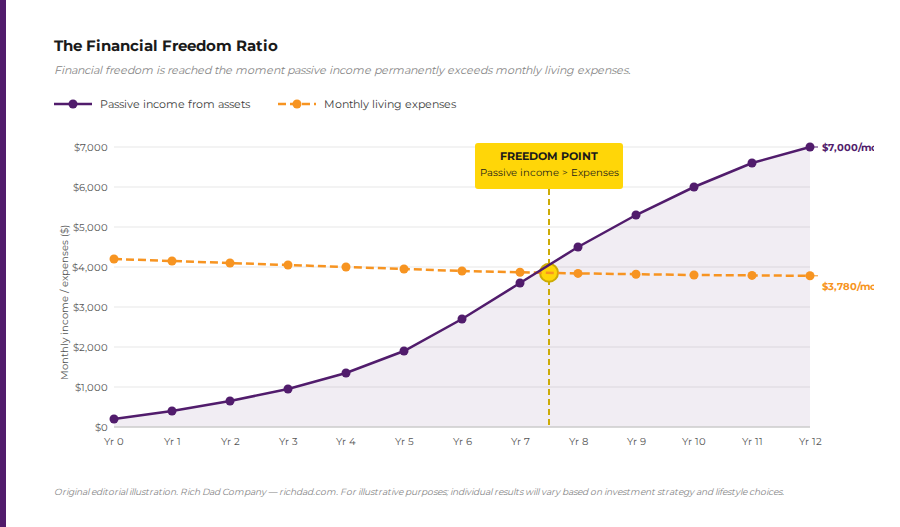

Financial freedom is the point at which the monthly cash flow from your assets equals or exceeds your monthly living expenses. At that point, you no longer have to work for money. Your money works for you. You are free.

This definition is precise enough to measure. It is not about feelings of security or a net worth target. It is a ratio — passive income versus living expenses — that can be tracked, planned for, and ultimately crossed. And that makes it achievable in a way that chasing a vague savings number never is.

There is an important distinction here from financial independence, which is addressed separately. Financial independence means your assets can sustain your expenses. Financial freedom is the broader state — it includes the mindset and the choices, not just the math. A person can be financially independent and still be controlled by money, if fear and scarcity thinking drive their decisions. True freedom requires both the structural reality of passive income exceeding expenses and the internal state of no longer being governed by financial anxiety.

Having a lot of money doesn’t mean you’re financially free

The assumption that wealth equals freedom is perhaps the most persistent myth in personal finance. It feels logical: more money means fewer problems. But the math rarely works out the way people expect, for two reasons.

The first is lifestyle inflation. As income rises, expenses tend to rise with it — sometimes faster. A person earning $200,000 a year who carries a $1.8 million mortgage, two car leases, private school tuition, and a high-end lifestyle has less financial flexibility than it appears. Every dollar of income is already spoken for. Any disruption — a job loss, a market correction, a health event — is a crisis rather than an inconvenience.

The second reason is the absence of assets that generate income. As covered inthis guide to saving vs. investing, money that sits in a savings account or gets spent on liabilities is not building financial freedom. It is being consumed. The only path to freedom is acquiring assets — investments, businesses, properties — that generate cash flow month after month, independent of whether the owner shows up to work.

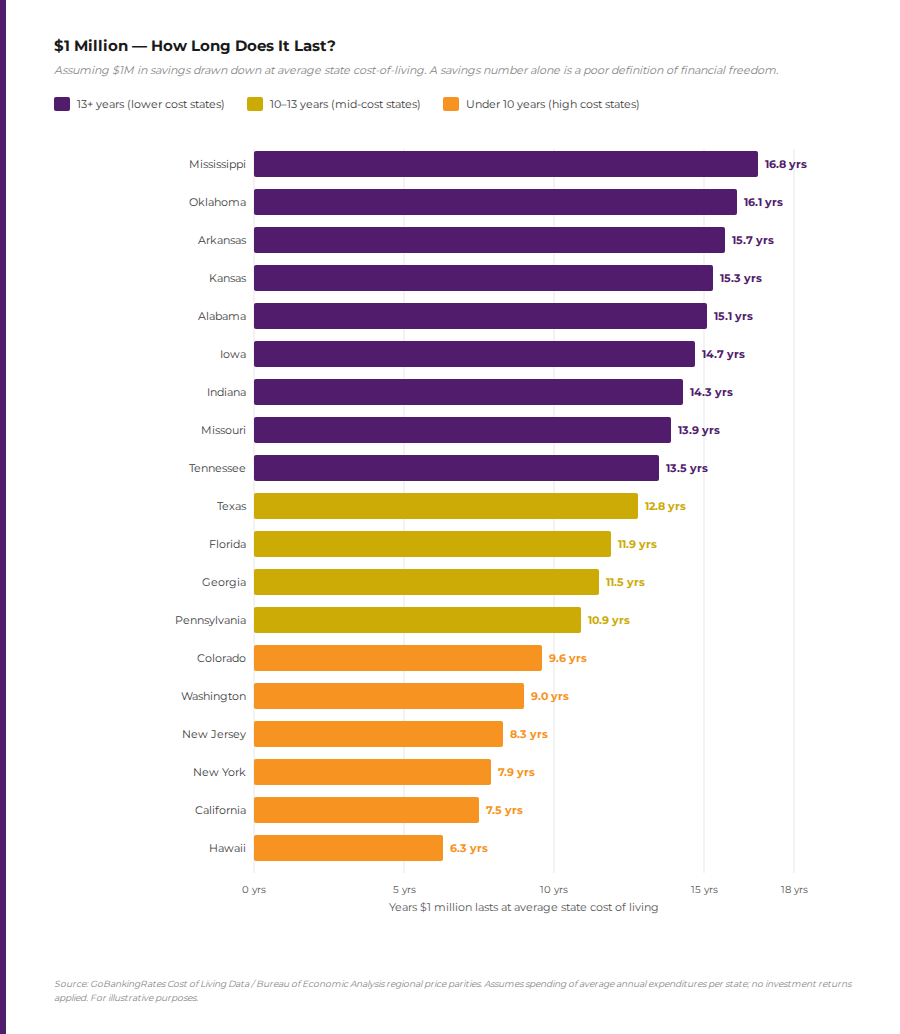

This is why the conventional retirement model — work for 40 years, save as much as possible, hope the balance lasts — produces anxiety rather than freedom for so many people. It depends on spending down a finite pile of money rather than building an ongoing stream of income. A $1 million retirement account, withdrawn at a standard 4% annual rate, produces $40,000 a year before taxes. In many U.S. cities, that is not a life of abundance. In Hawaii, a million dollars in savings lasts approximately 11 years.

Scarcity mindset vs. abundance mindset

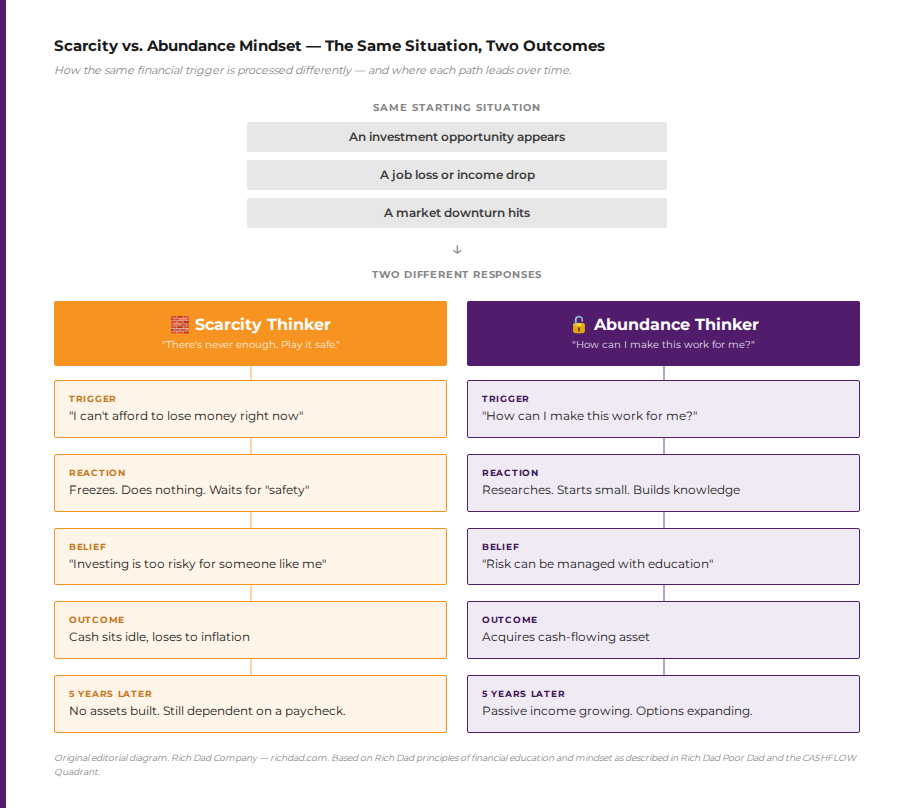

Before the math of financial freedom can work, the mindset has to change. Rich Dad has always taught that there are two ways people see the world of money. Those operating from a scarcity mindset believe there is not enough — not enough opportunity, not enough money, not enough room for everyone to succeed. Fear drives their decisions. They hold onto what they have, avoid risk, and remain stuck in patterns that keep them where they are.

Those operating from an abundance mindset see the world differently. They believe there is enough for everyone willing to learn and act. They are not reckless — they simply do not let fear of loss override the pursuit of opportunity. These are the people who start businesses, make meaningful investments, and build the kind of financial lives that look like freedom from the outside because they genuinely are.

The shift from scarcity to abundance thinking is not a matter of personality. It is a product of financial education — of learning enough about how money works that the fear of it dissolves. When the rules of the game are understood, the game becomes less threatening. And when fear steps back, better decisions move in.

This is one reason Rich Dad places so much emphasis on education before action. The free CASHFLOW Classic game exists partly to build this intuition in a no-risk environment — to let players experience the mechanics of assets, liabilities, income, and expenses until the patterns become instinctive rather than frightening.

Financial freedom vs. financial independence

These two terms are often used interchangeably, but they describe different things. Financial independence is the structural condition: your assets generate enough income to cover your expenses without needing to work. It is measurable and binary — either the cash flow covers the bills or it does not. Rich Dad covers the mechanics of this in detail, including strategies for real estate cash flow, paper assets and options income, and building businesses that generate income without trading time.

Financial freedom is the fuller state. It includes independence, but adds the psychological and behavioral components: the absence of fear-based decision-making, the presence of choices not driven by financial necessity, and the ability to pursue the work, relationships, and experiences that matter most without the override of financial pressure. A person can become financially independent and still be miserable — hoarding wealth, making decisions out of anxiety, and feeling no more free than they did before the assets were acquired. That is not freedom. It is just a more comfortable cage.

The goal here is to have both: the structural condition of passive income exceeding expenses, combined with the internal condition of money no longer being the controlling force in daily life.

How to achieve financial freedom: The Rich Dad Path

Financial freedom is not a destination reached by accident or inheritance. It is built, step by step, through financial education, deliberate asset acquisition, and the consistent application of a few core principles. Here is how Rich Dad’s framework maps the path.

Build financial literacy first

No strategy works without the foundation. Financial literacy means being able to read a personal financial statement, understand the difference between assets and liabilities, distinguish cash flow from capital gains, and recognize how taxes affect different types of income.Rich Dad’s personal finance hub is built around this foundation — covering budgeting, debt strategy, tax planning, and the mechanics of saving versus investing.

Acquire assets that generate cash flow

The engine of financial freedom is cash flow — recurring income from assets that does not require trading time. Rich Dad identifies four asset classes where this can be built: real estate (rental income), paper assets (dividends, options premium), business ownership (earnings that flow without direct daily labor), and commodities. The specific mix depends on individual circumstances, risk tolerance, and level of financial education — but the direction is consistent: acquire income-producing assets, reduce income-consuming liabilities.

Understand how taxes work in your favor

Taxes are one of the biggest levers in the wealth-building equation, and most employees pay the highest effective rates of anyone in the economy. Business owners and investors have access to legal tax advantages — depreciation, entity structuring, capital gains treatment, and more — that dramatically shift how much of each dollar is kept.Rich Dad’s tax education resources and the WealthAbility Show address this in depth. Moving from the Employee or Self-Employed quadrant to the Business Owner or Investor quadrant of the CASHFLOW Quadrant changes not just income — it changes the tax structure entirely.

Use good debt, eliminate bad debt

Debt is not the enemy of financial freedom — bad debt is. Rich Dad’s framework on debt distinguishes between debt that acquires income-producing assets (good debt, which builds freedom) and debt that finances consumption and liabilities (bad debt, which destroys it). Eliminating high-interest consumer debt while strategically using leverage to acquire cash-flowing assets is one of the most effective accelerators on the path to freedom.

Measure progress with the financial statement

Financial freedom can be tracked. The personal financial statement — income, expenses, assets, liabilities — is the instrument. The metric to watch is the ratio of passive income to monthly expenses. When passive income covers 25% of monthly expenses, that is progress. When it covers 50%, the end is in sight. When it crosses 100%, financial freedom has been reached. This is not theoretical — it is a number that moves in measurable increments as assets are acquired and liabilities are reduced.

Financial Freedom and the FIRE Movement

The FIRE movement — Financial Independence, Retire Early — has brought the concept of financial freedom into broader cultural awareness over the past decade. At its core, FIRE advocates living below your means, saving and investing aggressively, and reaching a point where investment returns cover living expenses early in life rather than waiting until traditional retirement age. It shares significant common ground with Rich Dad’s framework, particularly the emphasis on passive income and escaping dependence on a paycheck.

Where Rich Dad’s approach diverges is on the nature of the assets being built. The FIRE movement often relies heavily on index fund accumulation and the 4% withdrawal rule — a strategy that remains capital-gains dependent and subject to sequence-of-returns risk. Rich Dad places greater emphasis on cash flow-generating assets — rental properties, businesses, and income-producing paper assets — that pay out regularly regardless of whether the portfolio is growing or declining. Cash flow does not require selling. It does not depend on a market that cooperates. And for many investors, that distinction matters enormously.

Signs you’re moving towards financial freedom

Financial freedom is not an overnight arrival. It is a progression, and there are clear markers along the way. The following are signs that the path is working:

Your passive income covers at least a portion of your monthly expenses — even $200 a month in rental income or dividends is the system beginning to work.

You make financial decisions based on strategy rather than fear — turning down a poor investment because the numbers do not work, not because the idea is frightening.

Your liabilities are declining while your asset column grows — less consumer debt, more income-producing investments.

You understand your personal financial statement — you know exactly what is coming in, going out, and where every dollar is working or sitting idle.

You have built at least one income stream outside your primary job — a rental unit, a dividend portfolio, a side business generating profit without your constant presence.

Where to begin your journey

The most important first step is not opening an investment account or buying a property. It is education. Without understanding how money works, every investment decision carries more risk than it needs to. Rich Dad offers multiple entry points for that education — all of them designed to build the kind of financial intelligence that makes the path to freedom navigable rather than overwhelming.

Play CASHFLOW Classic for free to develop intuition around assets, liabilities, and the mechanics of financial freedom in a risk-free environment. Explore the Rich Dad Radio Show and StockCast with Andy Tanner for ongoing education in investing, paper assets, and cash flow strategies. Read Rich Dad Poor Dad if the foundational philosophy is still new. And take the Investment IQ assessment to identify the specific gaps in financial knowledge worth addressing first.

Financial freedom is not reserved for the lucky, the high-income, or the already-wealthy. It is built through education, applied consistently over time. The only real barrier is starting — and the only way to fail is not to.

FAQs

In the Rich Dad framework, financial freedom is reached when the monthly cash flow generated by your assets equals or exceeds your monthly living expenses. At that point, money is working for you rather than the other way around, and you are no longer required to trade time for income to sustain your lifestyle.

Financial independence is the structural condition — your assets generate enough passive income to cover your expenses. Financial freedom is broader: it includes the mindset and behavioral shift that comes with no longer being controlled by financial fear or scarcity thinking. You can be financially independent and still be governed by anxiety about money. True freedom requires both the structural reality and the internal state.

No. Financial freedom is about the relationship between income and expenses, not the absolute size of either. A person with modest living expenses and consistent passive income from a rental property or dividend portfolio can be genuinely financially free, while a high earner whose lifestyle consumes every dollar of income is not. Wealth and freedom are related but not the same thing.

There is no universal number, because financial freedom depends on your specific monthly expenses — not a fixed savings target. The Rich Dad formula is simple: when your passive income (from assets like rental properties, dividends, or business income) equals or exceeds your monthly living costs, you are financially free. The path there involves growing that passive income while keeping expenses from expanding at the same pace.

FIRE — Financial Independence, Retire Early — is a movement built around aggressive saving and investing to achieve financial independence well before traditional retirement age. It shares the Rich Dad goal of escaping dependence on a paycheck but typically relies on index fund accumulation and portfolio withdrawal. Rich Dad’s approach places greater emphasis on cash flow-generating assets — real estate, businesses, income-producing paper assets — that pay out regularly regardless of market conditions, reducing reliance on portfolio growth or withdrawal strategies.

Rich Dad identifies four main asset classes for building financial freedom: real estate (rental income), paper assets (dividends, options premium through strategies like covered calls), business ownership (income generated without daily direct labor), and commodities (as an inflation hedge). The right mix depends on financial education level, risk tolerance, and available capital — but the common thread is that all four generate cash flow rather than requiring the sale of an asset to produce income.

Significantly. Employees typically pay the highest effective tax rates, while business owners and investors have access to legal strategies — depreciation, entity structures, capital gains treatment — that reduce the tax burden considerably. Progressing from the Employee quadrant to the Business Owner or Investor quadrant changes not just income potential but the entire tax structure around that income, making each dollar of passive income go further toward covering expenses and accelerating the path to freedom.

Rich Dad recommends starting with financial education before making any investment decisions. Learn to read a personal financial statement, understand the difference between assets and liabilities, and begin distinguishing cash flow from capital gains. The free CASHFLOW Classic game at richdad.com/cashflow/ is one of the best starting points — it builds the intuition around financial mechanics in a no-risk environment. From there, the investing hub at richdad.com/investing/ and the Rich Dad podcast library provide ongoing education across every relevant asset class.