What is the velocity of money?

The term “velocity of money” has two distinct meanings that are worth understanding separately. In macroeconomics, it refers to the rate at which money circulates through an economy — the frequency with which a single dollar changes hands within a given period. The Federal Reserve tracks this metric as a measure of economic health: when velocity is high, money is moving freely, businesses are transacting, and economic output tends to grow.

In the Rich Dad context of personal investing, the velocity of money means something more actionable: the speed at which an investor recovers original capital from an investment, freeing it to be redeployed into new assets. The faster capital cycles back into productive use, the faster wealth compounds. As Jay Vasantharajah, an entrepreneur and private equity investor, describes it: velocity of money in investing is about the return OF capital — not just the return ON capital. Getting principal back fast, while retaining ongoing upside from the original asset, is the foundation of the strategy.

Think of money like an electrical current. It is a powerful force — but only while it is moving. The moment it stops, it begins to lose potency. That is exactly what happens when money sits in a savings account, a low-yield 401(k), or any vehicle that is designed to hold capital rather than deploy it.

Savers are losers: The math that changes everything

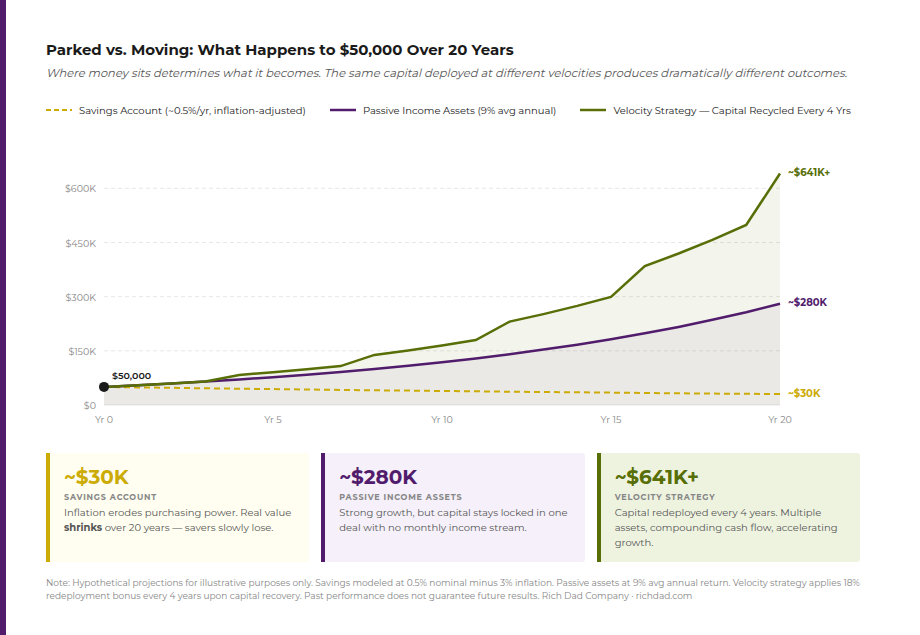

Robert’s rich dad famously declared, “Savers are losers.” It was not an insult — it was an economic observation. In a world where the average high-yield savings account earns under 5% nominal and inflation has averaged 3–4% annually over recent decades, money sitting in savings is, in real purchasing-power terms, slowly evaporating.

The problem is compounded for anyone following the conventional advice to park retirement funds in a 401(k) and wait. Markets can and do crash — sometimes eliminating decades of paper gains in a matter of months. There is no monthly cash flow. There is no early access without penalty. And when the money finally comes out, it is taxed as ordinary income — the highest-taxed income type in the U.S. tax code. This is not a pathway to financial freedom. It is a pathway to financial dependence on a system that was not designed with the investor’s best interest in mind.

The fundamental truth that poor dad did not understand — and that rich dad grasped intuitively — is that inflation and low interest rates act as an invisible tax on savers. The best financial decision for those who want to build real wealth is not to save money, but to immediately deploy it into assets that generate returns above the inflation rate and produce monthly income along the way. Explore more on this in Rich Dad’s guide to why savers are losers. The poor mindset of saving money

How the poor, middle class, and wealthy use money differently

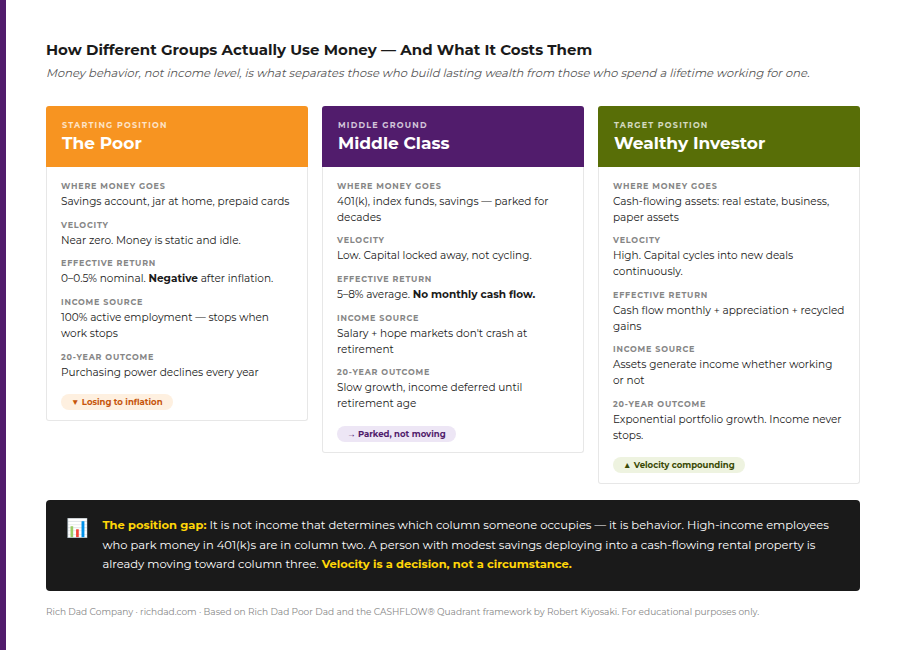

Understanding the velocity of money begins by recognizing that most people fall into one of three categories based on how they deploy their capital — and that the differences compound dramatically over time.

The poor: Money at a standstill

The poor, as Rich Dad defines it, are those who keep their money in the lowest-velocity vehicles: savings accounts, under mattresses, or prepaid cards. There is no return above inflation. There is no asset accumulation. Each dollar parked is, in real terms, a declining dollar. The only income is from active employment — and income stops the moment work stops.

The middle class: Money parked for decades

The middle class takes better advice — but still follows the conventional playbook. They park their savings in 401(k) accounts, index funds, and mutual funds. The returns are better than a savings account, but there are three critical problems: there is no monthly cash flow, the money is locked away for decades, and market crashes can destroy years of growth without warning. This is the strategy of deferred gratification — work harder now and hope the market cooperates. Rich Dad addresses this directly in its analysis of 401(k) problems and alternatives.

The wealthy investor: money in constant motion

Sophisticated investors — those on the right side of the CASHFLOW® Quadrant — keep their money moving through cash-flowing assets. Real estate, businesses, and paper assets such as dividend-paying stocks or options strategies generate income every month. When that income and capital are redeployed into new investments, the cycle accelerates. Wealth compounds not just from returns but from the frequency of compounding cycles. This is the velocity advantage.Savers are losers: The math that changes everything

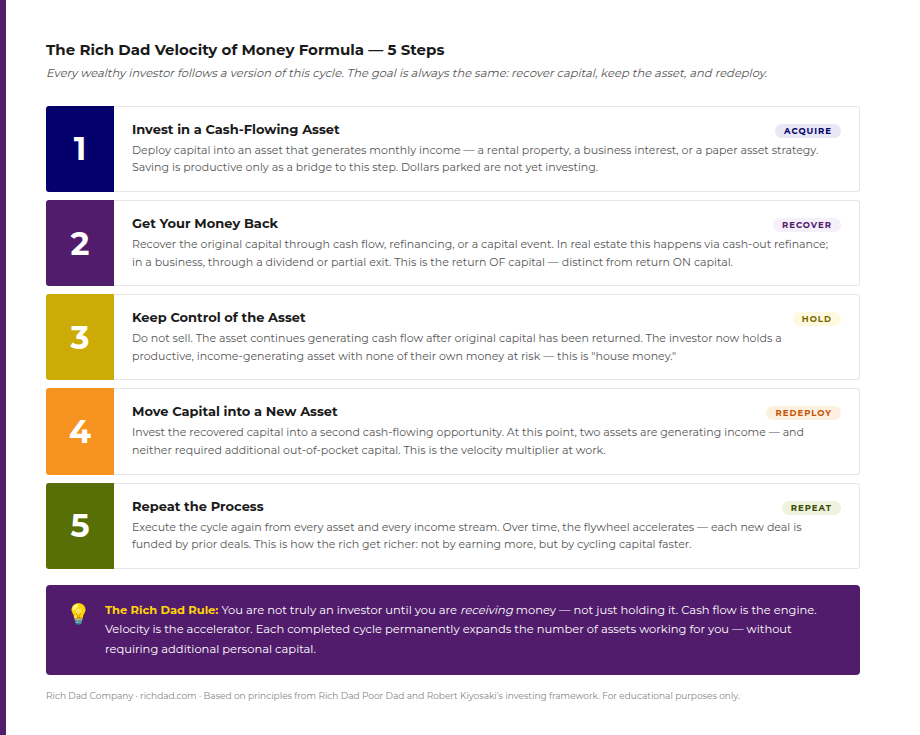

The 5-Step Velocity of Money Formula

Velocity of money is not a theory — it is an executable formula. Rich Dad’s investing framework reduces it to five repeatable steps that any investor can begin applying today. The key insight embedded in every step is this: wealth-building is not about how much you invest, but how many times you can put the same capital to work.

- Invest in a cash-flowing asset

Deploy available capital into an asset that generates income: a rental property, a business interest, or a paper asset strategy like covered calls. Saving is useful only as a bridge to this step — dollars parked are not investing.

- Get your money back

Recover the original capital through cash flow, a refinance, or a capital event. In real estate, this often happens through a cash-out refinance after a property appreciates in value. In private equity, it may happen through a dividend recap or partial sale. This is the return OF capital — the step most conventional investors never reach.

- Keep the asset

Do not sell. The asset continues to generate cash flow after original capital has been returned. This is where the “house money” concept becomes reality — the investor now holds a productive asset with none of their own capital at risk.

- Redeploy to a new asset

Take the recovered capital and acquire a second cash-flowing investment. At this point, two assets are generating income — and neither required additional out-of-pocket capital. This is the velocity multiplier at work.

- Repeat the process

Execute the cycle again from every asset and every income stream. Over time, this flywheel creates exponential wealth growth — not because any single investment outperforms, but because capital is never idle.How the poor, middle class, and wealthy use money differently

Playing with house money: The professional investor’s edge

Professional gamblers in Las Vegas use a specific strategy: as soon as their winnings exceed their original stake, they stop using their own money and bet exclusively with the casino’s money — their winnings. They call this “playing with house money.” The downside risk to their personal capital is effectively eliminated, while the upside continues without limit.

Professional investors apply the same logic. Once an investor has recovered original capital from an investment — through refinancing, cash flow, or a partial exit — the remaining exposure in that deal is entirely funded by house money. A market correction, an occupancy dip, or a temporary earnings decline no longer threatens personal wealth. The investor can weather volatility with composure because the real money was already safely extracted and redeployed.

This is one of the reasons Robert Kiyosaki and his real estate advisor Ken McElroy have repeatedly partnered on large apartment investments: improve the property, raise rents, refinance to extract equity, keep the building, and repeat with the extracted capital. The result is not just one great investment — it is a portfolio of cash-flowing assets, most of which are generating returns on house money. Learn more about this approach in Rich Dad’s guide to real estate investing and the BRRRR method.

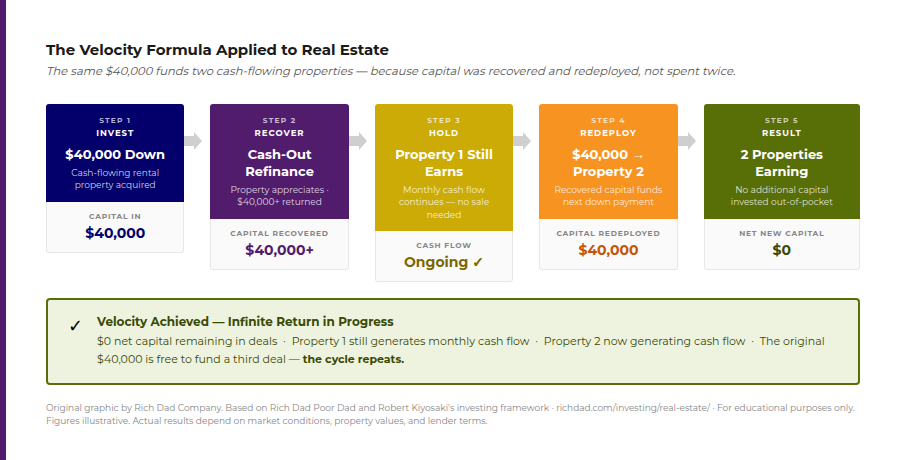

Real estate and the velocity of money in practice

Real estate is one of the most powerful asset classes for applying the velocity of money formula, because it offers multiple mechanisms for capital recovery: monthly rental income, property appreciation, tax-advantaged depreciation deductions, and the ability to refinance and extract equity without triggering a taxable event.

Consider a simplified example. An investor acquires a rental property for $200,000, putting $40,000 down. Over several years, the property appreciates to $280,000 and rents have increased to cover all operating expenses plus cash flow. A cash-out refinance at 75% LTV yields $210,000 — returning the original $40,000 down payment and providing additional capital beyond that. The property continues to produce cash flow. The recovered capital goes into the next deal.The 5-Step Velocity of Money Formula

This is not theoretical. It is the systematic strategy employed by successful real estate investors across every market cycle. The BRRRR method — Buy, Rehab, Rent, Refinance, Repeat — is a structured codification of this exact velocity principle applied to value-add real estate. The same logic applies to paper assets and options strategies, where covered calls and cash-secured puts generate monthly premium income that can be reinvested into new positions.

What a falling velocity of money means for savers

The Federal Reserve tracks the velocity of money at a national level using the M2 money supply. In the decades following the 2008 financial crisis, the velocity of M2 has declined sharply, hitting record lows during and after the COVID-19 pandemic. This means that, at a macro level, money is circulating less frequently through the economy — partly because households and institutions are holding cash rather than deploying it into productive activity.

For savers, this macro trend is particularly damaging. Quantitative easing — the Federal Reserve’s policy of expanding the money supply — has historically suppressed savings rates and bond yields, eroding the returns available to those who park capital in conventional vehicles. The rich, who understand how to move money, benefit from low interest rates by borrowing cheaply to acquire assets. The middle class, who park money in savings accounts and bonds, are squeezed between near-zero yields and persistent inflation.

The macro and personal lessons converge on the same conclusion: in an environment of monetary expansion and suppressed yields, the only winning strategy is to own productive assets that generate income regardless of interest rate policy.Real estate and the velocity of money in practice

Two major benefits of high-velocity investing

1. Dramatically reduced risk

When an investor has recovered original capital and is generating returns on house money, the risk profile of that investment fundamentally changes. A bad year, a vacancy, or a market correction affects the income stream — but it does not threaten the principal, because the principal is no longer in the deal. This is the professional investor’s greatest advantage: the ability to hold assets through cycles without the psychological or financial pressure that forces amateur investors to sell at the worst possible time.

2. Compounding at a faster pace

Conventional compounding grows wealth by reinvesting returns on a single pool of capital. Velocity compounding multiplies the number of income-generating assets over time. Two properties generating cash flow compound faster than one. Four compound faster than two. As each cycle completes and new assets are added, the income base expands — and the pace of expansion accelerates. This is the flywheel effect: slow to start, but increasingly powerful as momentum builds.

This is how billionaires reach a point where they genuinely cannot give money away fast enough. The velocity of their capital — moving through businesses, investments, and financial structures — generates income faster than it can be spent or donated. The principle is the same at every level of wealth. Starting small matters less than starting correctly.

Start increasing your own velocity of money

The velocity of money formula is not reserved for those who already have substantial capital. It begins with any amount of money put to productive use. The first step is understanding the difference between assets and liabilities — and ensuring every dollar saved is working toward acquiring a cash-flowing asset rather than accumulating in a low-yield vehicle.

Rich Dad recommends beginning with financial education. Understanding the four asset classes — real estate, business, paper assets, and commodities — and which type of investment aligns with existing knowledge and resources is the foundation of every wealth-building journey. The CASHFLOW® Quadrant provides the framework for understanding where income currently comes from, and where it needs to move to achieve financial freedom.

From there, the path is the formula: invest, recover, keep, redeploy, repeat. Each completed cycle does not just increase net worth — it permanently expands the income base. That expanding base, consistently recycled, is how ordinary investors achieve extraordinary outcomes.

For those just beginning, playing CASHFLOW Classic for free online is one of the most effective ways to internalize the velocity formula without putting real money at risk. The game simulates the exact cycle described above — and every round builds the investor instincts needed to execute it in real life.Two major benefits of high-velocity investing

The defining financial principle

The velocity of money is the defining financial principle that separates those who build lasting wealth from those who spend decades trading time for a paycheck. It is not about earning more — it is about deploying capital more intelligently, recovering it faster, and never letting it sit idle when it could be generating income.

Rich dad’s lesson was simple and devastating in its honesty: savers are losers not because they are bad people, but because they are playing the wrong game. The right game is velocity — keeping money moving through assets that produce cash flow, recovering capital quickly, and using it to acquire the next asset. Done consistently, over time, this is how the rich get richer. And it is available to anyone willing to learn the rules.

Start with financial education. Start with the CASHFLOW game. And start asking not how much money you have saved — but how fast it is moving.

FAQs

The velocity of money is the speed at which money cycles through productive investments. In personal finance, it refers to how quickly an investor recovers original capital from one investment and redeployes it into another — keeping money working rather than sitting idle.

Wealthy investors use cash-flowing assets that return capital quickly — through rental income, business distributions, and refinancing. Rather than parking capital for decades and hoping for appreciation, they recover their investment basis and redeploy it into new deals. This multiplies the number of income-generating assets over time without requiring additional out-of-pocket capital.

The BRRRR method — Buy, Rehab, Rent, Refinance, Repeat — is a direct application of the velocity of money formula to real estate. Each cycle recovers original capital through a cash-out refinance while keeping the property and its cash flow intact. The recovered capital then funds the next acquisition, accelerating portfolio growth without scaling up personal capital contributions.

Saving is a bridge, not a destination. Accumulating capital with the explicit goal of deploying it into cash-flowing assets is the correct use of a savings discipline. The problem arises when saving becomes the end strategy rather than the means — when capital accumulates in low-yield accounts for years without ever being put to productive use. Rich Dad’s philosophy is to save intentionally, deploy quickly, and never let capital sit idle longer than necessary.

When the Federal Reserve expands the money supply through quantitative easing, it suppresses yields on savings accounts and bonds — making the conventional “save and park” strategy even less effective. At the same time, low interest rates make borrowing cheap for investors who understand leverage. Sophisticated investors borrow at low rates to acquire appreciating, cash-flowing assets while savers earn near-zero returns. The macroeconomic environment consistently rewards velocity over accumulation.

Yes. Options strategies such as covered calls and cash-secured puts generate premium income that can be reinvested into new positions — creating a velocity cycle in the stock market. Dividend-reinvestment strategies function similarly. The key is that capital must be actively deployed and its returns reinvested rather than left as idle cash in a brokerage account. Andy Tanner’s StockCast podcast covers these paper asset strategies in depth.

The fastest path begins with financial education — specifically, learning to identify cash-flowing investment opportunities within one’s existing knowledge base. Real estate is often the most accessible starting point because leverage is readily available, the asset class is well understood, and the cash-out refinance mechanism provides a reliable vehicle for capital recovery. Starting with a small rental property and executing one complete BRRRR cycle is one of the most effective ways to internalize the velocity formula through direct experience.