Is the debt worth it?

When Robert Kiyosaki was young, his poor dad counseled a clear path: go to school, earn a degree, get a good job. At the time, the cost of that advice was relatively manageable. Today, the numbers tell a very different story.

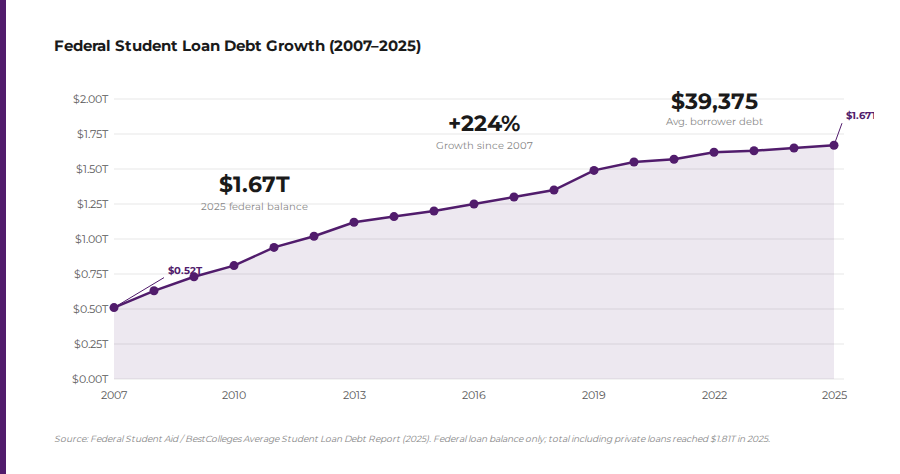

According to the Federal Reserve, total student loan debt in the United States stands at $1.8 trillion as of 2025. The average federal student loan balance per borrower is approximately $39,375 — nearly twice the average from 2008. Half of all bachelor’s degree recipients graduated with student debt in 2022–23, and nearly 20% of borrowers report being behind on payments. The debt follows people well into middle age: borrowers between 35 and 49 collectively carry the largest share of student loan debt in the country.

And what does that investment buy? According to the Federal Reserve Bank of New York, 41% of recent college graduates are underemployed — working in roles that don’t require a four-year degree. That statistic alone should prompt every family to ask a harder question: not just how to pay for college, but whether the credential is worth the price.

The AI Factor Changes Everything

For decades, the conventional wisdom held that white-collar, knowledge-based work was safe from automation. Trade jobs might be disrupted, the thinking went, but the desk jobs a college degree unlocks were secure. Artificial intelligence has dismantled that assumption.

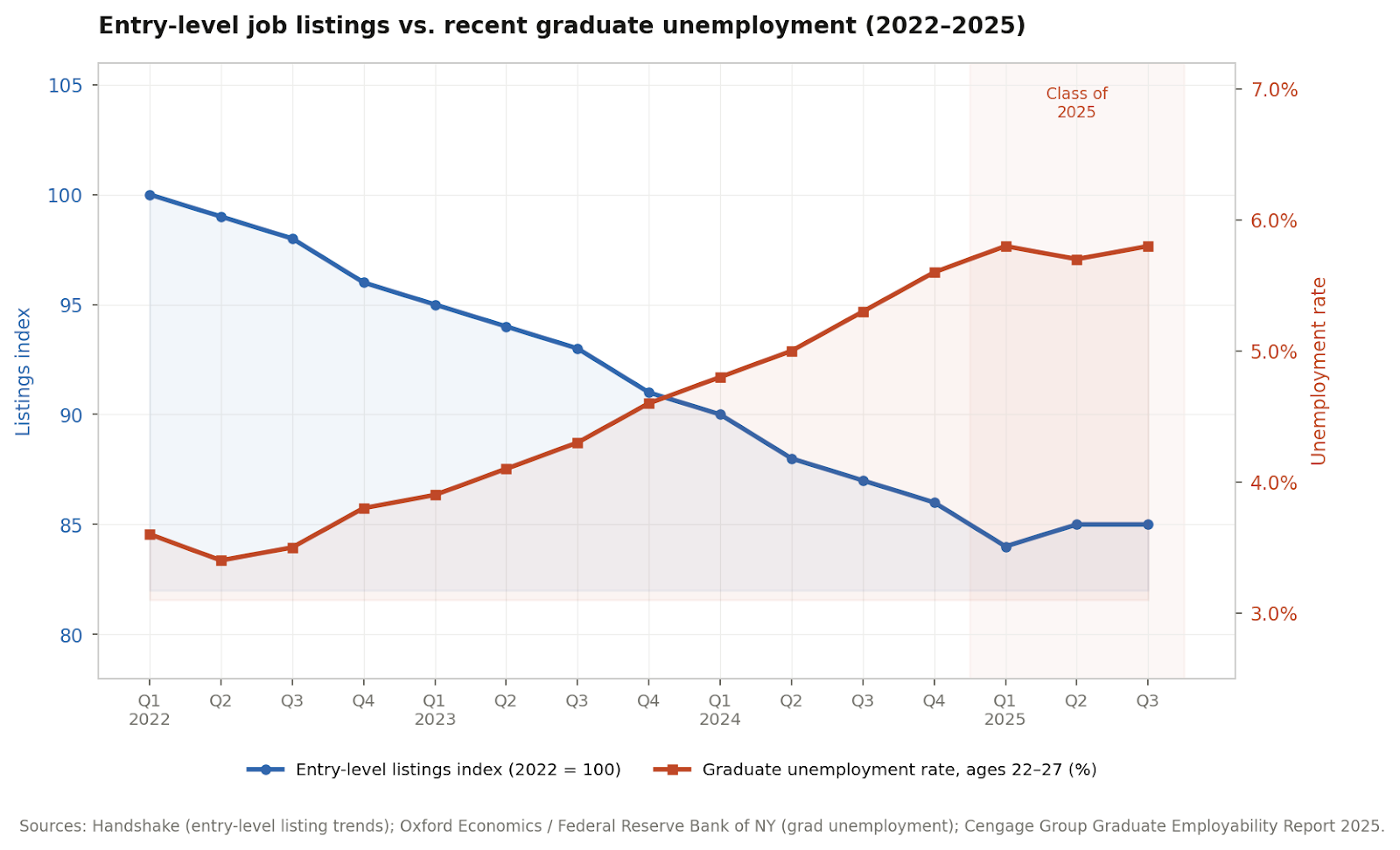

Research from Oxford Economics found that the unemployment rate for recent college graduates rose faster than the national rate through 2025, with AI absorption of entry-level tasks identified as a primary cause. According to career platform Handshake, job listings for entry-level corporate roles declined 15%, while applications per posting surged 30%. Just 30% of the Class of 2025 secured full-time employment in their field, down from 41% the prior year.

A 2025 survey by IDC and Deel found that 66% of global enterprises plan to cut entry-level hiring due to AI adoption. The World Economic Forum’s Future of Jobs Report 2025 warned that 40% of employers expect to reduce staff where AI can automate tasks. The first rung of the career ladder — the one that a college degree was supposed to guarantee — is being removed.

This does not mean the end of opportunity. It means the end of the assumption that a $40,000 credential automatically leads to employment. The five alternatives below were sound financial decisions before AI reshaped the job market. They are even more compelling now.

5 Things to Do Instead of College

1. Work to Learn — Not Just to Earn

Robert Kiyosaki graduated from the U.S. Merchant Marine Academy and was immediately offered a well-paying career in the shipping industry. He turned it down to take a sales job at Xerox — not for the paycheck, but for the skill. He knew that sales mastery would power every business he would ever build. That single decision proved more financially valuable than any classroom course ever could have.

The principle holds today. The most valuable education often comes from working in a role specifically chosen for what it teaches, not for what it currently pays. Someone interested in real estate investing might take a position at a property management firm to understand operations from the inside. Someone interested in entrepreneurship might work in sales or business development to develop the foundational skills every successful business owner needs.

The question to ask before accepting any position is not just “what does it pay?” but “what will I know at the end of this that I didn’t know at the beginning?” Skills and relationships built through purposeful, intentional work create more wealth — and carry far less debt — than four years of tuition-funded coursework.

2. Pursue Non-Traditional Financial Education

The landscape of accessible, high-quality education has changed dramatically. A person today can learn investing, accounting, coding, and business strategy from world-class instructors at a fraction of the cost of a university course — through platforms like Coursera and Udemy or through the financial education resources that the Rich Dad library has been developing for decades.

What most traditional education still does not teach is financial intelligence: how money actually works, how assets differ from liabilities, how the wealthy use debt strategically, and how the tax code rewards investors and business owners rather than employees. Understanding the CASHFLOW Quadrant — Robert Kiyosaki’s framework for how people earn income, from Employee to Business Owner to Investor — provides a financial map no standard college curriculum offers.

Non-traditional financial education also includes learning from mentors, reading foundational texts, attending financial seminars, and building a personal advisory team of accountants, attorneys, and advisors who understand wealth-building. This kind of education compounds over time. The earlier it begins, the greater the advantage.

3. Begin Investing

If the average four-year college experience costs more than $100,000 when accounting for tuition, housing, and living expenses, the relevant question is: what else could that capital do?

The Rich Dad philosophy draws a clear line between good debt and bad debt. Bad debt takes money out of the pocket. College debt — which finances a credential rather than a cash-flowing asset — fits that definition for many borrowers. Good debt is used to acquire assets that produce income. Someone who enters the workforce and directs even a portion of what they would have spent on tuition toward real estate or stocks and paper assets can build a substantially different financial position over a decade than a peer who starts career life carrying $40,000 in student loans.

Investing does not require large amounts of capital to start. It requires education, patience, and the discipline to act on knowledge. For those who want to understand investing before committing real money, the CASHFLOW game — developed by Robert Kiyosaki and Kim Kiyosaki — provides a real-world financial simulation covering cash flow, assets, liabilities, and the mechanics of escaping the rat race.

4. Start a Business

Some of the most financially successful entrepreneurs in history left college before finishing their degrees. This is not a universal template, but it illustrates a truth the Rich Dad philosophy has always emphasized: the skills required to build a business cannot be fully taught in a classroom.

Entrepreneurship is the quadrant of the CASHFLOW framework where income potential and tax advantages are maximized simultaneously. Business owners can deduct legitimate operating expenses — vehicles, equipment, travel, and more — before they pay taxes, while employees pay taxes first and live on what remains. That difference in tax treatment represents a structural financial advantage that compounds over an entire career.

Starting a business also develops financial skills that no degree program matches: reading profit-and-loss statements, managing cash flow, negotiating contracts, understanding customers, and building systems that work without the owner being constantly present. For anyone with a viable idea or skill set, beginning that business now — rather than postponing it four years and $40,000 in debt — is almost always the wealthier path.

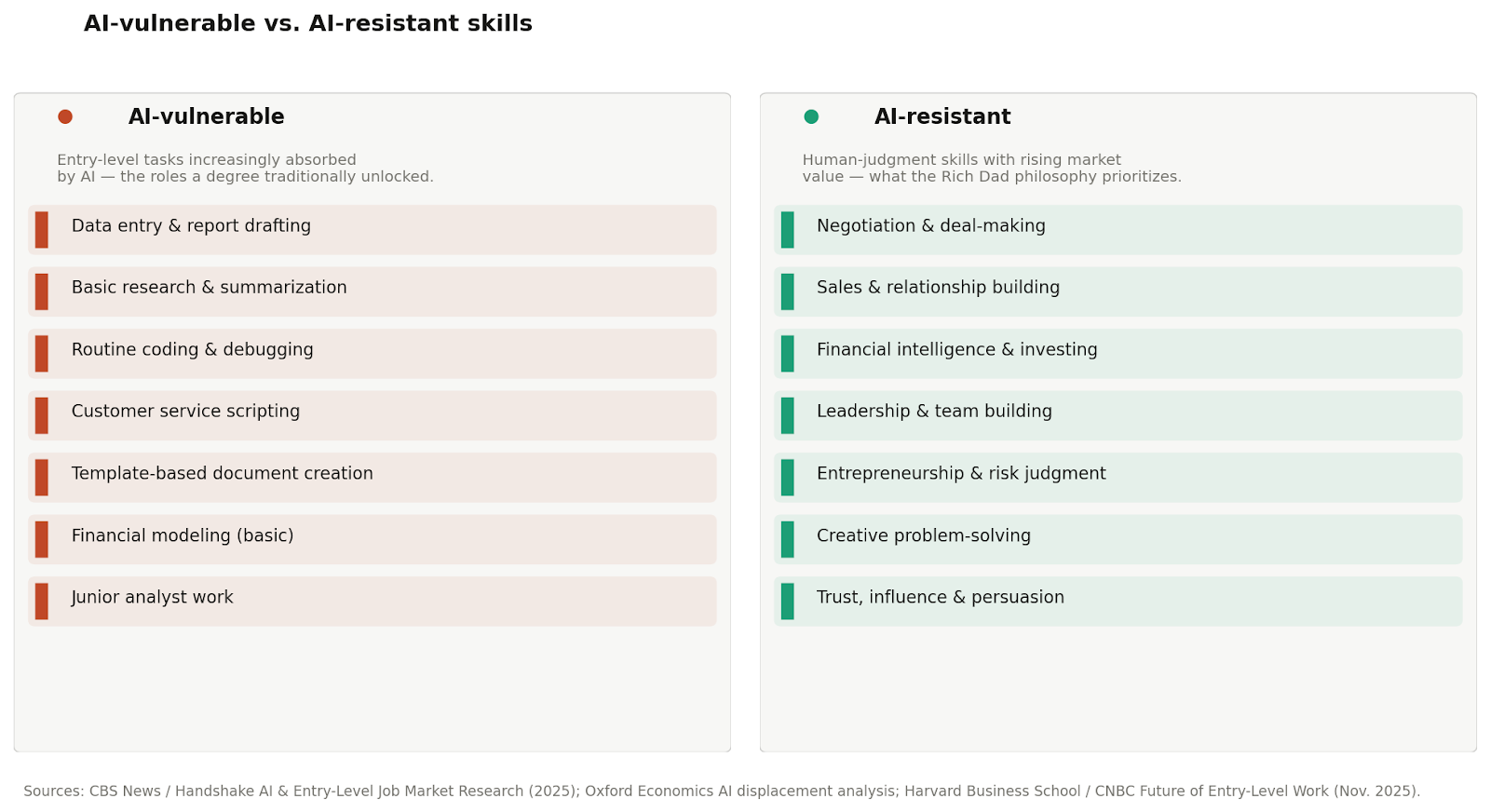

5. Build Skills AI Can’t Replace

Artificial intelligence is absorbing the entry-level, task-based work that once served as the on-ramp for college graduates. Data entry, basic research, drafting routine documents, generating reports, even early-stage coding — these categories of work are increasingly handled efficiently and cheaply by AI tools. For the graduate who borrowed $40,000 to earn a degree preparing them for exactly these roles, the job market math is increasingly unfavorable.

The skills AI cannot easily replicate are those requiring human judgment, relationship-building, and contextual decision-making: negotiation, sales, leadership, financial literacy, and the ability to understand people well enough to lead, persuade, or serve them effectively. These are also, not coincidentally, the skills the Rich Dad philosophy has always placed at the center of financial education.

Building AI-resistant skills does not require a four-year institution. It requires intentional practice, quality mentorship, and the willingness to take on challenges that develop judgment rather than simply technical competency. Those who invest in this kind of development now will be positioned on the right side of the AI divide — not among those whose credentials have been commoditized, but among those whose capabilities cannot be automated.

The Real Education Is Financial Intelligence

The question of whether to attend college has never been purely academic — it has always been financial. A degree can open doors, but it can also close them, particularly when student debt becomes a decade-long anchor on every financial decision that follows. The five alternatives in this article are not shortcuts. They require education, discipline, and the willingness to take a different path than the one conventional wisdom prescribes.

The Rich Dad philosophy does not tell people to avoid learning. It tells them to be selective about what they learn and strategic about how they invest their resources — including their time. Whether the goal is financial freedom through real estate, building a business, or developing judgment that AI cannot replicate, the greatest asset any person can possess is financial intelligence. That education is available to anyone willing to pursue it, degree or no degree.

FAQs

For certain fields — medicine, law, engineering — a degree remains a practical and often legally required credential. Outside those specific paths, the answer depends on an honest cost-benefit analysis. With average student loan debt approaching $40,000 and 41% of recent graduates underemployed, the automatic assumption that any degree in any field is worth any cost no longer holds. The Rich Dad framework asks a simple question: does this investment generate a return, or does it drain one?

The paths outlined above — working to learn, pursuing financial education, investing, starting a business, and building AI-resistant skills — all create financial opportunity without requiring a four-year credential. The key starting point is financial education that helps identify which path aligns best with a person’s skills, goals, and available resources.

Yes, but it requires education first. The distinction between good debt and bad debt is central here. Using capital or manageable debt to acquire cash-flowing assets is fundamentally different from borrowing to fund four years of education with uncertain returns. Understanding that distinction — and acting on it early — is one of the most financially impactful decisions a young person can make.

AI is absorbing the entry-level roles that a college degree traditionally unlocked. Research from Oxford Economics and Handshake shows entry-level job listings declining significantly while graduate unemployment rises. This strengthens the financial case against debt-funded degrees and shifts the advantage toward skills, entrepreneurship, and investing — none of which require a four-year credential to begin.

The entire Rich Dad philosophy is built on the premise that schools do not teach financial intelligence. Understanding assets versus liabilities, cash flow over capital gains, the strategic use of debt, and the CASHFLOW Quadrant are all frameworks developed outside of — and often in direct opposition to — what conventional education teaches about money. These principles are explored across richdad.com and in Robert Kiyosaki’s books and courses.