Error: Campaign not found.

Why conventional investing rules fall short

The standard playbook for building wealth through investing — save diligently, maximize 401(k) contributions, buy diversified mutual funds, and stay the course — is not inherently wrong. But it is incomplete. It is a strategy built around accumulation rather than cash flow, and it carries a built-in assumption that most people will accept a lower standard of living in retirement in exchange for a finite pool of savings.

According to Grant Thornton’s tax planning analysis, the top marginal rate on ordinary income — the kind most employees earn — stands at 37%, while the top rate on long-term capital gains and qualifying dividends is just 20%. Business owners and sophisticated investors who structure their income correctly operate in an entirely different tax environment. The rules of investing for the wealthy are not the same rules being taught in mainstream financial media, and Rich Dad’s seven principles reflect that gap.

The 7 rules of investing

These rules for investing are not a get-rich-quick scheme. They are a framework for thinking about money differently — starting with the most fundamental shift of all.

Rule 1: Adjust your money mindset

The first and most important of all the rules for investing has nothing to do with stocks, real estate, or asset allocation. It has to do with what a person believes about money and how it works. Without the right mindset, every other rule is impossible to apply.

Rich dad identified a fundamental difference between how the poor and middle class are taught to think about money and how the wealthy actually operate. The conventional instruction passed down to most families sounds like this: “Go to school, get a good job, work hard, and save money. That will make you rich.”

Rich dad’s instructions were different: “Learn how money works, create good jobs, have money work hard for you, and invest in cash-flowing assets. That will make you rich.”

The difference between these two worldviews is not trivial. The first produces employees who trade time for income and pay taxes before they ever see their money. The second produces investors who use pre-tax dollars, reduce their taxable income through business structures, and build assets that generate income without requiring their daily presence. Beginning to see money the way the wealthy see it — as a tool to be deployed rather than a reward to be saved — is the prerequisite for every rule that follows.

Developing this mindset is an ongoing process. Rich Dad’s core curriculum, including Rich Dad’s Guide to Investing, is built around exactly this transformation — changing not just what someone does with money, but what they believe is possible.

Rule 2: Know what kind of income you’re working for

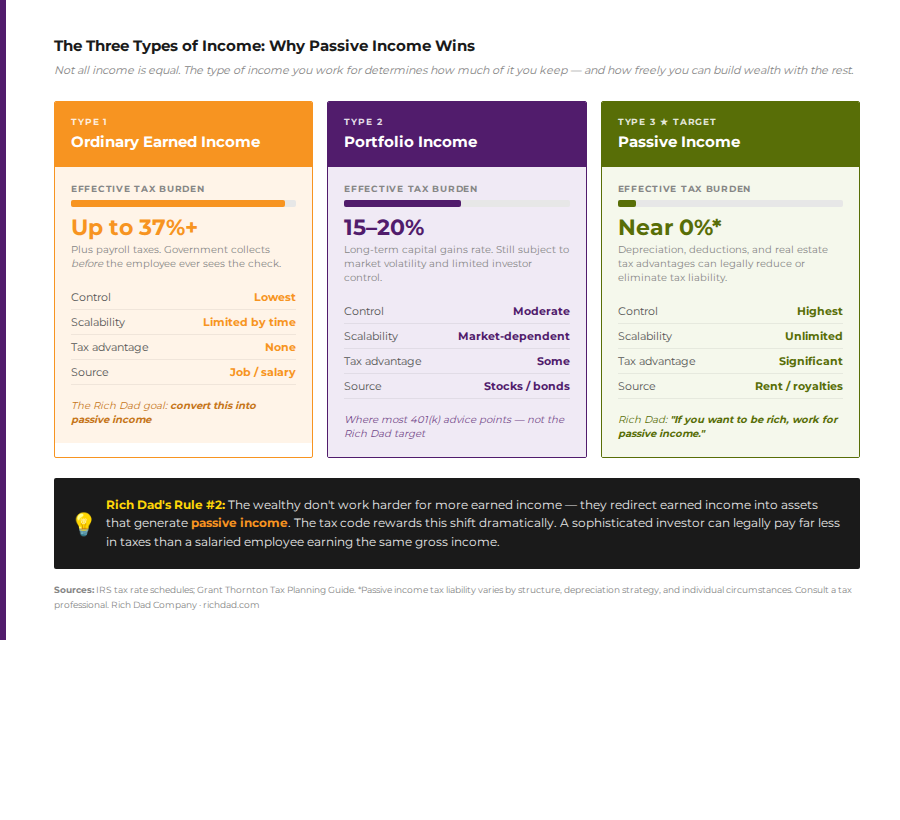

One of the most powerful rules for investing that most people never learn is that not all income is equal. Rich dad taught that there are three types of income, and they are taxed very differently — which means their wealth-building potential is dramatically different as well.

Ordinary earned income

This is the income most people know. It comes from a job — a salary, hourly wage, or self-employment. It is the most heavily taxed type of income, with the government collecting before an employee receives a single dollar. Earned income is also the most fragile: it stops the moment a person stops working. According to the IRS tax code structure, a top earner on ordinary income can face a marginal rate of up to 37%, plus payroll taxes — a structural disadvantage that no amount of frugality can overcome.

Portfolio income

Portfolio income comes from paper assets — stocks, bonds, mutual funds, and similar instruments. It is the second-highest taxed income type, and while it receives somewhat more favorable treatment than earned income (long-term capital gains and qualified dividends are taxed at lower rates), it still offers limited control. The investor is subject to market volatility, fund manager decisions, and macro-economic conditions that no individual can influence.

Most financial advisors building conventional investment plans focus entirely on portfolio income — 401(k) accounts, IRAs, index funds. These can be useful tools, but they are not the foundation on which financial freedom is built, because they are still fundamentally dependent on market performance and the eventual drawdown of a finite balance.

Passive income: The investor’s true target

Passive income is the goal. It comes from real estate rental income, business distributions, royalties, and other sources that produce cash flow whether or not the owner is actively working. It is the lowest-taxed income type — often benefiting from depreciation, deductions, and other provisions that reduce or eliminate tax liability entirely. More importantly, it is the only income type that is truly scalable without trading more time.

Rich dad’s instruction was unambiguous: “If you want to be rich, work for passive income.” That single sentence reorients an entire investment strategy. Instead of asking “how do I earn more salary?” a financially educated investor asks “what assets can I acquire that will generate cash flow this month?”

Rule 3: Convert ordinary income into passive income

Understanding that passive income is the goal is only half of the equation. The other half is knowing how to get there from wherever a person starts — which, for most people, is earning ordinary income from a job.

Rich dad illustrated this with a simple diagram: the income statement. Money comes in as earned income. The investor’s job is to redirect as much of that money as possible into assets that generate passive income — so that each dollar in the first column creates a stream of dollars in the second column that do not require additional hours of work.

In practical terms, this means treating investment costs as the most important expense — not a discretionary line item to be funded after everything else. Rich dad called this paying yourself first: before mortgage, before groceries, before any other obligation, money is directed into income-producing assets. When a person receives a raise or bonus, the conventional advice is to increase 401(k) contributions or save more. Rich Dad’s answer is to convert that new money immediately into passive income — to buy a cash-flowing asset that will generate returns indefinitely, rather than depositing it into a vehicle that depends on market performance and eventual depletion.

The process is not instantaneous. Building a portfolio of cash-flowing assets takes time, financial education, and deliberate decision-making. But the direction is clear and consistent: every additional dollar of earned income is a potential seed for passive income, and every passive income stream acquired is a permanent step toward financial freedom.

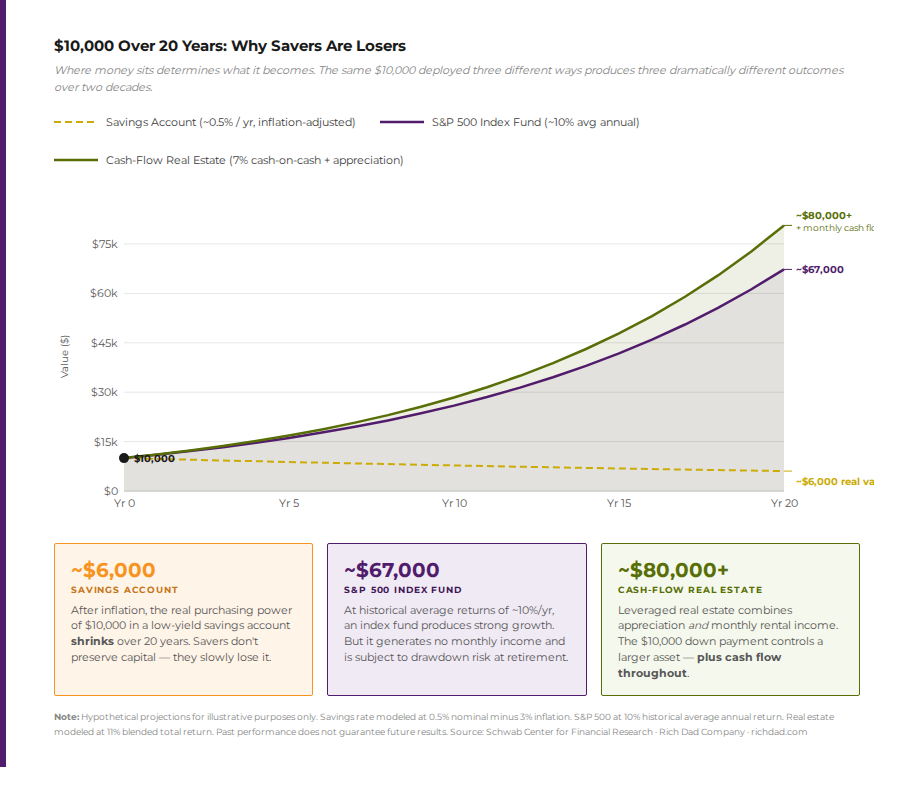

Rule 4: Savers are losers; spenders are winners

Of all seven rules for investing, this one generates the most resistance. It runs counter to everything most people were taught. But it is one of the most important concepts in financial education — and one of the most misunderstood.

Saving money in a low-yield account is not a wealth-building strategy. It is a slow-motion loss. Inflation erodes the purchasing power of savings year after year. Taxes reduce returns on interest income. Hidden fees in retirement accounts compound the damage over decades. The conventional wisdom that diligent saving equals financial security is built on an economy that no longer exists — one where savings accounts paid meaningful interest and the dollar held its value over time.

Rich dad’s point is not that spending is inherently virtuous — it is that money must move to grow. “Money is not backed by anything. It is a currency, which, like a current of electricity, is always moving.” The investors who build wealth are those who understand where money is flowing in the economy and move their capital accordingly — into assets that capture that flow. The savers who hoard cash are not protecting their wealth; they are watching it erode.The implication for practical investing rules is significant: the goal is not to save money, but to deploy it. Deployed into the right assets, money generates income, builds equity, and compounds over time. Sitting in a savings account, it loses ground to inflation daily. For more on this concept, explore Rich Dad’s thinking on why savers lose in today’s economy.

Rule 5: The investor is the asset or the liability

A common misconception about investing rules is that they center on which assets to choose. In reality, one of the most fundamental rules for investing is about the investor themselves. The quality of an investor’s decisions — not the quality of the market — determines outcomes.

Rich dad said: “I have seen investors lose money when everyone else is making it. In fact, a good investor loves to follow behind a risky investor because that is where the real investment bargains can be found!”

What separates a profitable investor from one who consistently loses is financial intelligence — the ability to evaluate deals, understand risk, read financial statements, identify cash-flowing assets, and recognize when something is overpriced. A person with a low financial IQ who purchases an investment property without understanding vacancy rates, maintenance costs, or local rental markets can lose money in the same environment where an educated investor generates strong monthly cash flow.

This rule has a direct implication for where beginners should start: invest in financial education before investing in assets. Start small. Build real experience through real transactions, learn from mistakes, and increase deal size as knowledge grows. Rich Dad’s CASHFLOW® board game was designed specifically to simulate this progression — giving investors a risk-free environment to practice evaluating deals, managing cash flow, and thinking like a sophisticated investor before real money is at stake.

The investor is not a passive participant in the outcome of any investment. The investor is the determining variable. And that means financial education is not a luxury — it is the most important investment anyone can make.

Rule 6: Good deals attract money

One of the most liberating of all the rules for investing — especially for those who worry they don’t have enough capital to get started — is this: finding a genuinely great deal is harder than raising the money to fund it.

Rich dad put it directly: “If you are prepared, which means you have education and experience, and you find a good deal, the money will find you or you will find the money.”

This principle — often called OPM, or Other People’s Money — reflects how sophisticated investors actually operate. Joint ventures, private lending, investor partnerships, and creative deal structures allow a knowledgeable investor to fund acquisitions without using all of their own capital. Wealthy investors actively seek other smart investors to back well-structured deals, because a 10% return on someone else’s money is better than no deal at all.

For beginning investors, this rule serves a motivational function as well. The obstacle is rarely capital. The obstacle is preparation — developing enough knowledge and deal-evaluation skill that when a true opportunity appears, the confidence and credibility to act on it are already in place. Focus on the deal first. The money follows preparation.

Rule 7: Learn to evaluate risk and reward

The seventh and final rule for investing is the one that ties all the others together: the ability to evaluate risk and reward accurately. Every investment involves risk. The question is never whether risk exists but whether the potential reward justifies that risk given the investor’s current knowledge, preparation, and financial position.

Rich dad illustrated this with a memorable example. Imagine a nephew who wants $25,000 to open a burger stand with no experience. The risk is high; the reward potential is limited. Now imagine the same nephew — but he has spent 15 years as a vice president at a major burger chain, and is launching a concept he knows deeply, seeking just 5% of the company for $25,000. The risk is the same dollar amount. The reward potential is vastly different. The ability to see that distinction is what separates a sophisticated investor from an uninformed one.

Evaluating risk and reward is a learnable skill. It requires understanding cash flow analysis, market conditions, exit strategies, and the specific dynamics of any asset class being considered. It also requires self-awareness — knowing where gaps in knowledge exist and either filling them through education or bringing in advisors who can fill them.

The risk isn’t the investment. The risk is the investor who doesn’t know what they’re doing. A high financial IQ turns most investments into informed decisions with quantifiable risk. A low financial IQ turns even simple investments into gambling.Rule 4: Savers are losers; spenders are winners

How the 7 rules of investing work together

Taken individually, each of these investing rules is valuable. Together, they form a coherent framework for building wealth through cash-flowing assets — a framework that is fundamentally different from the conventional financial planning model.

The journey begins with a mindset shift (Rule 1) and an understanding of income types (Rule 2). That understanding drives the behavior of converting earned income into passive income (Rule 3), which requires abandoning the saving-is-safe mythology (Rule 4). Executing that conversion well requires continuous investment in financial education, because the quality of the investor determines the quality of the outcomes (Rule 5). With knowledge comes the ability to find genuinely great deals (Rule 6) and evaluate them with sophistication (Rule 7).

This is not a linear checklist to be completed once. It is a compounding process. Each deal teaches more. Each passive income stream funds the next investment. Each year of applying these rules for investing builds the financial intelligence that makes the next deal easier to identify, structure, and execute.

Applying these rules

For someone beginning their investing journey, the gap between knowing these rules and applying them can feel daunting. Rich Dad’s consistent instruction is to start with education, not capital. Before putting money into any asset, understand how that asset produces income, what risks are specific to it, and what financial metrics determine whether a deal is good or bad.

Rich Dad’s approach to real estate investing, for example, begins with learning to read a deal — calculating projected cash flow, understanding cap rates and net operating income, evaluating neighborhood vacancy trends. The same applies to stocks and paper assets: understanding the difference between speculating on price appreciation and generating cash flow through dividends or options strategies determines whether a paper asset investment aligns with Rule 2 or contradicts it.

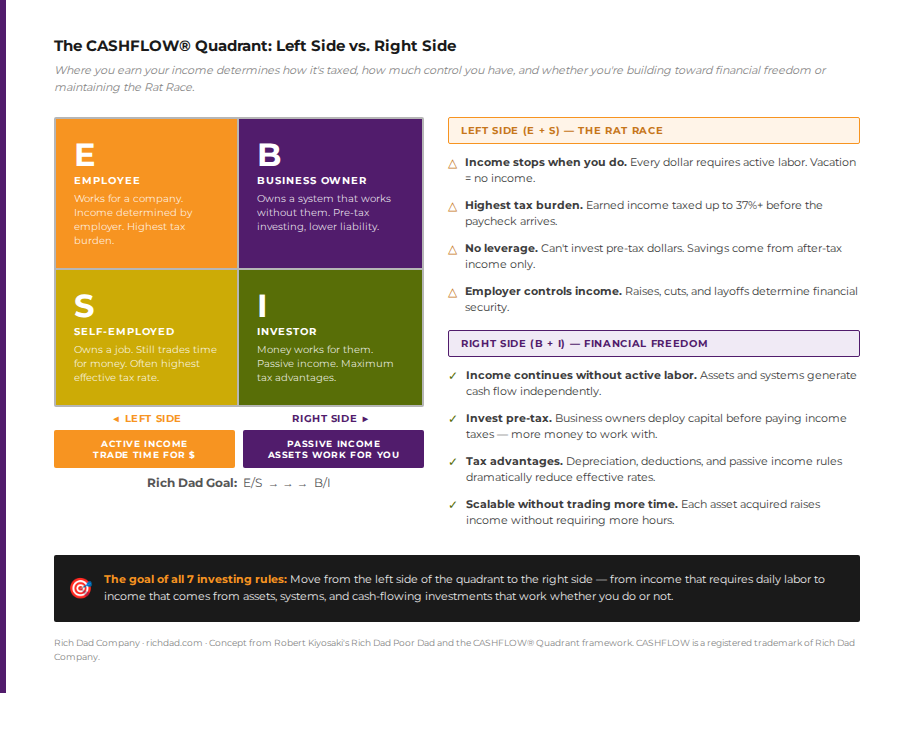

Beginning investors can also explore entrepreneurship as a path to the right side of the CASHFLOW Quadrant. Building a business that generates income independent of the owner’s daily involvement is, in Rich Dad’s framework, a cash-flowing asset — subject to the same rules for investing as any other income-producing property.

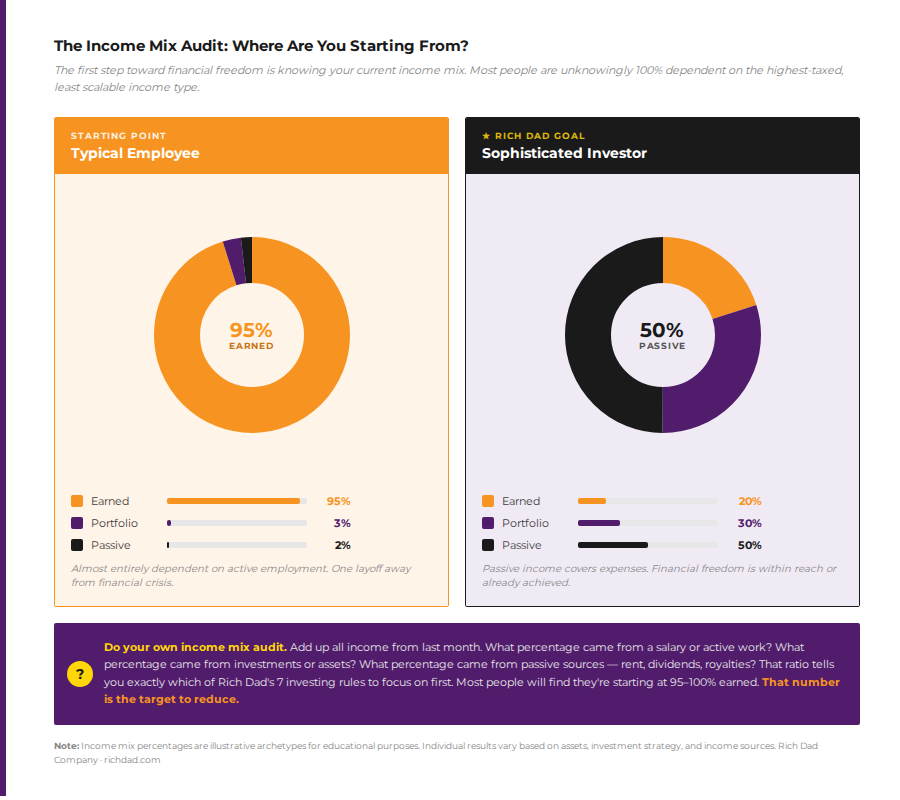

The most actionable first step for any beginner is to calculate their current income mix. What percentage of monthly income is earned (traded for time)? What percentage is portfolio income? What percentage is passive? That single audit reveals exactly which rules to focus on applying first.Rule 7: Learn to evaluate risk and reward

What separates investors who follow these rules from those who don’t

The conventional investing population operates on a fundamentally different set of rules — save 10-15% of income, diversify across asset classes, maintain a target-date fund, and hope the market cooperates until retirement. That approach has produced modest wealth for some and chronic financial anxiety for many more.

Investors who apply Rich Dad’s seven rules operate differently. They think about income type before they make any investment decision. They evaluate every potential acquisition for its cash-flow potential. They treat financial education as an ongoing expense rather than a one-time credential. They are not at the mercy of market timing because their income comes from assets that produce regardless of what the stock market does on any given Tuesday.

The behavioral difference is most visible in how these two groups respond to opportunities. A conventional investor who inherits money or receives a large bonus asks: “Should I put this in my 401(k) or a savings account?” An investor operating by Rich Dad’s rules asks: “What cash-flowing asset can I acquire with this capital that will generate income for the rest of my life?”

The answer to the second question is where wealth is built. And finding that answer, consistently and with increasing sophistication, is what applying these seven rules for investing ultimately produces.

The foundation of a lifetime of investing

These seven rules for investing are not complicated. But they are countercultural. They ask the investor to question assumptions that most people never examine — about savings, about income types, about risk, about where money really comes from and where it needs to go.

Mastering these rules takes time. It requires reading, practical experience, the inevitable mistakes that teach more than any book can, and the discipline to keep redirecting ordinary income into passive income assets even when the conventional world suggests a different path. But for investors willing to do that work, the rewards are not modest. They are the difference between a retirement that requires careful rationing and a life in which money simply isn’t a source of stress anymore.Start by exploring Rich Dad’s free financial tools and investing education resources. Play the CASHFLOW® game to practice applying these rules without real money at stake. And come back to these seven principles whenever an investment decision feels uncertain — because the answer to almost every investing question is somewhere within them.Applying these rules

FAQs

Robert Kiyosaki’s seven basic rules for investing are:

- Adjust your money mindset;

- Know what kind of income you’re working for;

- Convert ordinary income into passive income;

- Savers are losers — deploy money into assets;

- The investor is the asset or the liability;

- Good deals attract money; and

- Learn to evaluate risk and reward.

Together, these rules form a framework for building wealth through cash-flowing assets rather than accumulating a finite savings balance.

Rich Dad’s framework places mindset and financial education at the center of all investing rules. Without the right understanding of how money works — particularly the difference between earned income, portfolio income, and passive income — no other rule can be applied effectively. The investor is the determining variable in any investment outcome, which means investing in financial education consistently is the most important foundational rule.

Earned income comes from active labor — salaries and wages. It is the highest-taxed income type.

Portfolio income comes from paper assets like stocks and bonds — taxed at lower rates but still subject to market volatility and limited investor control.

Passive income comes from cash-flowing assets like rental real estate, business distributions, and royalties. It is the lowest-taxed income type and the only type that is scalable without trading additional hours of work. Rich Dad’s investing rules direct all strategies toward building passive income.

The “savers are losers” principle doesn’t mean saving is wrong — it means keeping money idle in a low-yield account is a guaranteed way to lose purchasing power over time. Inflation, taxes on interest income, and hidden fees in conventional retirement accounts all erode the real value of saved money. Rich Dad’s investing rules treat idle cash as a liability, not an asset. Money needs to be deployed into income-producing assets to grow. Savers preserve capital; investors multiply it.

For beginners, the most applicable investing rules are: start with financial education before committing capital; understand the three income types and consciously target passive income; treat every dollar of earned income as a potential seed for a cash-flowing asset; and start small, learn from experience, and scale deliberately. Rich Dad also recommends using simulations — like the CASHFLOW® board game — to practice deal evaluation and cash flow thinking before real money is at stake.

OPM stands for Other People’s Money — the principle that a financially educated investor with a genuinely great deal can attract funding from others rather than relying solely on personal capital. Rich Dad’s Rule 6 (good deals attract money) is built on this concept. It means that the scarcest resource in investing is not capital — it is the knowledge and preparation to find and evaluate excellent opportunities. Investors who develop that capability rarely find that money is the limiting factor in executing a deal.

The CASHFLOW Quadrant describes four income positions: Employee, Self-Employed, Business Owner, and Investor. The left side (E and S) represents active income — trading time for money. The right side (B and I) represents passive income — assets and systems that generate cash flow without the owner’s daily involvement. All seven of Rich Dad’s rules for investing are designed to help people move from the left side of the quadrant to the right — from income dependence to income independence.