What is the difference between being rich and being wealthy?

The confusion between rich and wealthy is understandable — both words conjure images of large bank accounts and expensive homes. But they describe two very different financial realities. As Robert Kiyosaki learned from his rich dad: “The rich have lots of money but the wealthy don’t worry about money.”

Being rich is primarily about income and appearances. A surgeon earning $400,000 a year, driving a leased luxury car, carrying a large mortgage, and living paycheck to paycheck is, by most measures, rich. But if that income stopped tomorrow, so would everything else. The lifestyle is propped up entirely by active labor.

Being wealthy is about the relationship between assets and expenses. A person generating $6,000 a month from rental properties and dividend income, with $4,500 in monthly expenses, is wealthy — regardless of whether their income looks impressive on paper. Their assets work for them. They do not have to work for their assets. That is the core distinction.

Rich: High income, high dependence

High earners who consume most of what they earn are financially fragile. This is what Robert calls the Rat Race: a cycle of earning and spending that keeps even six-figure households locked into mandatory employment. A single layoff, health crisis, or economic downturn can unravel years of apparent financial progress. Income without assets is not wealth — it is a recurring salary that disappears the moment it stops.

The data reinforces how common this trap is. According to the Federal Reserve’s 2024 Report on the Economic Well-Being of U.S. Households, roughly 30% of American adults could not cover three months of expenses by any means whatsoever — not savings, not credit, not assets. High income does not protect against this. Spending at the rate of income does.

Wealthy: Passive income, true independence

Wealthy people own assets that generate income whether or not they show up to work. These might include rental real estate that produces monthly cash flow, dividend-paying stocks and paper assets, royalties, or businesses that operate without the owner’s daily involvement. The common thread is that income is decoupled from time.True wealth is the ability to sustain a chosen lifestyle indefinitely without exchanging hours for dollars. When passive income meets or exceeds monthly expenses, employment becomes optional — and that threshold, Kiyosaki argues, is the only definition of financial freedom worth pursuing.The definition of being wealthy

There are countless ways to define the word “wealth.” A brilliant inventor, philosopher, and humanitarian named R. Buckminster Fuller defined it as such: “Wealth is a person’s ability to survive X number of days forward.”

How to know which side you’re on: The Wealth Number

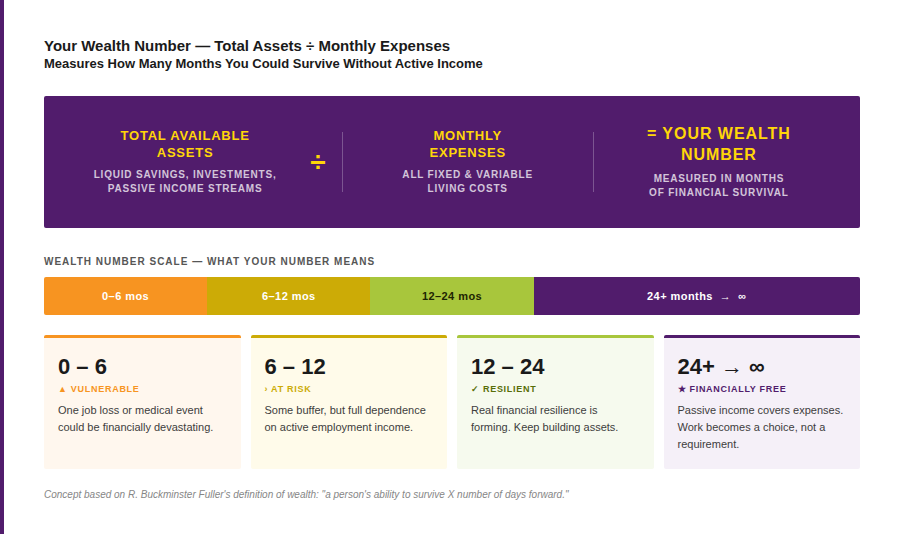

The abstract distinction between rich and wealthy becomes concrete with one calculation. R. Buckminster Fuller — inventor, philosopher, and one of the twentieth century’s most original thinkers — defined wealth not in currency but in time: “a person’s ability to survive X number of days forward.” Robert built on this to create the Wealth Number: a simple formula that answers, without ambiguity, which side of the rich vs. wealthy line a person is actually standing on.

Rich dad put it simply: “Rich is measured in money, and wealth is measured in time. Most people focus on getting rich rather than becoming wealthy.”

The Wealth Number answers one essential question: If you — or you and your partner — stopped working today, how long could you survive financially at your current standard of living?

Not at a reduced standard. Not after selling possessions or downsizing. At the lifestyle that exists right now. The result is expressed in months, and it is perhaps the most honest financial assessment most people have ever confronted.

What counts — and what doesn’t

When calculating a Wealth Number, assets that count are those convertible to cash today or that generate income without requiring active labor:

- Cash savings and money market accounts

- CDs and liquid investment accounts

- Retirement accounts (401k, IRA — noting that early withdrawal penalties apply)

- Liquid stocks that could be sold today

- Physical gold and silver held in possession

- Passive income from rental properties, dividends, or other income-generating investments

What does NOT count toward the Wealth Number:

- Equity in a primary residence (selling it would lower the standard of living)

- Jewelry, furniture, or everyday vehicles

- Business equity that cannot be quickly liquidated

The goal is not to inventory everything of value — it’s to isolate the resources available to sustain life without active work. That distinction is what matters.

How to calculate your Wealth Number

The formula is straightforward:

To calculate it accurately, follow three steps:

- Determine total monthly expenses

Don’t estimate. Pull three months of bank and credit card statements and calculate the average. Include every recurring obligation: housing, food, transportation, utilities, subscriptions, insurance, and debt service. The objective is to confront the real number, not a sanitized version of it. - Total all available liquid assets

Add cash, savings accounts, liquid investments, physical precious metals, and passive income streams. For passive income, calculate the monthly amount it generates and include it as an ongoing offset against expenses. - Divide

Divide total available assets by total monthly expenses. The result is the Wealth Number in months.

Example: If monthly expenses are $5,000 and total available liquid assets are $25,000, the Wealth Number is 5 — meaning five months of financial survival without any employment income.The formula is straightforward:

Your Wealth Number defined

Once calculated, the Wealth Number is a direct signal of financial health:

- Under 6 months

Financially vulnerable. A single job loss, medical event, or economic disruption could be catastrophic. - 6 to 12 months

Some buffer exists, but the household is still entirely dependent on employment income. - 12 to 24 months

Progress. Real financial resilience is beginning to form. - Effectively unlimited

Financial freedom. Passive income covers monthly expenses indefinitely, with no need to draw down principal.

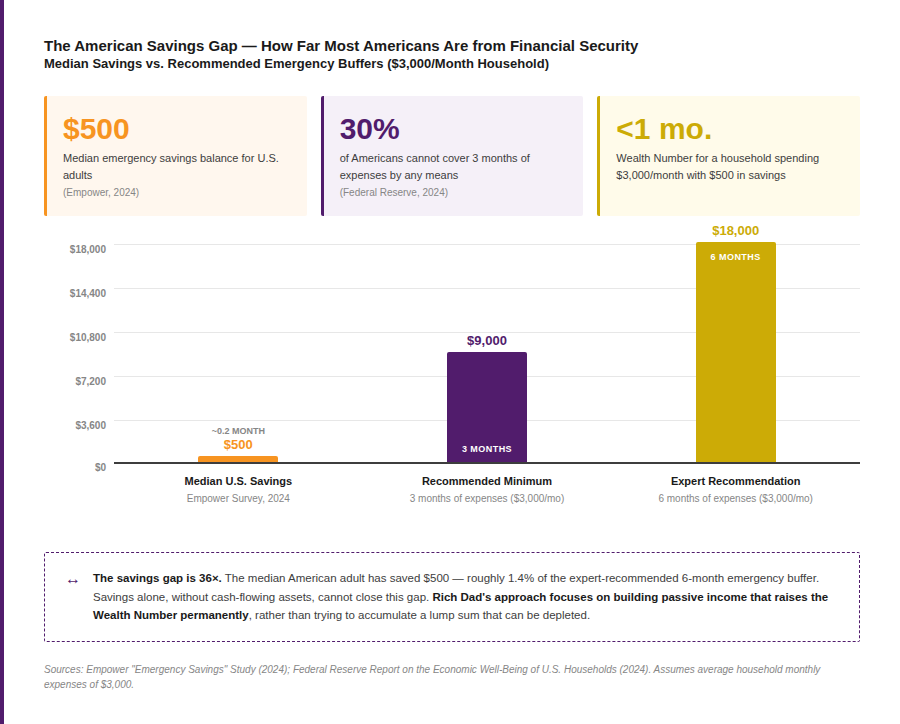

The sobering reality: a 2024 survey by Empower Financial Services found the median emergency savings balance among American adults is just $500. For a household spending $3,000 per month, that’s a Wealth Number of 0.17 — less than one week. That is not a measurement of wealth. It is a measurement of financial precarity.

The most unsettling realization for many who do this exercise is that after decades of working, their Wealth Number is still measured in weeks, not years.

Rich vs. wealthy in retirement

The rich vs. wealthy distinction plays out most dramatically at retirement age. Conventional financial planning effectively assumes that most retirees will be rich — not wealthy. It operates on two assumptions Robert has long challenged:

- At retirement, a person will have a fixed lump sum that earns modest interest until it is depleted.

- Retirement requires accepting a lower standard of living than was enjoyed while working.

The Rich Dad philosophy rejects both. Instead of building toward a finite pool of money that must be rationed until death — a stressful calculation with no guaranteed outcome — Rich Dad teaches the acquisition of assets that produce ongoing cash flow. The goal isn’t a retirement account balance; it’s a monthly passive income that covers expenses indefinitely.

Consider two retirees:

| Retiree A (Traditional) | Retiree B (Rich Dad Approach) |

|---|---|

| $800,000 in a 401(k) | $200,000 in savings + 3 rental properties |

| 4% rule = $2,667/month income | $3,500/month net passive income |

| $4,000 monthly expenses — runs out in ~20 years | $3,000 monthly expenses — income never depletes |

| Wealth Number: ~200 months (finite) | Wealth Number: Unlimited (∞) |

This is the difference between a finite Wealth Number and an infinite one. One runs out. The other doesn’t. Rich Dad’s approach to real estate investing, stocks and paper assets, and entrepreneurship is built entirely around converting finite Wealth Numbers into infinite ones.

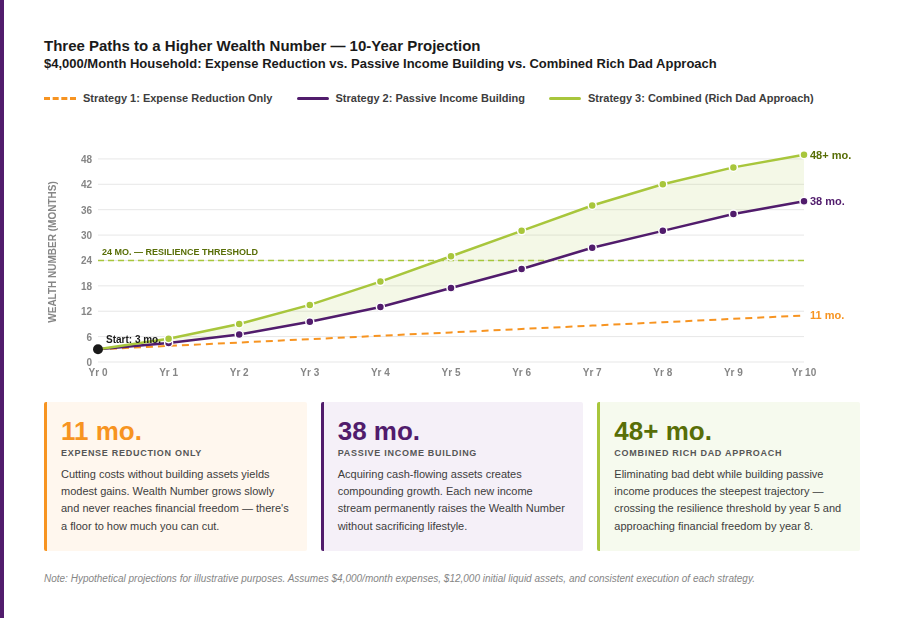

Moving from rich to wealthy

Moving from rich to wealthy — from income-dependent to asset-supported — requires changing what gets built, not just how much gets earned. There are only two levers available: reduce monthly expenses or increase passive income. Most financial advice focuses heavily on the first. Rich Dad focuses on the second — and for good reason. Cutting expenses is finite. There is a floor below which spending cannot go. But passive income has no ceiling. Every cash-flowing asset added to a portfolio permanently raises the Wealth Number without requiring any reduction in lifestyle.

Step 1: Know your number first

Most people have never calculated their Wealth Number. The calculation takes less than an hour, and the clarity it delivers is worth more than any financial plan built on vague estimates. The process is the same as described above — but the most important thing is to actually do it, and to be honest with the numbers.

Step 2: Build cash-flowing assets

The assets that most meaningfully increase a Wealth Number are those that generate income without requiring daily labor: rental real estate, dividend-paying investments, royalties, and businesses that operate without the owner’s constant involvement. Each new income stream raises the monthly passive income figure and, in turn, the Wealth Number.

Step 3: Eliminate bad debt

Bad debt — consumer credit, high-interest liabilities that generate no income — increases monthly expenses and suppresses the Wealth Number. Understanding the difference between good debt and bad debt is one of the foundational principles of the Rich Dad philosophy. Paying down bad debt is one of the fastest ways to improve the metric.

Step 4: Build Financial Intelligence

Rich Dad’s core argument has always been that financial education is the most undervalued asset in most people’s lives. Understanding how money works, how the tax code treats investors versus employees, and how to evaluate income-producing assets changes the quality of every financial decision going forward. A higher financial IQ translates directly into a higher Wealth Number.

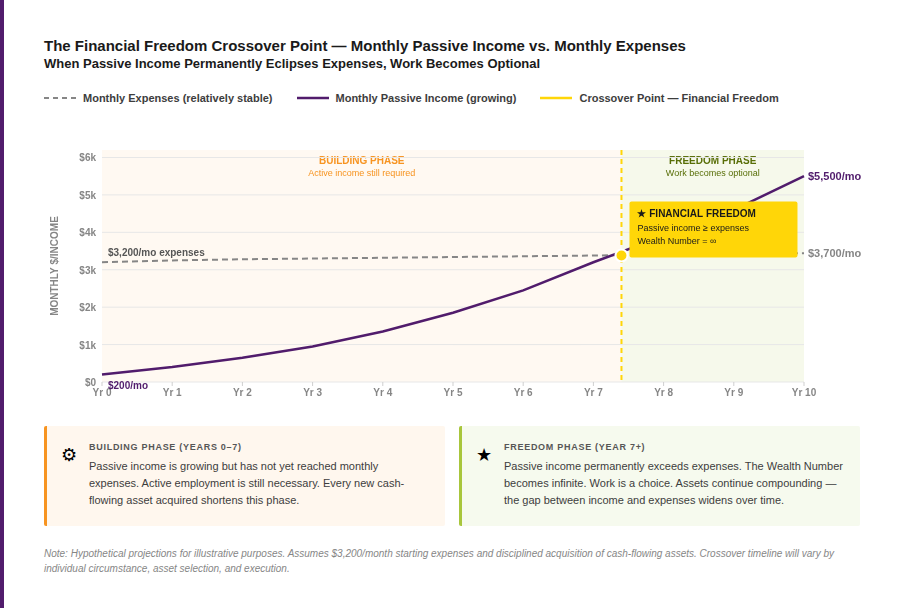

The crossover point: When wealthy finally overtakes rich

There is a specific milestone that marks the transition from rich to truly wealthy: the moment monthly passive income permanently equals or exceeds monthly expenses. At that point, the Wealth Number becomes effectively infinite — no assets need to be drawn down, expenses are covered regardless of employment status, and work is a choice rather than a requirement.

Robert defines this as true financial freedom: not a dollar figure in an account, but a cash-flow state. It is the destination the entire Rich Dad framework is designed to reach. And it is achieved not by saving more of a paycheck, but by acquiring assets that generate income whether or not anyone shows up to work.

Why so many high earners are rich, but not wealthy

Most high earners are rich by conventional standards. They have impressive salaries, nice homes, and expensive lifestyles. But many are one missed paycheck away from afinancial crisis — because everything they have is funded by active labor, not by assets. That is the definition of the Rat Race: a cycle of earning and spending that makes the distinction between rich and wealthy feel invisible until it suddenly becomes urgent.

The CASHFLOW® board game — central to Robert Kiyosaki’s Rich Dad Poor Dad curriculum and playable at richdad.com/cashflow — was designed specifically to make this distinction tangible. Players learn to identify assets that generate income and liabilities that drain it, and experience firsthand what it feels like to move a Wealth Number from zero toward financial freedom.

The lesson isn’t that high income is bad. It’s that high income without asset acquisition keeps even the highest earners on the wrong side of the rich vs. wealthy divide.Why so many high earners are rich, but not wealthy

Asking the right retirement question: Rich or wealthy?

The conventional retirement question is: “How much money do I need to save?” That is a rich person’s question — it assumes a lump sum to be protected and carefully spent down. Rich Dad reframes it: “How much monthly passive income do I need to cover my expenses permanently?” That is a wealthy person’s question — it assumes an asset base that produces income indefinitely.

The difference is not academic. A retiree with $800,000 in a 401(k) is rich on paper, but if monthly expenses exceed what that balance can safely generate, the money runs out. A retiree with $200,000 in savings and three rental properties generating $3,500 a month in net cash flow may be worth less on paper — but will never run out of income. One is rich. The other is wealthy. Understanding which path is being built toward, and doing so while there is still time to course-correct, is what Rich Dad’s approach to saving and investing is designed to achieve.

Conclusion

The difference between rich and wealthy is not a matter of how much someone earns — it’s a matter of what their money does when they stop earning it. Rich people have income. Wealthy people have assets that produce income. And the gap between those two positions is measured by the Wealth Number: total available assets divided by monthly expenses, expressed in months.

For most Americans, that number is smaller than expected. But the calculation itself is the starting point. Knowing where the line is — and how far from it a current financial situation sits — makes the path forward visible. The Rich Dad approach to building passive income, eliminating bad debt, and developing genuine financial intelligence is a proven path from rich to truly wealthy.

The goal isn’t to impress others with income. It’s to build assets that generate enough cash flow that work becomes a choice. That is what it means to move from rich to wealthy — and it begins with knowing your number. Explore Rich Dad’s free financial tools and personal finance education resources to begin building the financial intelligence that makes a growing Wealth Number possible.

FAQs

Being rich typically means having a high income or significant money — but also significant expenses that make active income a necessity. Being wealthy means having passive income or assets sufficient to cover all living expenses indefinitely, without relying on a job. Rich describes how much someone earns. Wealthy describes how long they could survive without earning. According to Robert Kiyosaki, the key distinction is that the wealthy don’t worry about money — because their assets work for them whether they work or not.

Yes — and it is more common than most people realize. A high-income professional who spends at or near their income level, carries a large mortgage, and has little in the way of income-producing assets is rich but not wealthy. If their income stopped tomorrow, their lifestyle would collapse within months. Wealth requires assets that generate income independent of active labor. High income alone does not create wealth; it simply creates the opportunity to build it.

The Wealth Number is Robert Kiyosaki’s practical test of whether someone is truly wealthy. It is calculated by dividing total available liquid assets — cash, savings, liquid investments, physical gold and silver, and passive income streams — by total monthly expenses. The result is a number of months. A Wealth Number of 6 means six months of financial survival without income. An unlimited Wealth Number means passive income fully covers all expenses indefinitely.

Rich Dad defines wealth in terms of time rather than money, drawing on R. Buckminster Fuller’s concept that “wealth is a person’s ability to survive X number of days forward.” In practical terms, a person is wealthy when their assets generate enough passive income to cover their living expenses without requiring active work. Wealth is not a dollar amount — it is a cash-flow condition.

There is no universal benchmark, but a Wealth Number below 6 months indicates financial vulnerability. Between 12 and 24 reflects meaningful resilience. The Rich Dad philosophy ultimately aims for an unlimited Wealth Number — the point at which monthly passive income equals or exceeds monthly expenses permanently. That is the definition of financial freedom, and it marks the true transition from rich to wealthy.

The path from rich to wealthy involves acquiring income-producing assets: rental real estate, dividend-paying investments, businesses that generate income without constant personal involvement, and other cash-flowing holdings. Eliminating bad debt reduces monthly expenses and accelerates the process. Building financial education — understanding how money, taxes, and assets work — is the foundation that makes every other step more effective. Rich Dad’s core curriculum is built around exactly this transition.

Passive income is the defining factor. The wealthy are wealthy precisely because their passive income covers their expenses. Every new income-producing asset acquired raises the Wealth Number permanently — and once passive income exceeds monthly expenses, the Wealth Number becomes infinite. That crossover point is the moment rich becomes wealthy, and it is achievable through deliberate asset acquisition rather than simply earning more.