Flipping the script

Personal finance advice is everywhere — and most of it leads to the same place. Millions of Americans follow the conventional script: live below their means, max out a 401(k), and hope the market cooperates by the time they turn 65. Rich Dad’s approach is fundamentally different. It begins not with restriction, but with financial education.

Robert Kiyosaki first published Rich Dad Poor Dad in 1997. With more than 32 million copies sold, it remains the best-selling personal finance book of all time — not because it told people what they expected to hear, but because it told them the truth about how money actually works. This guide covers that same territory, updated for today’s economy.

The Rich Dad way to budget

Most financial experts define budgeting as the art of balancing income against expenses. Rich Dad defines it differently: budgeting is a tool for generating more income and expanding your means — not just for managing what you already have. The budget is not a cage. It is a map.

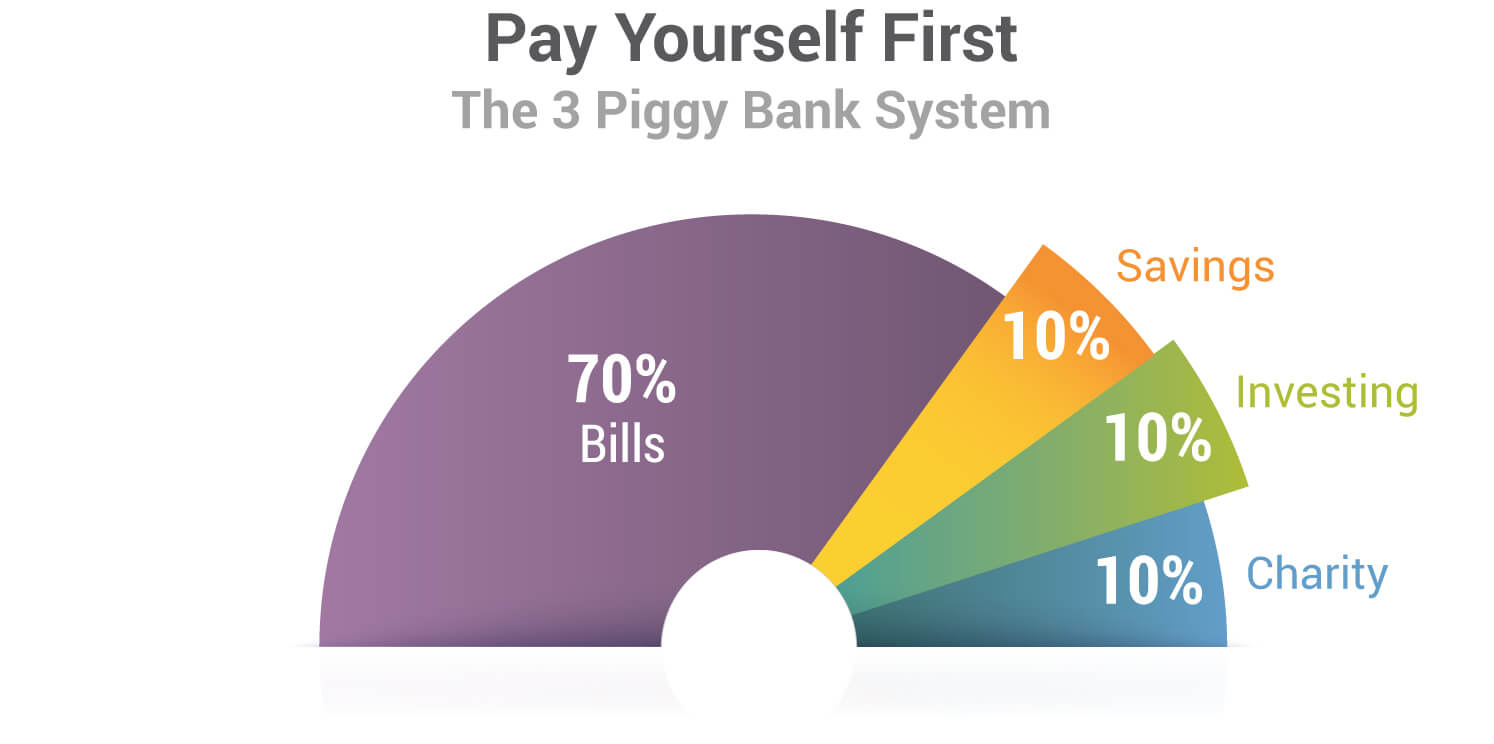

Pay yourself first

The foundation of Rich Dad’s budgeting philosophy is a principle called Pay Yourself First. Before bills are paid, before groceries are bought, before any expense is addressed — a portion of every dollar that comes in is allocated toward building financial security.

The Rich Dad model divides that 30% allocation across three accounts:

- Savings Account (10%) — A cushion for unforeseen emergencies, not a wealth-building vehicle. This account exists to prevent a crisis from becoming a catastrophe.

- Investing Account (10%) — Capital reserved for investment opportunities. Keeping this funded and separate means that when a deal appears, the money is ready.

- Charity or Tithing Account (10%) — Consistent giving reinforces an abundance mindset. As Rich Dad often observed, those who give freely tend to receive more in return.

The amount is secondary to the discipline. A person earning $3,000 per month who invests $300 consistently will build more lasting wealth than a person earning $10,000 who saves nothing.

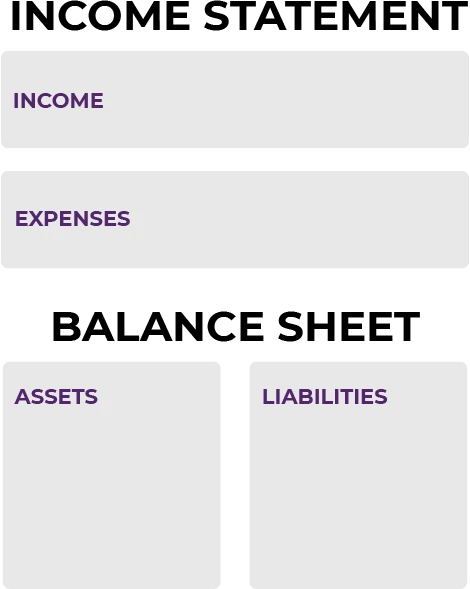

Budgeting with the personal financial statement

Most people track their finances with a basic income-and-expense spreadsheet. Rich Dad teaches the use of a personal financial statement — the same document that banks and sophisticated investors use to evaluate financial health.

A personal financial statement has two parts:

- The income statement tracks money flowing in and out. It records the three types of income — earned, portfolio, and passive — alongside all monthly expenses. The critical insight is directional: money coming in should flow toward assets, not directly toward expenses.

- The balance sheet records what is owned and what is owed. Assets appear on one side, liabilities on the other. Most people cannot reliably distinguish between the two — which is precisely why most people remain financially stuck.

The critical difference between assets and liabilities

Rich Dad’s most important lesson can be reduced to one sentence: an asset puts money into your pocket, and a liability takes money out of it.

This sounds obvious — until you consider that most Americans have been told their home is their greatest asset. According to Rich Dad, a personal residence is a liability, not an asset. It generates no income and creates ongoing expenses in the form of mortgage payments, property taxes, insurance, and maintenance.

True assets include rental properties that generate monthly cash flow, dividend-paying stocks and paper assets, businesses that produce income without requiring the owner’s daily presence, and royalties from intellectual property. Liabilities include consumer debt, personal vehicles, a primary residence, and any purchase that depreciates without producing a return.

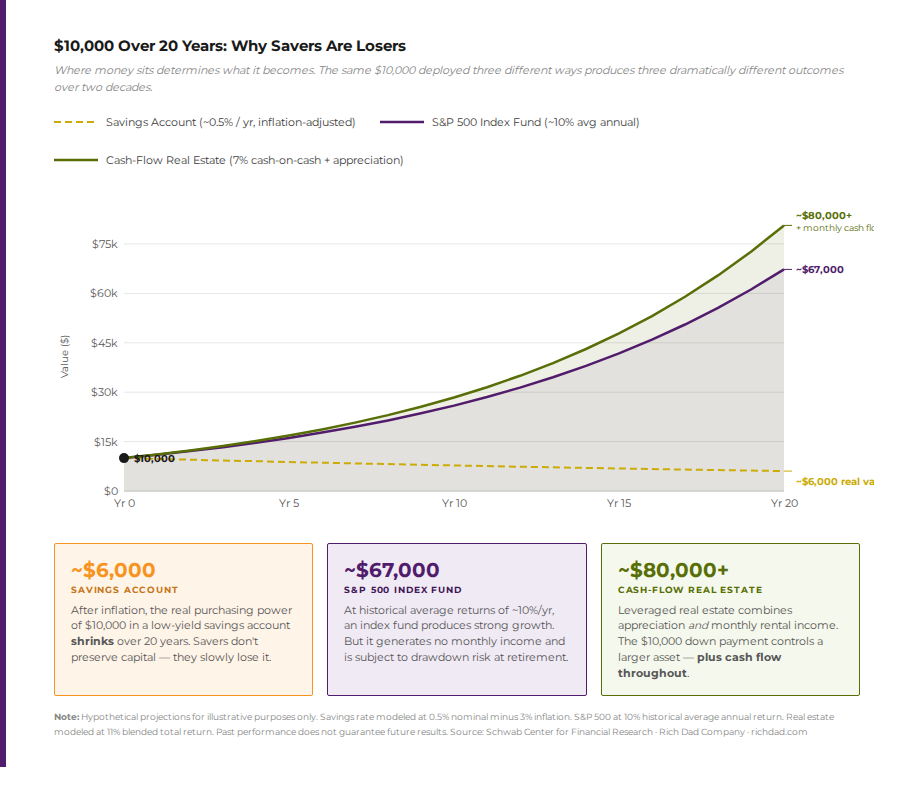

Savers are losers

This position on saving is one of its most counterintuitive — and most important. Saving money in a low-yield account is not building wealth. It is losing purchasing power in slow motion.

The mechanism is inflation. When inflation runs at 3–4% annually and the average savings account yields 0.58% — the current national rate according to Bankrate’s 2025 savings data — money sitting in the bank loses real value every single year. The Federal Reserve targets 2% inflation. No savings account keeps pace with that, let alone the higher inflation rates experienced by most households in recent years.

Savers are not rewarded — they are slowly depleted. The Rich Dad alternative is to deploy capital into cash-flowing assets: investments that generate income every month regardless of whether the owner is working.

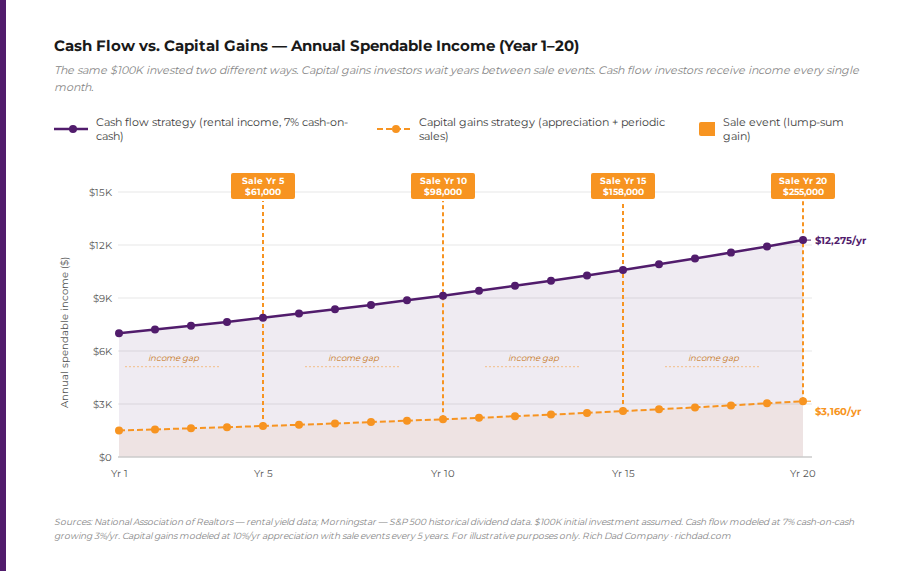

Cash flow vs. capital gains

There are two ways to profit from an investment: cash flow and capital gains.

Capital gains come from selling an asset at a higher price than what was paid. This is the default model most people follow with stocks and real estate — buy low, hope the price rises, sell. The problem is that capital gains require a sale event to generate income. Between sale events, the investor earns nothing.

Cash flow is income that arrives every month: rent from a rental property, dividends from stocks, royalties from a book or patent, distributions from a business. The asset is never sold — it simply produces income continuously.

Rich Dad prioritizes cash flow because it creates income independence. An investor who builds enough monthly passive income to cover living expenses no longer depends on a paycheck — and has reached what Rich Dad calls the financial freedom crossover point.

How the rich use debt to their advantage

Most conventional financial advice instructs people to eliminate all debt as quickly as possible. Rich Dad makes a distinction that most advisors overlook: not all debt is created equal.

There are two types — good debt and bad debt.

Bad debt finances liabilities: consumer goods, vacations, personal vehicles, a primary residence. It extracts money from your pocket without returning anything. Bad debt should be minimized and paid off as quickly as possible.

Good debt finances income-producing assets. When borrowed money is used to acquire a rental property that generates positive monthly cash flow after all expenses — including the mortgage payment — that debt is working for the borrower. The asset is producing more than the debt costs. This is leverage.

The wealthy understand that using Other People’s Money (OPM) — borrowed capital — to acquire assets allows an investor to control significantly more than they could with their own funds alone. The cash flow those assets produce services the debt and still generates a positive return. This is one reason real estate has historically been one of the most powerful wealth-building vehicles available.

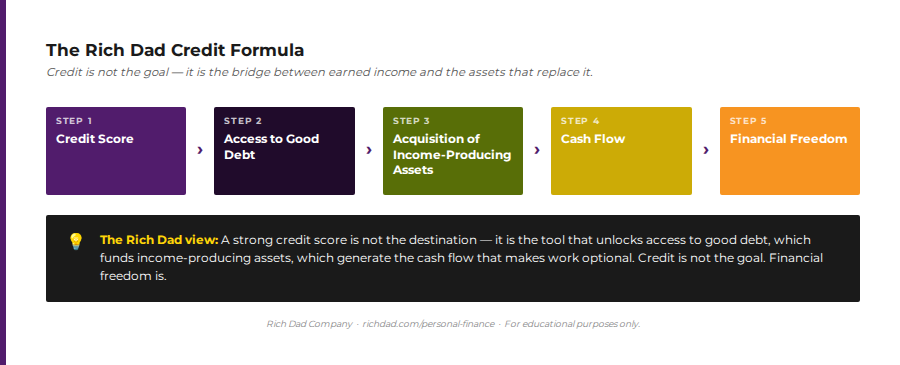

Your credit score and why it matters

The key to accessing good debt is creditworthiness. A strong credit score is not just a number — it is a gateway to better interest rates, more favorable loan terms, and the financial access that makes investment possible.

Credit scores are measured on a scale from 300 to 850. According to Experian’s consumer credit guide, a score above 670 is considered “good,” and anything above 800 is “exceptional.” Lenders use this score to assess risk — the lower the perceived risk, the better the terms offered to the borrower.

The factors that determine a credit score include:

- Payment history — The single most important factor.

- Credit utilization — How much available credit is currently being used.

- Length of credit history — Older accounts signal stability.

- Types of credit accounts — A mix of revolving and installment credit.

- Recent credit inquiries — Multiple hard inquiries in a short window signal financial stress.

The fastest path to a better credit score is paying creditors on time and reducing balances on revolving accounts. Rich Dad’s framing: a strong credit score is not the end goal — it is a tool that unlocks access to good debt, which funds income-producing assets.

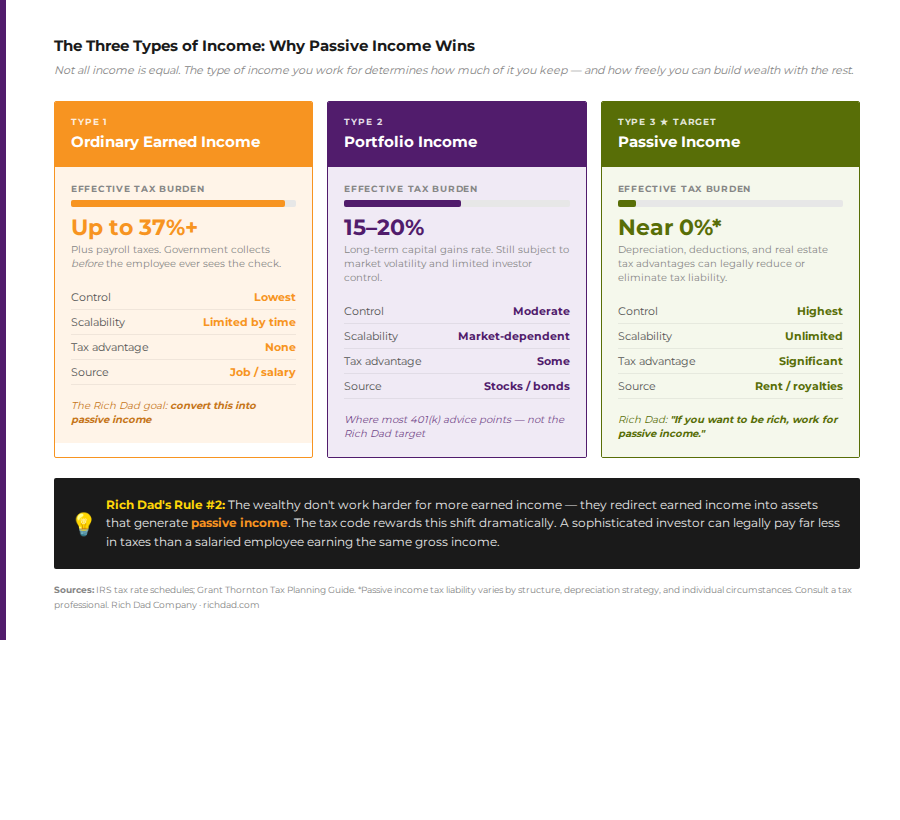

The three types of income and how they’re taxed

The tax code is one of the most powerful levers available to investors — and most people never use it. Rich Dad teaches that financial freedom is built not just by earning more, but by keeping more of what is earned. That requires understanding how different income types are taxed at dramatically different rates.

This is not a loophole. The tax code rewards investors who deploy capital into productive economic activity — real estate, business ownership, and other cash-flowing assets. Rich Dad’s strategy is to redirect earned income into assets that generate passive income, gradually shifting the effective tax burden from the highest category to the lowest. For rates specific to your situation, consult a qualified tax professional.

How to retire young and rich

Conventional retirement planning says to accumulate a large enough lump sum that the interest and withdrawals can sustain living expenses for the rest of a person’s life. Rich Dad argues this model is fundamentally flawed — because it depends entirely on the lump sum not running out.

The Rich Dad alternative is to build enough passive income to permanently cover monthly expenses. When that happens, the lump sum becomes irrelevant — because the income continues indefinitely.

The rich don’t work for money; money works for them

The central idea behind Rich Dad’s retirement philosophy is that financial freedom is achieved not when a person has saved enough to stop working, but when their assets generate enough income to make work optional.

This is the difference between accumulation and cash flow. A person who has saved $1 million but earns no passive income is still dependent on that finite pool of capital not depleting. A person who earns $5,000 per month from rental properties, dividends, and royalties can retire indefinitely — because the income streams continue regardless of whether they work.

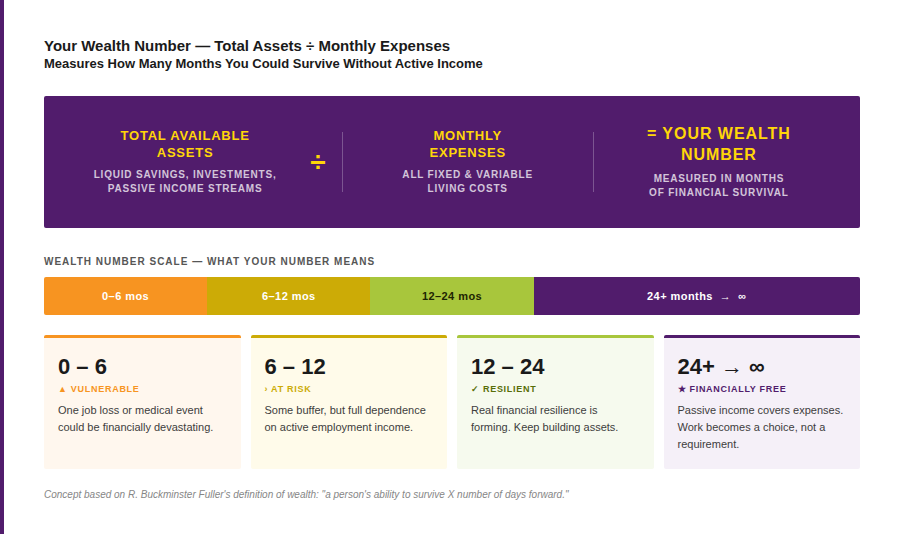

Your Wealth Number

Rich Dad teaches a metric called the Wealth Number that quantifies this reality:

The three piggy banks for retirement

Robert Kiyosaki’s rich dad used the metaphor of three piggy banks to explain the mechanics of building toward retirement, and they look familiar– as they are a continuation of the “Pay Yourself First” method mentioned above.

- Savings Account (10%) — A cushion for unforeseen emergencies, not a wealth-building vehicle. This account exists to prevent a crisis from becoming a catastrophe.

- Investing Account (10%) — Capital reserved for investment opportunities. Keeping this funded and separate means that when a deal appears, the money is ready.

- Charity or Tithing Account (10%) — Consistent giving reinforces an abundance mindset. As Rich Dad often observed, those who give freely tend to receive more in return.

The conventional retirement system — 401(k) plans, mutual funds, market-dependent savings — puts retirement outside the investor’s control. Rich Dad’s model returns control to the individual by focusing on real assets with real cash flow that the owner can evaluate, manage, and build.

Rich Dad’s core personal finance principles

The lessons in this guide are not theoretical. They are the same principles Robert Kiyosaki learned from his rich dad — his best friend’s father — and documented in Rich Dad Poor Dad. They apply equally whether someone is starting from zero, rebuilding from setbacks, or simply dissatisfied with the conventional financial script.

School trains employees, not entrepreneurs. True success requires financial education, not just traditional education.

Go to school

Go to school, get good grades, you’ll be successful.

Job security is a myth — real freedom comes from creating income through businesses and investments.

Get a good job

Get a good, secure job with good benefits to be financially stable.

The rich work smart — they make money work for them.

Work hard

Hard work leads to success and wealth.

The rich expand their means by building cash-flowing assets. Asking, “How can I afford that?” sparks creativity.

Live below your means

Cut expenses, budget strictly, and be frugal to get ahead.

Saving erodes wealth due to inflation. Investing in cash-flowing assets grows wealth. Savers are losers in today’s economy.

Save money

Saving money in the bank builds security and wealth.

If it takes money out of your pocket, it’s a liability — even your home.

Your house is an asset

Your personal home is your biggest asset and investment.

The wealthy use good debt to buy assets that pay them every month.

Get out of debt

All debt is bad. Pay off all your debts to be financially free.

True diversification means investing across different asset classes: real estate, business, commodities, and paper assets. Paper-only diversification keeps you exposed to systemic risk.

Diversify

Diversify into stocks, bonds, mutual funds and hold long term.

| PHILOSOPHIES | TRADITIONAL | RICH DAD |

|---|---|---|

| 1: Go to school | School trains employees, not entrepreneurs. True success requires financial education, not just traditional education. | Go to school, get good grades, you’ll be successful. |

| 2: Get a good job | Job security is a myth — real freedom comes from creating income through businesses and investments. | Get a good, secure job with good benefits to be financially stable. |

| 3: Work hard | The rich work smart — they make money work for them. | Hard work leads to success and wealth. |

| 4: Live below your means | The rich expand their means by building cash-flowing assets. Asking, “How can I afford that?” sparks creativity. | Cut expenses, budget strictly, and be frugal to get ahead. |

| 5: Save money | Saving erodes wealth due to inflation. Investing in cash-flowing assets grows wealth. Savers are losers in today’s economy. | Saving money in the bank builds security and wealth. |

| 6: Your house is not an asset | If it takes money out of your pocket, it’s a liability — even your home. | Your personal home is your biggest asset and investment. |

| 7: Get out of debt | The wealthy use good debt to buy assets that pay them every month. | All debt is bad. Pay off all your debts to be financially free. |

| 8: Diversify | True diversification means investing across different asset classes: real estate, business, commodities, and paper assets. Paper-only diversification keeps you exposed to systemic risk. | Diversify into stocks, bonds, mutual funds and hold long term. |

Optimize for financial freedom

Personal finance advice is everywhere. Most of it optimizes for financial security — which sounds reasonable, until you realize that “security” in the conventional sense means working until 65, hoping the market cooperates, and hoping the savings last. Rich Dad’s approach optimizes for financial freedom: the state where assets generate enough income to make work a choice.

The path starts with financial education. Understanding how money flows through a personal financial statement, why savers lose to inflation over time, how good debt accelerates asset acquisition, how different income types are taxed at dramatically different rates, and how the Wealth Number defines true retirement — these are not advanced concepts. They are the fundamentals most people were never taught.

For those ready to go deeper: Rich Dad Poor Dad remains the essential starting point. From there, the Rich Dad investing hub, budgeting resources, debt education, and tax strategy pages provide the next layers of knowledge. The CASHFLOW board game — available at the Rich Dad store — is the fastest way to practice these concepts in real time.

FAQs

Rich Dad’s approach centers on building cash-flowing assets rather than accumulating savings. The core principles include paying yourself first, understanding the difference between assets and liabilities, using good debt to acquire income-producing investments, and structuring income to minimize taxes. The goal is financial freedom — a state where passive income exceeds monthly expenses and work becomes optional.

Rich Dad defines an asset as anything that puts money into your pocket — rental properties, dividend-paying stocks, businesses with systems, royalties. A liability is anything that takes money out of your pocket — consumer debt, personal vehicles, and even a primary residence. Most people confuse the two, which is why most people remain financially stuck. Clarifying this distinction is the first step toward building real wealth.

When savings account interest rates fall below the rate of inflation — which they almost always do — money sitting in the bank loses purchasing power every year. Rich Dad’s position is not that saving is wrong, but that savings accounts are not a wealth-building strategy. The goal is to deploy capital into cash-flowing assets that generate returns exceeding inflation, not to accumulate dollars that slowly lose value.

Bad debt is borrowed money used to purchase liabilities — things that depreciate or generate no income, like consumer goods or personal vehicles. Good debt is borrowed money used to purchase income-producing assets, particularly investments where the monthly return exceeds the cost of the debt. When used correctly, good debt acts as leverage that allows an investor to control more assets than their own capital would permit.

Passive income — from rental properties, limited partnerships, and similar sources — is typically taxed at significantly lower effective rates than ordinary earned income. Depreciation deductions, cost segregation strategies, and passive loss rules can legally reduce or eliminate federal tax liability on passive income. Ordinary earned income, by contrast, is subject to both income tax and FICA payroll taxes, creating effective federal rates of 30–37% for middle and upper-income earners.

The Wealth Number is a Rich Dad metric that measures financial resilience: total available assets divided by monthly expenses equals the number of months a person could survive without active income. A Wealth Number of 24 or more indicates genuine financial resilience. When passive income permanently exceeds monthly expenses, the Wealth Number becomes theoretically infinite — which is Rich Dad’s definition of financial freedom.

Rich Dad views 401(k) plans critically. They put retirement savings in the hands of market performance, charge ongoing management fees, and defer taxes to retirement — when rates may be higher. More fundamentally, a 401(k) is a finite pool of capital that can be depleted. Rich Dad advocates instead for building passive income from real assets, so that retirement is funded by a continuous income stream that does not run out.