The myth of the million-dollar savings goal

For generations, “becoming a millionaire” has been the shorthand for financial success. Save a million dollars and, the thinking goes, you’ll be set for life. But the mathematics of that goal — and what that million actually buys — tells a very different story.

According to the Bureau of Labor Statistics, reaching $1 million in savings through traditional employment and disciplined saving requires roughly 40 or more years of extreme sacrifice — saving 13% of a median income at a 7% annual return, starting at age 20. That calculation leaves almost no room for health emergencies, market downturns, or the reality that most Americans save far less. In fact, a Bankrate survey found that 80% of Americans dip into their savings for essentials.

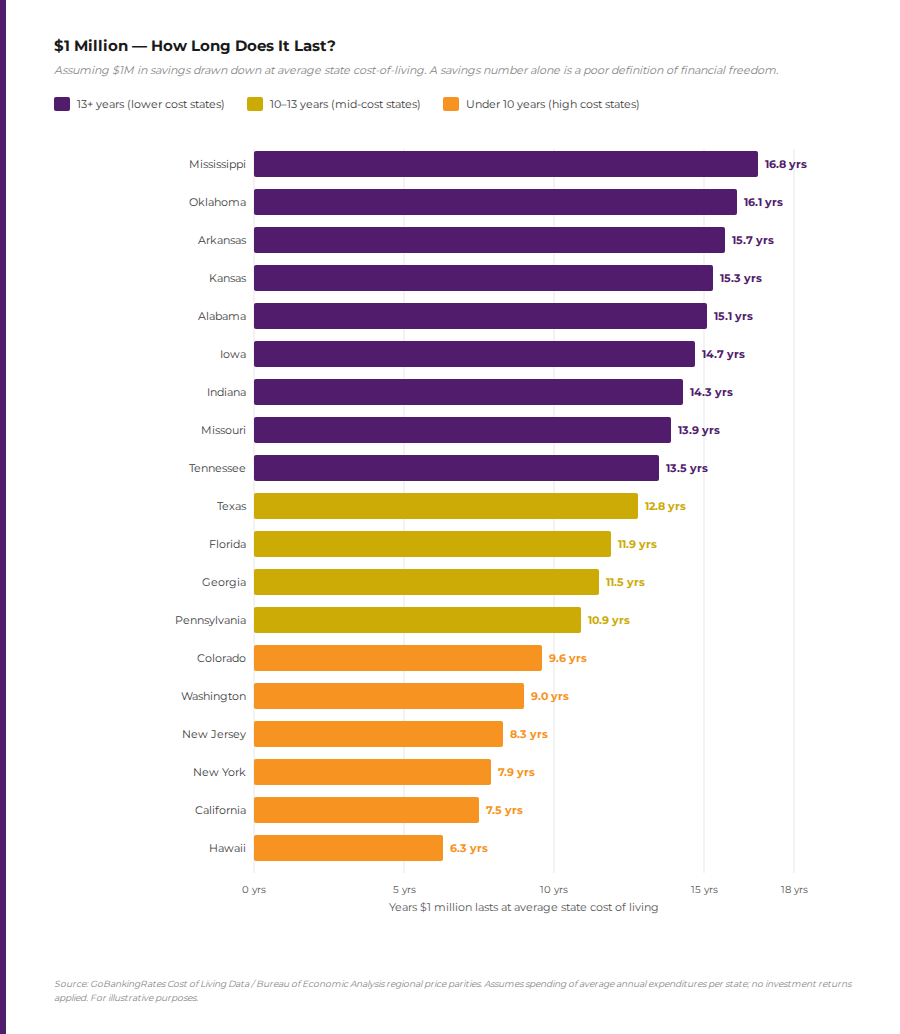

But even if someone achieves the million-dollar milestone, what does it actually provide? As the data shows, $1 million in savings drawn down at average state cost-of-living lasts fewer than eight years in California, New York, and New Jersey. In Hawaii, it lasts just over six. Only in the lowest cost-of-living states does $1 million stretch past 15 years.

This is the first mindset problem: most people are working toward a number that isn’t nearly as meaningful as they’ve been told. The wealthy don’t fixate on a savings target — they build income streams that don’t deplete. Real financial freedom isn’t a lump sum. It’s cash flow that exceeds monthly expenses indefinitely.

Why money alone will never make you rich

The world is full of people who received large sums of money and lost it entirely. Lottery winners, professional athletes, and heirs to large estates routinely blow through fortunes within a few years. Research from the National Endowment for Financial Education consistently finds that a significant percentage of sudden-wealth recipients eventually experience a financial crisis.

The common denominator isn’t bad luck. It’s the absence of a money mindset.

Having money and knowing what to do with money are two entirely different things. Without the frameworks to understand assets, liabilities, cash flow, and taxes, a windfall is just a bigger pile to spend. Robert Kiyosaki’s foundational insight in Rich Dad Poor Dad is precisely this: the problem isn’t a lack of money — it’s a lack of financial education. Money flows toward people who understand it, and away from people who don’t.

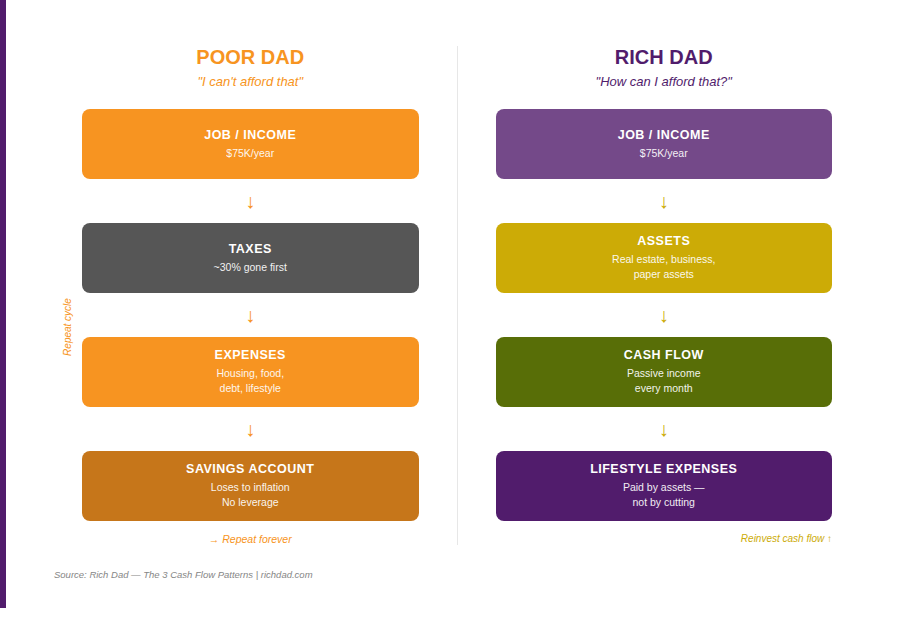

Poor dad vs. rich dad: Two operating systems

In Robert Kiyosaki’s experience, his biological father — his “poor dad” — was highly educated by conventional standards, yet consistently struggled financially. His best friend’s father — his “Rich Dad” — had little formal education, yet built significant wealth. The difference between them wasn’t intelligence or even effort. It was the operating system running in the background of every financial decision.

The Poor Dad mindset operates on a specific sequence: earn income → pay taxes → pay expenses → save what’s left → repeat. This cycle keeps the middle class locked in a pattern where the government takes its share first, expenses absorb the rest, and whatever survives is placed in an account that loses value to inflation year after year.

The Rich Dad mindset runs a different sequence: earn income → acquire assets → let assets generate cash flow → use cash flow to pay expenses and acquire more assets. The critical difference is that the rich build the asset base that generates passive income before they consider lifestyle upgrades — not after.Why money alone will never make you rich

The practical translation of this mindset difference is captured in the question the Poor Dad never asks: “How can I afford that?” Not “I can’t afford that” — but rather, “What would I need to do to afford that?” The first statement ends the inquiry. The second opens a problem-solving process. That reframe is not merely motivational — it changes the actions that follow. As Robert explains across Rich Dad’s financial philosophy, the questions you ask determine the answers you find.

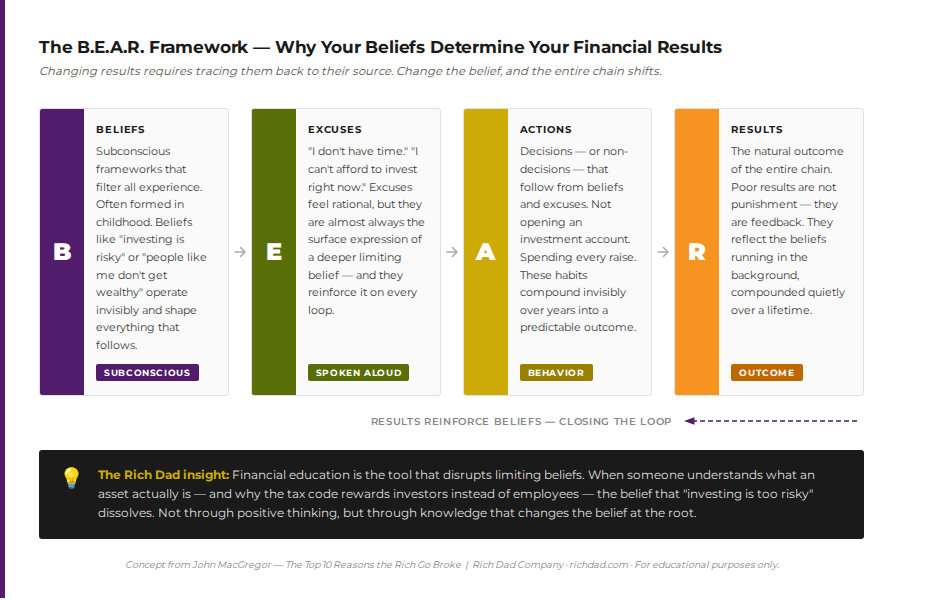

The B.E.A.R. Framework: Why your beliefs determine your bank accountPoor dad vs. rich dad: Two operating systems

Understanding why mindset change is so difficult requires looking at how the mind actually works. In The Top 10 Reasons the Rich Go Broke, author John MacGregor presents a powerful model using the acronym B.E.A.R.

Beliefs are the subconscious frameworks through which all experience is filtered. They are not reality — they are opinions so deeply held they function as facts. Beliefs like “money is hard to earn,” “investing is risky,” or “people like me don’t get wealthy” operate beneath conscious awareness and shape everything that follows.

Excuses are the verbal manifestations of those beliefs. “I don’t have time.” “I don’t have enough money to invest.” “The market is too unpredictable right now.” Excuses feel rational, but they are almost always the surface expression of a deeper, limiting belief. They create a feedback loop that reinforces the original belief and prevents action.

Actions are the decisions — or non-decisions — that follow from beliefs and excuses. Not opening an investment account isn’t a decision; it just becomes the default. Spending every raise on lifestyle upgrades isn’t a choice; it simply feels normal. These actions, compounding over years, produce predictable results.

Results are the natural outcome of the entire system. Poor results are not punishment — they are feedback. They reflect the beliefs operating in the background. As MacGregor writes, changing results requires changing beliefs, which changes excuses, which changes actions. There is no shortcut past this sequence.

Simply put: financial education is the tool that disrupts limiting beliefs. When someone understands what an asset actually is, why a house is not always an asset, and how the tax code is written to reward investors and business owners, the belief that “investing is too risky” often dissolves — not through positive thinking, but through knowledge.

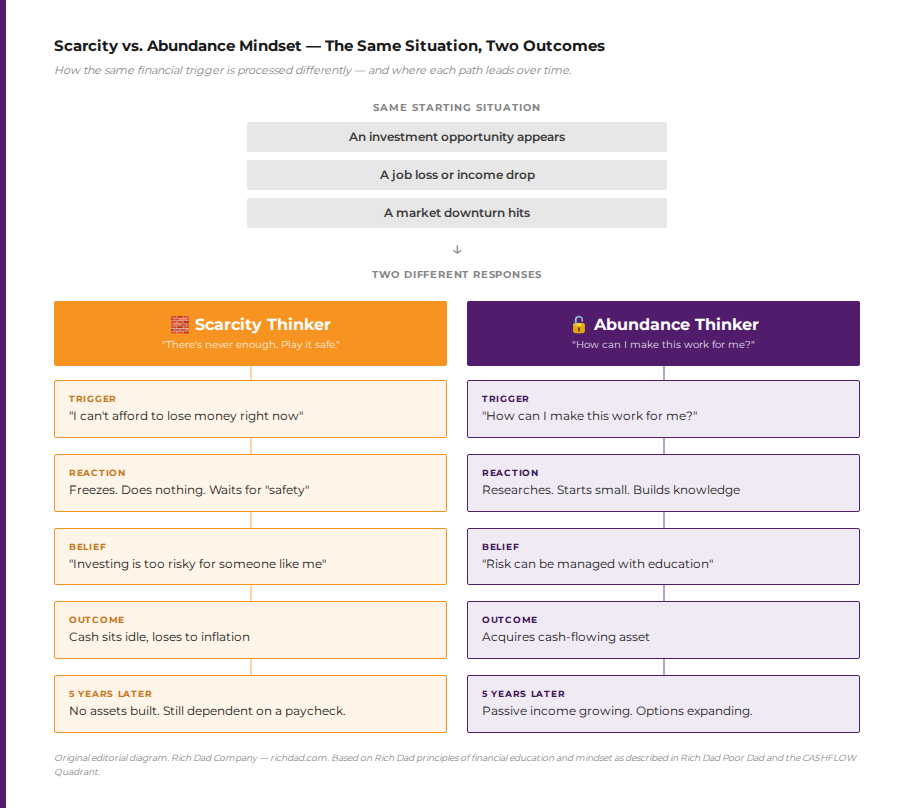

Scarcity vs. abundance: The two money mindsets in action

The scarcity mindset and the abundance mindset are not personality traits — they are conditioned responses, most of which were established in childhood. Research in behavioral finance has documented that most adults operate from deeply ingrained beliefs about money formed before the age of ten. These patterns run on autopilot, shaping financial behavior in ways their owners rarely recognize.

The scarcity mindset produces a specific set of behaviors: hoarding cash rather than deploying it into assets, avoiding investment risk even when the risk is manageable, viewing wealthy people with suspicion rather than curiosity, and treating money as a source of anxiety rather than a tool. The scarcity thinker holds cash because cash feels safe — even as inflation steadily erodes its purchasing power.

The abundance mindset produces a different behavior set: seeking information before reacting to financial challenges, viewing market downturns as buying opportunities rather than disasters, focusing on expanding income rather than merely cutting costs, and treating financial education as an ongoing practice rather than a one-time event.

Crucially, the abundance mindset is not about ignoring risk or engaging in wishful thinking. The goal is educated risk, not reckless risk. A sophisticated investor who understands a deal can manage its risks. An uneducated investor who avoids all risk still faces the guaranteed risk of inflation eating their savings and outliving their money. The question is never whether to take risk — it is always whether the risk is understood and managed.

The four economic ages and the knowledge mindshift

One of Robert Kiyosaki’s most powerful frameworks is his description of the four economic ages of humanity, outlined in Increase Your Financial IQ. Each age required a fundamentally different mindset to generate wealth — and those who failed to make the shift were left behind economically.

In the Hunter-Gatherer Age, wealth was found in nature and the tribe was the social safety net. Wealth was equally distributed because survival was equally demanding.

In the Agrarian Age, those who owned land became royalty; those who worked it became peasants. The mindshift required was from nomadism to cultivation and ownership.

In the Industrial Age, wealth shifted to those who controlled natural resources and could build systems of production. The mindshift was from land ownership to capital formation and manufacturing.

In the Information Age — the era in which the world now operates — wealth is generated by those who can process, leverage, and act on information. For the first time in history, the barrier to wealth creation is not land, capital, or physical resources. It is knowledge.

This last point is critical: the Information Age has democratized the access to information, but it has not democratized the application of it. A person with an internet connection can find every fact about how real estate investing works, how options trading generates cash flow, or how a business entity reduces taxes. But information without the financial intelligence to act on it produces nothing. Knowledge — the earned ability to filter, interpret, and deploy information — is what actually creates wealth.

Robert’s rich dad once put it plainly: crude oil is of little value until it is refined. The knowledge required to refine oil and produce fuel is what creates the wealth — not the oil itself. Today, information is the crude oil, and financial intelligence is the refinery. Mark Zuckerberg didn’t become one of the world’s wealthiest people because he had access to more information than others. He had the knowledge to process that information into systems that generated scalable value.

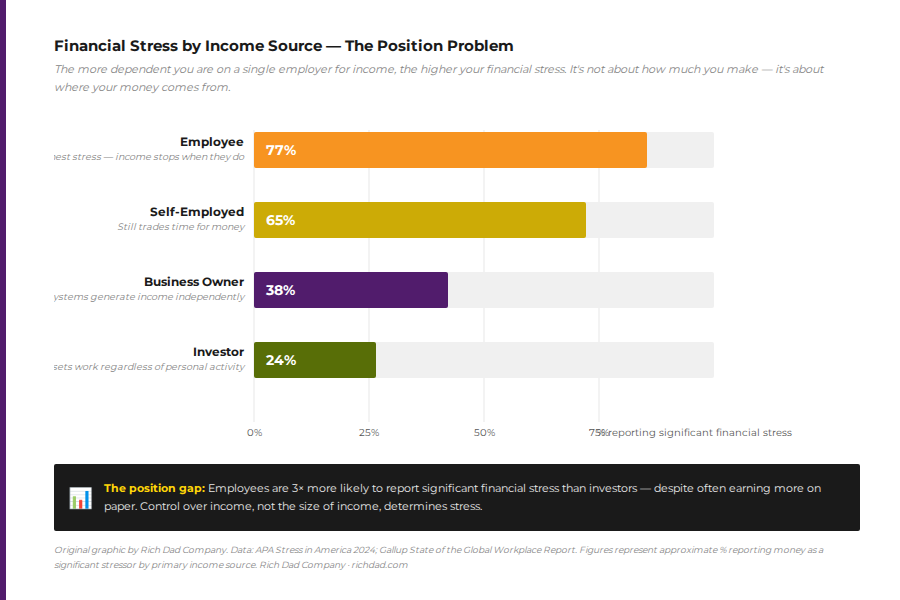

Financial stress and the income position problem

The relationship between a money mindset and financial wellbeing is not merely philosophical — it shows up measurably in financial stress data. Research consistently shows that financial stress is not primarily a function of income; it is a function of how income is structured.

Employees — people whose income stops the moment they stop working — report the highest levels of financial stress. Self-employed individuals report somewhat lower stress, but remain highly dependent on their personal labor. Business owners and investors, whose income is generated by systems and assets rather than personal effort, report dramatically lower financial stress — even when income levels are comparable to those in employment.

This data point reflects the fundamental distinction Robert Kiyosaki draws between the left side and right side of the CASHFLOW® Quadrant. Employees and the self-employed trade time for money. Business owners and investors build systems that generate money whether or not they show up to work. A money mindset — one focused on acquiring assets rather than maximizing earned income — is the bridge between those two worlds. It is not how much someone earns that determines their financial stress; it is whether their income continues when they stop working.

How to start building a money mindset today

Developing a money mindset is not a weekend project. It is a sustained practice of financial education, self-examination, and deliberate action. The following steps represent a practical starting point.

- Audit your current beliefs about money

Before changing financial behavior, it is necessary to understand what beliefs are currently driving it. Where does the belief that “investing is gambling” come from? Who taught that “saving is always virtuous, and spending is always irresponsible”? Uncovering these inherited scripts — and questioning whether they reflect reality or conditioned assumptions — is the first and most important step toward change. - Learn the difference between assets and liabilities

Robert Kiyosaki’s definitions are blunt and intentional: an asset puts money in your pocket. A liability takes money out. By this definition, a personal residence with a mortgage is a liability for most people — not an asset. Understanding this distinction changes the questions someone asks before every financial decision. Explore the distinction further through Rich Dad’s personal finance resources. - Learn the language of financial education

Concepts like cash flow and passive income, good debt versus bad debt, and the velocity of money are not advanced topics — they are foundational financial literacy. Just as learning to read opens access to all written knowledge, financial literacy opens access to the strategies the wealthy use as a matter of routine. Rich Dad’s saving vs. investing content illustrates why what most schools teach about money is incomplete at best and counterproductive at worst. - Understand the tax code and how it rewards asset-builders

As covered in Rich Dad’s personal tax strategies content, the tax code is written to reward business owners and investors with significant deductions, depreciation, and passive income advantages that employees cannot access. Understanding this changes how someone thinks about their relationship with earned income — and motivates the transition toward the right side of the CASHFLOW® Quadrant. - Build a financial education community

The B.E.A.R. framework makes clear that beliefs are social as well as personal — they are reinforced by the people, content, and conversations someone is surrounded by. A network of financially educated peers and mentors accelerates the mindset shift in ways that solitary study cannot. The wealthy have always known this: the people in your closest circle either compound your financial intelligence or erode it.

Invest in you

The money mindset is not about thinking positively about money. It is about thinking accurately. The wealthy do not simply believe they will be rich — they understand how wealth works, why the old rules of money no longer apply, and what specific actions build the kind of passive income that eventually makes employment optional.

Robert Kiyosaki’s framework — from the B.E.A.R. model to the four economic ages to the distinction between the Poor Dad and Rich Dad operating systems — offers something that no savings account and no 401(k) ever will: a set of mental tools for navigating a financial world that rewards knowledge above all else.

The first investment the Rich Dad philosophy recommends is always the same: invest in financial education. Because in the Information Age, knowledge is the new money — and a money mindset is the compound interest that grows it.

FAQs

A money mindset is the set of beliefs, attitudes, and behavioral patterns that govern how a person thinks about, earns, spends, saves, and invests money. Unlike budgeting strategies or investment tactics, a money mindset operates at the level of foundational assumptions — often formed in childhood and reinforced over decades. The Rich Dad framework distinguishes between a scarcity-based money mindset (which drives most people toward job security and savings accumulation) and an abundance-based money mindset (which drives wealth builders toward cash flow, assets, and passive income).

Financial literacy refers to knowledge of specific concepts: how interest rates work, what a balance sheet is, how taxes are calculated. A money mindset is the operating system through which that knowledge — or the absence of it — gets applied. Someone can be financially literate but still operate from a scarcity mindset, avoiding investment risk even when education would reveal it to be manageable. The Rich Dad philosophy treats financial education as the tool that transforms a limiting money mindset into a wealth-building one.

Yes — and behavioral finance research strongly supports this. Beliefs determine actions, and actions compound over time into financial outcomes. Someone who believes “investing is only for the wealthy” will not invest, regardless of how much they earn. Someone who believes “every dollar should be working for me” will consistently seek ways to deploy capital into cash-flowing assets. As Robert Kiyosaki teaches, the gap between a $75,000-per-year employee who retires broke and a $75,000-per-year investor who achieves financial freedom is almost never income — it is mindset and the financial decisions that mindset produces.

The scarcity mindset treats money as a limited resource to be hoarded and protected. It leads to behaviors like excessive risk avoidance, reluctance to invest, and measuring financial success by what’s in a savings account. The abundance mindset treats money as a tool that, when deployed intelligently into cash-flowing assets, multiplies over time. The abundance mindset does not ignore risk — it manages risk through financial education and diversification. Robert Kiyosaki frames this as the difference between asking “I can’t afford that” (which closes inquiry) and “How can I afford that?” (which opens problem-solving).

Research on sudden wealth is consistent: those who receive large sums of money without the mindset and financial intelligence to manage it typically lose it within a few years. Having money and knowing how money works are fundamentally different capabilities. Without understanding assets, liabilities, tax implications, and cash flow, a large sum is simply a bigger pile to spend. The Rich Dad principle is that financial education must precede wealth — otherwise, wealth is temporary. This is why Robert Kiyosaki emphasizes that financial IQ is the single most important investment anyone can make.

The Rich Dad philosophy frames a money mindset as a progression through the four economic ages of human history — from the Hunter-Gatherer Age through the Information Age — with the understanding that each era required a different mindset to generate wealth. In the Information Age, information itself is free and abundant. What separates the wealthy is the financial knowledge to filter, interpret, and act on that information through acquiring assets, building businesses, and creating passive income. The money mindset Robert Kiyosaki teaches is not about motivation — it is about education that leads to intelligent, deliberate action.

Begin with self-examination: identify the inherited beliefs about money that are currently driving financial decisions, and question whether those beliefs are accurate or limiting. From there, the foundational shift is learning the difference between assets and liabilities, understanding how passive income differs from earned income, and studying how the tax code rewards business owners and investors rather than employees. Building financial literacy through Rich Dad’s educational resources provides the knowledge that challenges scarcity-based beliefs and replaces them with wealth-building frameworks.