The millennial financial paradox: More educated, less financially literate

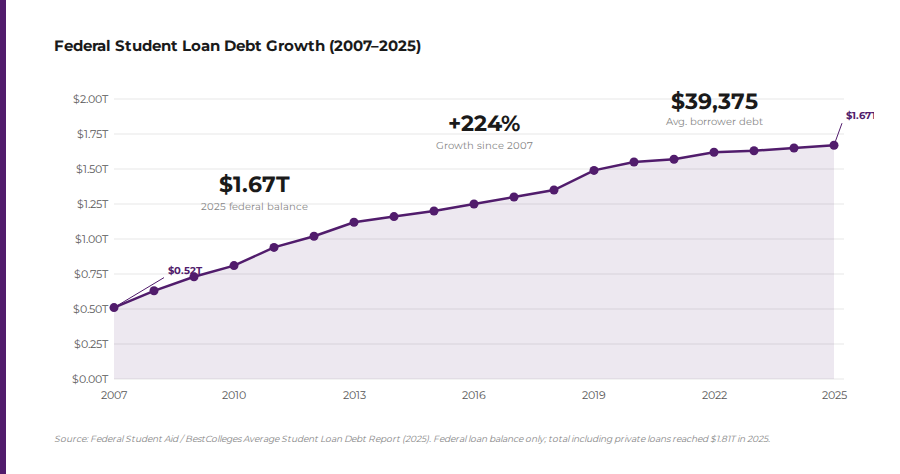

Millennials are the most credentialed generation in American history. According to the Pew Research Center, more millennials have four-year college degrees than any prior generation. Yet that academic achievement came attached to a financial anchor that previous generations never carried: an average of $39,000 in student loan debt per borrower, and a national total that has reached $1.67 trillion as of 2025 — a 224 percent increase since 2007.

Universities teach history, engineering, literature, and law. They do not teach how compound interest works against borrowers. They do not explain the difference between earned income and passive income, or why the former is taxed at the highest rate while the latter enjoys the lowest. They graduate millions of students every year who know nothing about how to read a financial statement, evaluate an investment, or build an asset column.

This is not accidental. It is a system that produces skilled employees — people who know how to add value to someone else’s enterprise. What it does not produce, by design, is financially independent individuals who know how to build enterprises of their own.

Three real economic headwinds millennials are navigating

The challenges millennials face are structural, not personal. Understanding them clearly is the first step to navigating around them. Three forces in particular have shaped this generation’s financial landscape in ways that prior financial advice was never equipped to address.

1. The job market has fundamentally changed

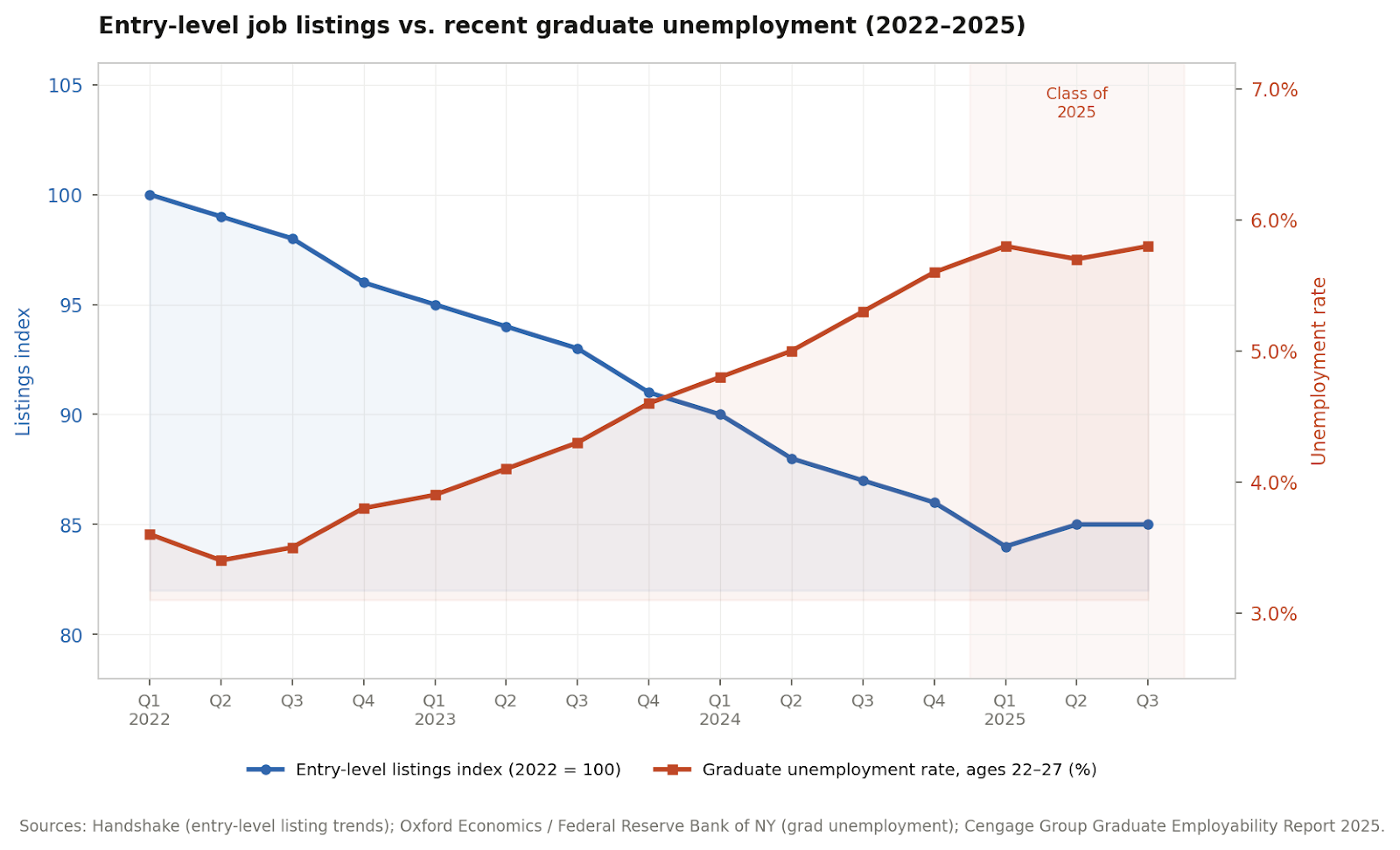

Entry-level job listings have fallen sharply since 2022, even as graduate unemployment has climbed. According to data tracked by Handshake and the Federal Reserve Bank of New York, the entry-level listings index dropped from 100 in 2022 to approximately 85 by mid-2025, while graduate unemployment for ages 22–27 rose toward 6 percent. Simultaneously, AI is displacing the entry-level tasks that a college degree traditionally unlocked, from report drafting to basic research to routine analysis. The credential no longer automatically delivers the economic return it once promised.

2. Housing affordability has become generational

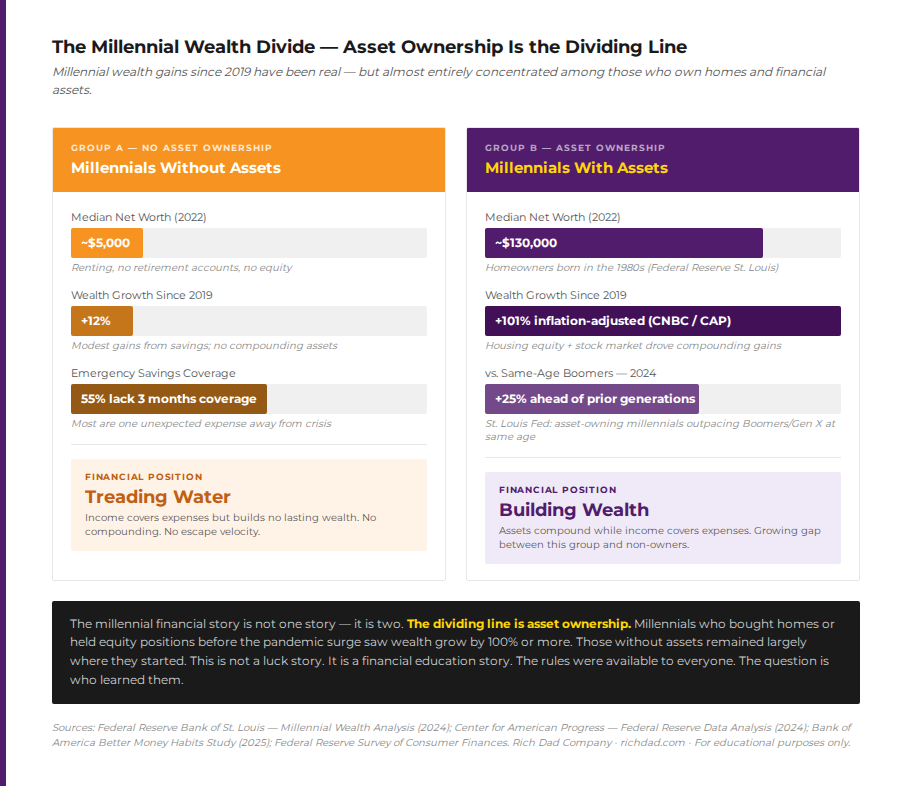

The homeownership divide is arguably the single largest factor separating millennials who are building wealth from those who are not. According to a St. Louis Fed analysis, median net worth for older millennials (born in the 1980s) rose from approximately $60,000 in 2019 to $130,000 in 2022 — almost entirely driven by home equity gains. Those who did not own homes saw no comparable windfall. Harvard’s Joint Center for Housing Studies now estimates that it takes a household income of at least $100,000 to afford the median-priced home in nearly half of all U.S. metro areas. For many millennials, homeownership remains structurally out of reach — which makes acquiring investment-grade real estate through alternative approaches all the more important.

3. The conventional retirement system is failing them

The 401(k) was never designed as a comprehensive retirement vehicle. It was a tax-deferred savings mechanism, introduced in 1978, that corporations adopted as a way to shift retirement risk from employer to employee. According to the Federal Reserve’s Survey of Consumer Finances, median retirement savings for millennials approaching 40 remain far below what is needed for a 30-year retirement. Worse, a traditional 401(k) defers taxation until withdrawal — which means millennial retirees who funded only this vehicle will owe taxes on every dollar they withdraw, potentially at higher future rates. Rich Dad’s philosophy on saving and investing addresses why this approach falls short and what to pursue instead.

The millennial wealth divide: Why the gap is widening within the generation

Perhaps the most important and underreported story about millennial finances is not how they compare to other generations — it is how dramatically they compare to each other. The average millennial net worth grew 12.74 percent in 2024 and has roughly doubled since 2019. But those gains were almost entirely concentrated among asset holders: those who owned homes before the pandemic price surge, who held equity-market positions through the recovery, and who had investment accounts benefiting from a decade-long bull market.

For the millennials who entered adulthood without access to inherited wealth, who graduated into the 2008 recession, who rented through the housing boom, and whose savings sat in low-yield accounts while inflation eroded purchasing power — the gains were minimal. Bank of America’s 2025 Better Money Habits study found that more than half of younger adults still cannot cover three months of expenses from savings. The generation is not monolithic. It is split into those who were in the right financial position at the right time — and those who were not.

This is not a message of despair. It is a message of clarity. The dividing line between these two groups is not luck or birth order. It is asset ownership — and asset ownership is a learnable, teachable, actionable goal for anyone willing to study how money actually works.

What the conventional advice actually costs millennials

Follow the conventional playbook and its costs are concrete and measurable. An employee in the E-quadrant — trading time for a salary — faces an effective federal tax rate of approximately 35.7 percent, according to IRS Statistics of Income data analyzed by the Tax Foundation. That is before state taxes. Meanwhile, an I-quadrant investor with the same gross income — drawing from rental property income, dividends, and capital gains — may pay an effective rate closer to 15 percent, thanks to depreciation deductions, passive loss rules, and preferential tax treatment of long-term capital gains. That 20-point gap, compounded over a career, is not a rounding error. It is the difference between building wealth and funding the government’s operations.

The conventional retirement vehicle — the 401(k) — introduces another hidden cost: deferred taxation without financial education. Employees are told to “set it and forget it,” handing control of their wealth to mutual fund managers who charge fees regardless of performance. According to research compiled by NerdWallet, a 1 percent annual fee on a 401(k) balance can consume as much as 28 percent of a retiree’s final nest egg over a 35-year career, thanks to compounding. Millennial workers funding this system are not building financial literacy. They are building dependency.

None of this means millennials should avoid contributing to retirement accounts. It means they should understand what those accounts are, what they are not, and what else is available — particularly cash-flowing assets that generate income now rather than in four decades.

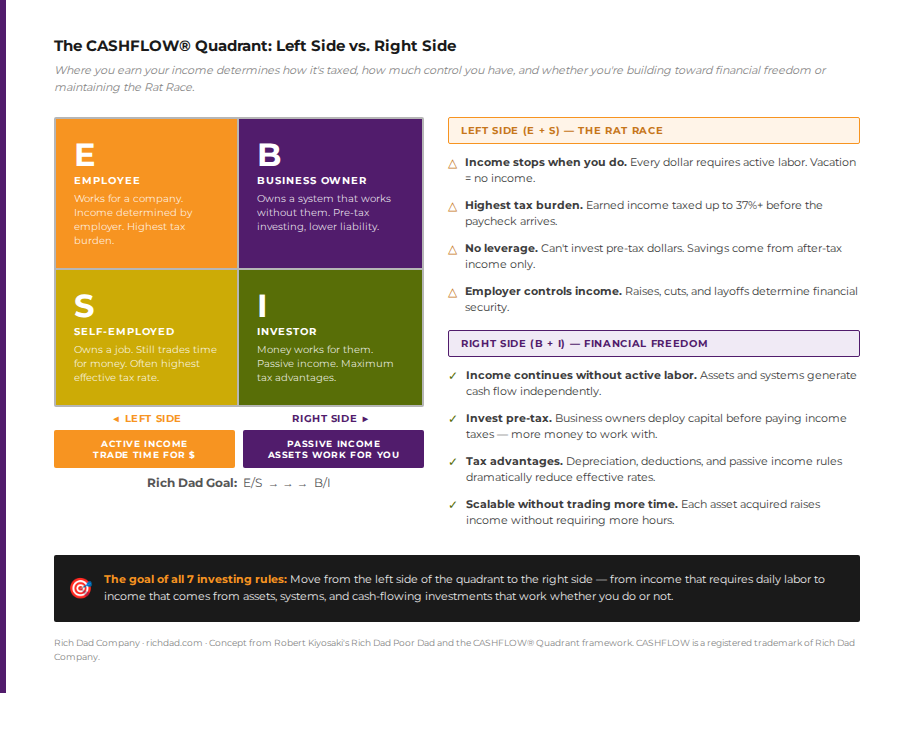

The CASHFLOW Quadrant: A framework built for the millennial moment

Robert Kiyosaki’s CASHFLOW Quadrant divides all income earners into four categories: Employee (E), Self-Employed (S), Business Owner (B), and Investor (I). Most millennials have been trained — by their parents, their schools, and society — to aim for the E or S quadrant. These quadrants offer the highest tax burden and the lowest scalability. Every dollar of E-quadrant income stops when the work stops.

The B and I quadrants operate by different rules entirely. A business owner’s income comes from a system that functions without continuous labor. An investor’s income comes from assets — real estate, stocks, businesses — that generate cash flow whether the owner is working or sleeping. The tax code rewards this shift dramatically. Moving from left-side to right-side income is not simply a career choice. It is the most impactful financial decision any millennial can make — and it begins with understanding the quadrant.

How millennials build wealth: The Rich Dad framework in action

The practical question is not whether financial education matters — it clearly does. The question is what it looks like applied to millennial circumstances. Rich Dad’s framework translates into several concrete, actionable shifts.

- Know your financial statement

Track income and expenses, list assets and liabilities honestly. Most millennials have never seen a personal financial statement. Building one — and updating it monthly — creates the awareness that drives better decisions. The personal financial statement is where financial education becomes personal. - Understand the three types of income

Earned income from a job is the most taxed and least scalable. Portfolio income from dividends and capital gains is more favorably taxed. Passive income from real estate or business distributions carries the lowest effective tax rate and the highest freedom. Shifting the income mix from earned toward passive is the long game every millennial should be playing. Learn more in Rich Dad’s section on investing. - Invest for cash flow, not appreciation

The millennials who benefited from the pandemic-era housing boom did so largely by accident — they bought before values surged. That kind of appreciation is not a strategy. A rental property that generates $300 in positive cash flow every month is an asset. A home that costs $2,200 per month and produces nothing is a liability. The distinction determines the financial outcome. Explore real estate investing strategies that prioritize cash flow. - Build financial intelligence as a skill

Financial education is not a one-time event. It is a practice. Millennials who commit to ongoing learning — through books, seminars, mentors, and applied experience — develop the confidence and competence to act when opportunities arise. Those who remain financially illiterate remain dependent. The financial education Rich Dad provides is designed to be practical, not academic. - Start the entrepreneurship path

More millennials are starting businesses than any prior generation, driven partly by economic necessity and partly by the recognition that employment alone is not enough. The business owner’s ability to invest pre-tax dollars, deduct expenses, and build systems that generate income independently of their labor is a structural advantage. Rich Dad’s entrepreneurship resources cover the practical mechanics of moving from self-employed to true business owner.

Millennial money mindset: From scarcity to strategy

One of the most consistent findings in research on millennial finances is the role of mindset. CNBC’s reporting on millennial financial struggles quotes economist Rachel Schneider describing a large portion of Americans as living “at break even” — making enough to cover expenses, but without the buffer or the strategy to build beyond that. That is a scarcity mindset in economic form: surviving rather than building.

Let’s identify the distinction between a scarcity mindset — which causes people to cut expenses, avoid risk, and look for safety — and an abundance mindset, which causes people to look for opportunities to expand their income, acquire assets, and take calculated risks with proper financial education behind them. Neither mindset is simply a personality trait. Both are learned. And one of them is systematically taught to millennials through every institution they encounter, while the other is almost entirely absent from conventional education.

The fear of losing money keeps many millennials out of investing entirely. The same dynamic Robert identified in earlier generations applies here: people who are afraid to lose hold onto losing positions too long and sell winning ones too soon. Financial education creates the emotional neutrality required to make rational investment decisions — to cut losses without shame, ride winners without greed, and make decisions based on analysis rather than fear.

The most important investment any millennial can make

The narrative around millennial finances has oscillated between two poles: blame and excuse. Either millennials are accused of financial irresponsibility, or they are portrayed as helpless victims of structural forces beyond their control. Both ought to be rejected.

The structural challenges are real. Student debt is real. Housing affordability is real. Wage stagnation is real. But so is the fact that a growing number of millennials — those who sought financial education, acquired assets, and built income streams outside their employment — have pulled ahead of every prior generation at the same age. The dividing line is not systemic advantage. It is financial knowledge applied over time.

The most important investment any millennial can make is not in a specific stock, a particular property, or a side hustle. It is in financial education — the foundational literacy that makes every subsequent financial decision better. It is understanding assets versus liabilities, the tax advantages of different income types, the mechanics of cash flow investing, and the psychological discipline that separates winners from losers in any market.

Millennials did not receive that education in school. But they can choose to receive it now. And that choice — made today, applied consistently — is still early enough to change everything.

FAQs

Millennials face a combination of structural headwinds — record student debt averaging $39,000 per borrower, housing markets that have outpaced wage growth, a gig economy with inconsistent income and no employer benefits, and a job market increasingly disrupted by AI. But the deepest problem is not structural: it is the absence of financial education. Millennials were taught to earn income as employees, save in tax-deferred retirement accounts, and treat a primary home as their biggest asset. None of those strategies builds genuine financial freedom, which requires understanding cash-flowing assets, passive income, and the tax advantages available to investors and business owners.

Millennial wealth has grown significantly since 2019, but that growth is sharply uneven. Millennials who owned homes or held equity investments captured most of those gains. Those without assets saw minimal growth. The generation is not uniformly succeeding or failing — it is bifurcating based on asset ownership.

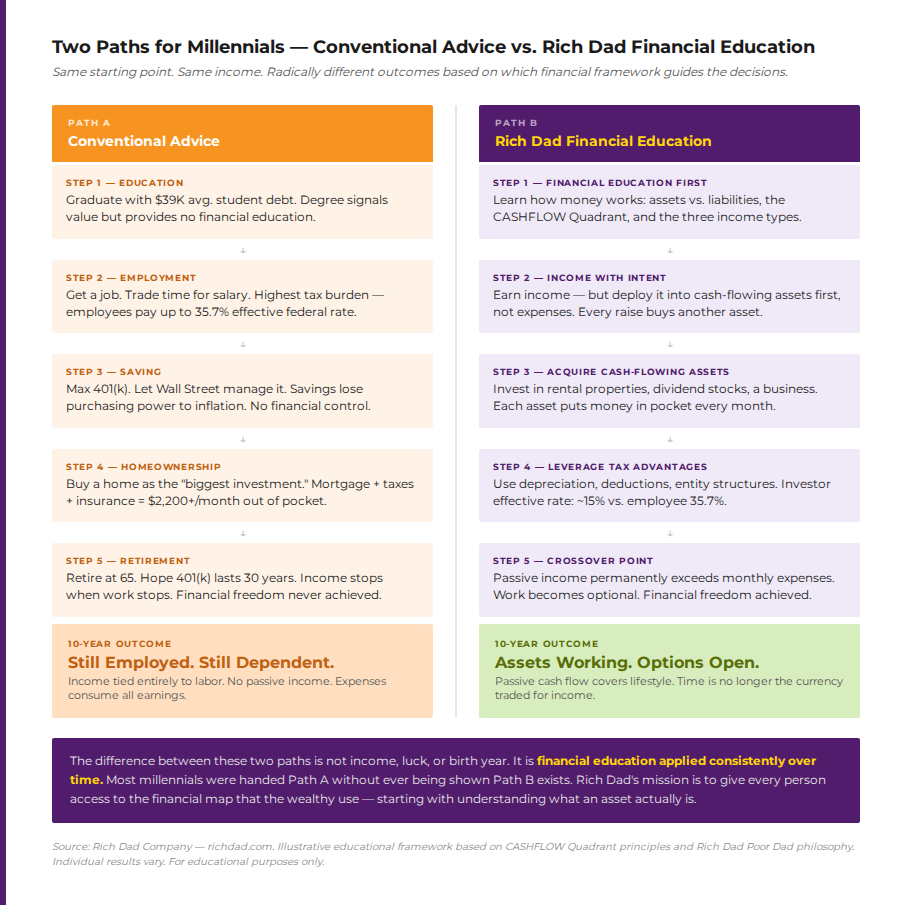

Simply put, millennials need the advice they were never given. Millennials need to understand the difference between assets and liabilities, the four income types and their tax implications, the CASHFLOW Quadrant and how to move from the E/S side to the B/I side, and the mechanics of cash flow investing across real estate, business, and paper assets. Conventional financial advice — save more, diversify your 401(k), pay off debt — is not wrong, but it is incomplete. It describes how to maintain a position, not how to build toward financial freedom.

The first step is financial education — learning how money works before putting it to work. The second step is tracking and adjusting the personal financial statement: reducing liabilities and directing income toward asset acquisition rather than lifestyle inflation. The third is identifying the lowest-barrier asset class appropriate to the individual’s skills and knowledge — which might be dividend-paying stocks, a small rental unit through house hacking, or a side business that generates income independent of a primary job. The goal is to build the first unit of passive income, however small, and compound from there.

The argument here isn’t that millennials are permanently disadvantaged — rather, the argument focuses on the fact that they were handed a financial playbook that was already outdated when it was written. The advice to go to a good school, get a stable job, and invest in a diversified stock portfolio made sense in a post-war economy with defined-benefit pensions, low housing costs, and stable employment. It does not map cleanly onto an economy characterized by gig work, $400,000+ median home prices, AI job displacement, and a retirement system that transfers all risk to the individual. Millennials need a new framework — not an update to the old one.

The CASHFLOW Quadrant, developed by Robert Kiyosaki, categorizes income sources into four types: Employee (E), Self-Employed (S), Business Owner (B), and Investor (I). The left side — E and S — is characterized by active income that stops when work stops, limited scalability, and the highest tax burdens. The right side — B and I — generates income from systems and assets, scales without proportional time investment, and benefits from dramatically lower effective tax rates. Most millennials occupy the E quadrant exclusively. Financial freedom, is achieved when right-side income permanently exceeds monthly expenses. Understanding the quadrant is the map; financial education is the vehicle.

Student debt is one of the most significant structural barriers to millennial wealth building. With the national federal student loan balance reaching $1.67 trillion in 2025 and average per-borrower debt at $39,375, many millennials spend their early earning years directing income toward debt service rather than asset acquisition. This delays the compounding process that wealth building depends on. Rich Dad’s approach is not to avoid addressing debt — good debt versus bad debt is a critical distinction — but to build asset income simultaneously so that passive cash flow eventually covers both debt obligations and living expenses, accelerating the path to financial independence.