The “live below your means” myth: Why conventional wisdom falls short

The case for living below your means sounds airtight. Spend less than you earn, save the difference, invest in a 401(k), and retire comfortably in 40 years. It’s the cornerstone of mainstream personal finance, championed by everyone from Dave Ramsey to the frugality blogging community.

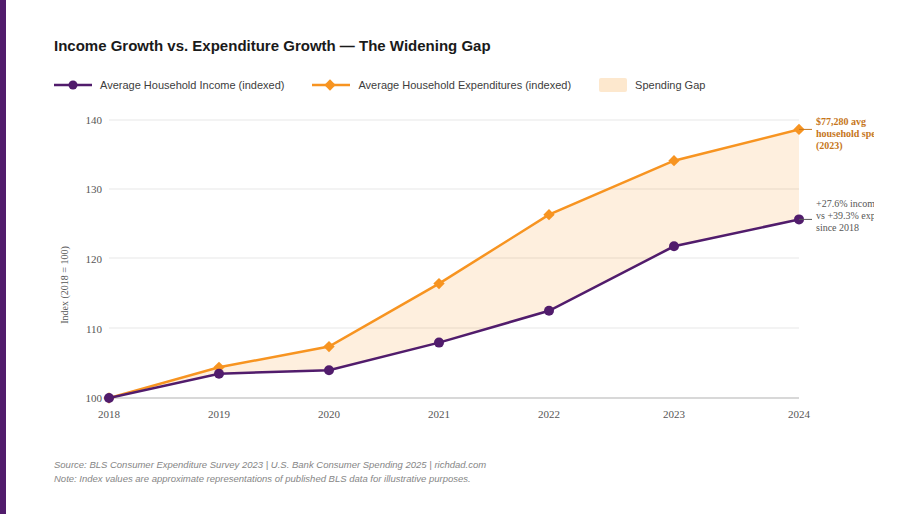

But the math tells a more complicated story. Bureau of Labor Statistics data shows average American household expenditures hit $77,280 in 2023 — up $15,946 from 2020. At the same time, wages and salaries grew only 3.6% over the 12 months ending mid-2025, barely outpacing inflation. The gap between what people earn and what a comfortable life actually costs keeps widening. Cutting lattes doesn’t close that gap. It just makes people miserable while the gap grows.

The deeper problem is that “live below your means” addresses the symptom, not the disease. The symptom is that expenses exceed income. The disease is that income isn’t growing fast enough — and the only cure is building assets that generate cash flow. Cutting spending is static. Building assets is compounding. One approach keeps a person treading water; the other moves them toward shore.

Rich Dad’s core philosophy makes the distinction plainly: only poor people live below their means. The wealthy don’t restrict their lifestyles to match their income — they expand their income to support their lives. That’s not a comfortable message for the financial establishment, but it’s the operating principle behind every wealthy person who didn’t inherit their fortune.

Poor dad vs. rich dad: Two answers to “I can’t afford that”

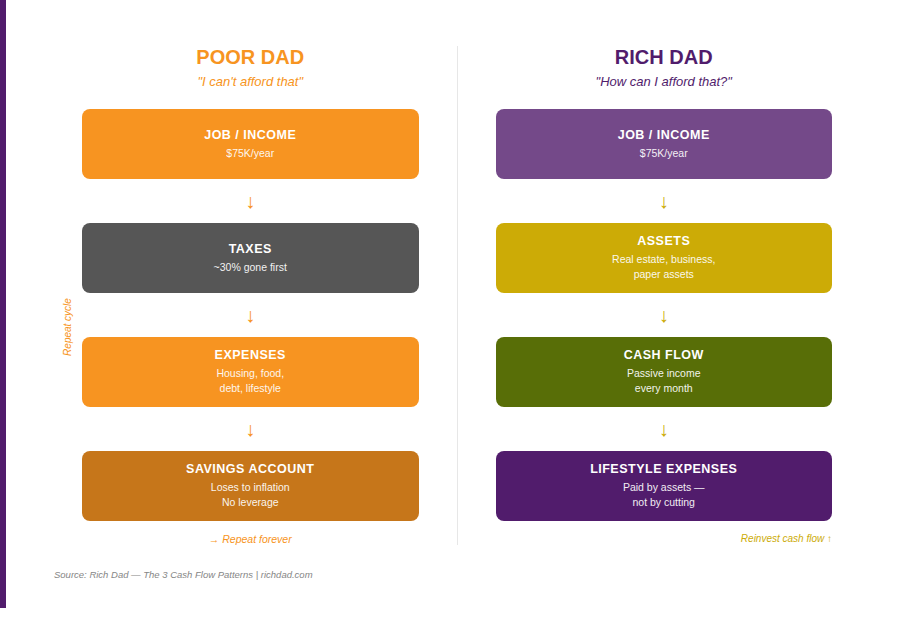

Robert Kiyosaki watched this contrast play out in real life. His poor dad — educated, respected, well-employed as Hawaii’s superintendent of schools — responded to financial wants with a closed statement: “We can’t afford that.” He meant it as responsible parenting. He was teaching his children to live within limits.

His rich dad responded to the same situation with an open question: “How can I afford that?” The difference seems subtle. It isn’t. A closed statement ends a conversation. An open question starts one. One trains the brain for scarcity; the other trains it for problem-solving.

Poor dad, despite his credentials and career, struggled financially his entire life. He never built meaningful assets. At the end of his life, he had little to leave behind. Not because he was lazy or unintelligent — by conventional measures, he was remarkably successful. But his money mindset was fundamentally broken. He knew how to earn. He didn’t know how to build.

Rich dad knew the difference between assets and liabilities — the foundational lesson of Rich Dad Poor Dad. He didn’t restrict his spending. He acquired assets that generated cash flow to cover his expenses. When Robert wanted a Bentley, rich dad didn’t say “cut your budget.” He said acquire an asset that produces enough cash flow to pay for it — then enjoy it. Six months of disciplined investing produced exactly that result.The “live below your means” myth: Why conventional wisdom falls short

The case for living below your means sounds airtight. Spend less than you earn, save the difference, invest in a 401(k), and retire comfortably in 40 years. It’s the cornerstone of mainstream personal finance, championed by everyone from Dave Ramsey to the frugality blogging community.

What it actually means to expand your means

Expanding your means is not a license to overspend. It is a discipline — a specific, intentional practice of acquiring income-producing assets before acquiring liabilities. The sequence matters enormously.

In the conventional model, the sequence is: earn income → spend on lifestyle → save whatever remains → hope it compounds. The Rich Dad model inverts the middle: earn income → acquire assets → let assets generate cash flow → use cash flow to fund lifestyle. In the second model, the lifestyle is funded by assets, not by labor. That makes it scalable and, eventually, self-sustaining.

The practical application looks like this. Instead of cutting $300 per month from a budget to afford something, a Rich Dad investor asks what asset they could acquire whose cash flow generates $300 monthly. A small rental property, a dividend-producing stock position, an options strategy — all of these can generate recurring income. Once the asset is in place, the $300 is no longer a budget sacrifice. It arrives every month from the asset while the asset also continues appreciating.

This is the core of Rich Dad’s investing philosophy: acquire assets that put money in your pocket. Everything else — the lifestyle, the nice things, the experiences — gets funded by the assets, not by restricting your enjoyment of life. The goal isn’t deprivation. The goal is building the income engine that makes deprivation unnecessary.

The lifestyle inflation trap

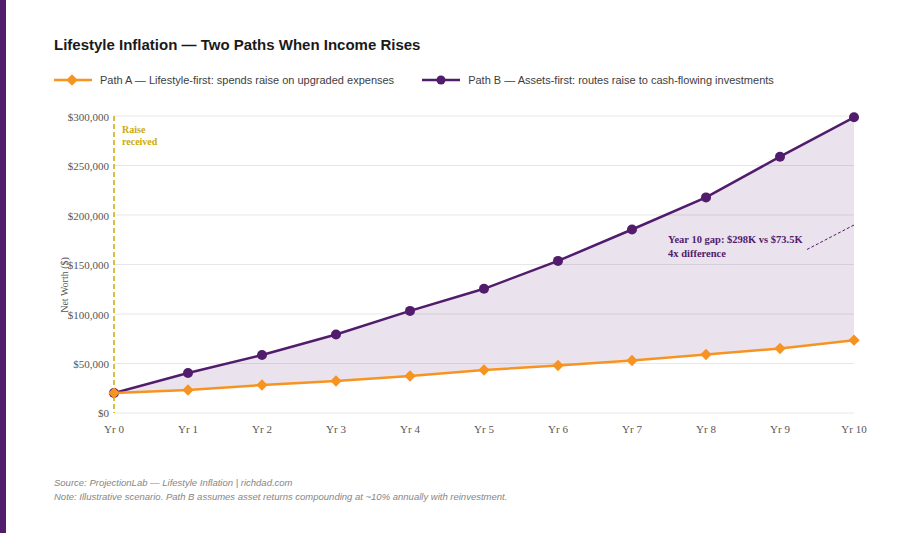

One genuine financial danger that “live below your means” advocates correctly identify is lifestyle inflation — the tendency for spending to rise proportionally with income. Research on lifestyle inflation confirms the pattern: as income rises, expenses tend to rise to match or exceed it, leaving the same financial gap regardless of how much someone earns. This is why salary increases alone rarely produce wealth.

The mainstream solution is restraint: when income rises, keep expenses flat and bank the difference. The Rich Dad solution is direction: when income rises, route the new income toward assets first, then let the assets fund any lifestyle upgrade. The restraint model creates a savings account. The direction model creates a wealth engine. Rich Dad’s guide to saving explains why savings sitting in a bank account lose value to inflation — and why investing in cash-flowing assets is the only real cure for the lifestyle inflation problem.

Why minimalism is just “live below your means” in disguise

Every generation repackages the same underlying scarcity mindset in new clothing. For the current era, it’s minimalism — the philosophy that freedom comes from owning less and spending less. Marie Kondo it. Downsize. Opt out of consumerism. The aesthetics change. The underlying instruction doesn’t: constrict your life to match your income.

Here’s a pointed critique of minimalism: it addresses spending as a symptom without diagnosing income as the actual variable to change. If someone genuinely prefers a minimalist lifestyle, that’s a personal choice with legitimate merit. But minimalism framed as financial strategy — as a path to wealth — is misdirection. People who live minimally and invest nothing end up with minimalism plus poverty. People who invest aggressively and happen to live modestly end up wealthy. The lifestyle is incidental; the investing is causal.

The moralism built into minimalism advocacy makes it particularly insidious. The frugality community doesn’t just say spend less — it implies that spending is morally suspect and that frugality is virtuous. That framing makes it harder to question, because questioning it seems like defending greed. But the question isn’t whether spending is virtuous. The question is whether cutting spending builds wealth. According to Rich Dad, it doesn’t — not on its own. Building cash-flowing assets builds wealth. Everything else is window dressing.

The CASHFLOW Quadrant: Why employees are structurally disadvantaged

The “live below your means” advice is almost exclusively directed at employees — people on the left side of the CASHFLOW Quadrant. Employees trade time for money. Their income has a hard ceiling: there are only so many hours in a day, and most employers won’t pay unlimited overtime. For employees, the only financial levers available are to earn more (limited) or spend less (also limited). “Live below your means” is the only tool they have, and it’s a blunt one.

Business owners and investors on the right side of the Quadrant don’t face this structural limitation. Business income doesn’t have an hours ceiling — a well-built system generates income whether the owner is working or not. Investment income doesn’t require labor at all. For right-side Quadrant participants, the question is never “How do I cut expenses?” It’s always “How do I build another income stream?”

This is why Rich Dad encourages everyone to begin moving toward the right side of the Quadrant — not by quitting their jobs overnight, but by starting to build assets and income streams outside of employment. Starting a business, acquiring rental real estate, generating options income from paper assets — each of these moves income-generation off the time-for-money treadmill and onto assets. “Live below your means” is advice for people trapped on the left side of the Quadrant. Expanding your means is advice for people who intend to leave it.The lifestyle inflation trap

Expand your means: The Rich Dad action plan

Shifting from a “live below your means” mindset to an “expand your means” mindset isn’t just philosophical — it requires a concrete change in behavior. Here is the framework Rich Dad applies:

Step 1: Stop saying “I can’t afford that” — start asking “How can I afford that?”

This single habit change restructures the brain’s relationship with money. Closed statements produce resignation. Open questions produce strategies. Every time the impulse to say “I can’t” arises, replace it with a genuine question about what asset or income stream could make it possible.

Step 2: Identify one liability you want and reverse-engineer the asset that pays for it.

Don’t buy the thing yet. Instead, calculate what monthly cash flow would cover it. Then research what asset would generate that cash flow. A rental property cash-flowing $500/month covers a $500/month car payment. Buy the asset first. Enjoy the liability with the asset’s income.

Step 3: Build financial intelligence in one asset class.

Rich Dad recommends mastering one asset class before diversifying. Use Rich Dad’s investing education hub, books, and tools like the CASHFLOW board game to understand how cash-flowing assets actually work before deploying capital.

Step 4: Use good debt, not zero debt.

The conventional “live below your means” crowd typically preaches debt elimination. Rich Dad distinguishes between good debt and bad debt. Bad debt funds depreciating liabilities. Good debt funds cash-flowing assets. A mortgage on a rental property generating $500/month net is good debt — the asset pays the debt and then some. Eliminating all debt means eliminating the leverage that lets ordinary investors control extraordinary assets.

Step 5: Optimize the tax strategy.

High-income employees pay the highest effective tax rates. Business owners and investors pay the lowest, thanks to legal deductions, depreciation, and preferential capital gains treatment. Personal tax strategies and business tax strategies represent one of the most powerful — and most overlooked — components of expanding your means. Keeping more of what you earn is mathematically equivalent to earning more.

Step 6: Reinvest cash flow into more assets.

The compounding principle works in reverse too: a person who spends all their cash flow never escapes the cycle. The discipline in the Rich Dad model isn’t restricting lifestyle — it’s directing new income toward assets before lifestyle upgrades. Over time, the asset base grows large enough that cash flow exceeds any reasonable lifestyle expense. That is financial freedom: passive income exceeding monthly expenses.The CASHFLOW Quadrant: Why employees are structurally disadvantaged

The Bentley Principle: Acquiring assets before luxuries

Robert Kiyosaki’s Bentley story is one of the most clarifying illustrations of expanding your means in action. When he wanted the car, the conventional approach would have been to save up for it or simply decide it was too expensive and scale back his desires. Instead, he invested in assets that, within six months, generated enough monthly cash flow to cover the car’s cost entirely.

The result: he got the car. He kept his capital. His assets continued growing. And his wealth increased because the assets he acquired to fund the car exceeded the car’s cost in total return. The Bentley became, paradoxically, a wealth-building tool — because the decision to acquire it through assets rather than savings forced him to build a more productive investment position.

This is the Bentley Principle in practice: use desired purchases as motivation to build assets, not as reasons to cut spending. Every material goal becomes an investment target. Every luxury becomes a prompt to ask, “What asset will generate the income to pay for this?” The goal isn’t the luxury — it’s the asset. The luxury is just the measuring stick for how productive the asset needs to be.

Most people — conditioned by poor dad thinking — will read this and say it requires more money than they have. It doesn’t. It requires a different mindset about what to do with the money already coming in. Even modest amounts, systematically directed toward assets rather than expenses, produce dramatically different outcomes over time. The starting point is less important than the direction.

The richest people don’t live below their means

Study any wealthy person who built their fortune rather than inheriting it, and one thing is consistent: they did not get there by living below their means. They got there by expanding their means — by building businesses, acquiring real estate, investing in assets that generated income independent of their labor hours.

“Live below your means” isn’t useless advice. It contains a kernel of truth: spending on liabilities that produce no income is a path to poverty regardless of income level. But the kernel has been inflated into a full strategy, and as a strategy it fails. It caps aspiration, closes mental doors, and keeps hardworking people treadmilling through decades of budget cuts that never quite produce the financial security they promised.

The Rich Dad alternative is more demanding intellectually — it requires learning about assets and liabilities, understanding how cash flow works, developing financial intelligence, and taking action where most people stay comfortable. But it produces a fundamentally different outcome: not a life scaled down to fit an income, but an income scaled up to fund the life someone actually wants.

The question worth asking isn’t “What can I cut?” It’s “What can I build?”

FAQs

Rich Dad calls it a scam because it trains people to think in terms of scarcity and restriction rather than creation and abundance. The advice addresses financial struggle by compressing lifestyle rather than expanding income — which means the underlying problem (insufficient income-producing assets) never gets solved. People following this advice work hard, spend less, and still don’t build wealth because they never learn to acquire assets.

Rich Dad doesn’t advocate overspending. The argument is against the specific mindset of “I can’t afford that,” which shuts down creative thinking about income expansion. The goal is to acquire assets first, then use their cash flow to fund expenses — including luxuries. This is the opposite of reckless spending; it’s deliberate, asset-first financial planning.

Expanding your means means acquiring income-producing assets — rental properties, businesses, dividend-paying investments, or paper asset strategies like covered calls — whose cash flow covers desired expenses. The classic Rich Dad example: instead of saving up cash to buy a Bentley, Robert Kiyosaki invested in assets that generated enough monthly income to pay for the car. He got the car, kept his capital, and his net worth increased.

It’s important to distinguish between good debt and bad debt. Bad debt funds liabilities — things that take money out of your pocket (consumer goods, depreciating vehicles bought on credit). Good debt funds assets — things that put money into your pocket (rental properties, businesses). The expand-your-means approach uses good debt to acquire cash-flowing assets, not bad debt to fund a bigger lifestyle before the assets exist.

Rich Dad’s position is that minimalism as a lifestyle philosophy is a personal choice with no right or wrong answer. But minimalism promoted as a wealth-building strategy is misdirection. Owning fewer things doesn’t build wealth — acquiring assets does. Someone who lives minimally and builds no assets will be both minimal and broke. Someone who builds assets and happens to prefer a simple lifestyle will be both minimal and wealthy. The lifestyle is incidental to the outcome.

Rich Dad recommends starting with financial education before capital deployment. Understand the asset class before investing in it. Use tools like the CASHFLOW board game and Rich Dad’s investing courses to build financial intelligence. Then identify one small income-producing asset — a single rental unit, a dividend-paying stock position, a side business — and build from there. The starting amount matters less than the direction: every dollar should be building toward an asset that generates cash flow.

Savings accounts lose purchasing power to inflation over time — Rich Dad’s guide to saving explains why savers are, in effect, losers in today’s monetary system. Money sitting in a 4% savings account while inflation runs at 3% produces minimal real gains, no tax advantages, and no compounding leverage. Investing in cash-flowing assets — real estate, businesses, paper assets — produces income, appreciation, tax benefits, and leverage. Saving is not investing.