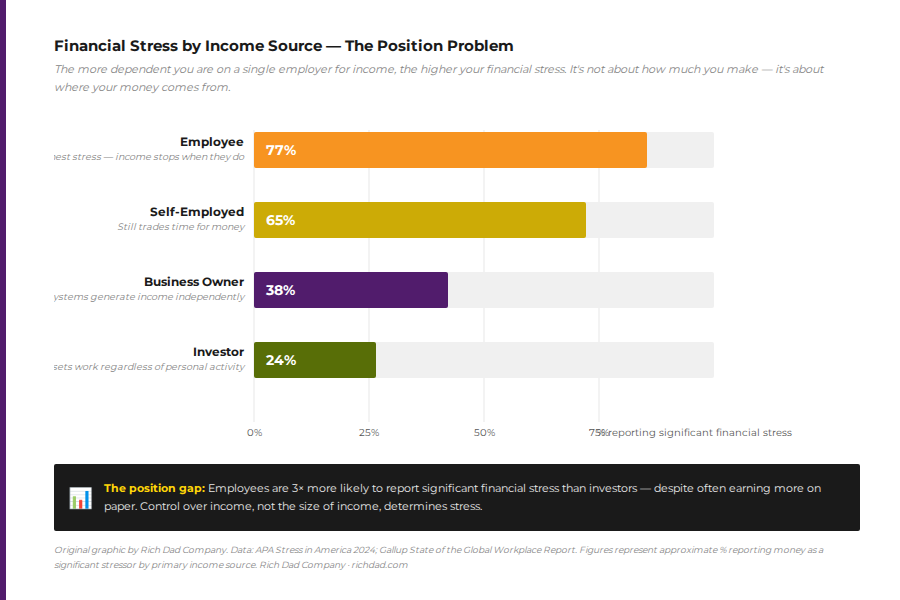

Why most financial plans fail before they start

Ask the average American whether they have a financial plan and most will say yes — a job, a savings account, a 401(k) contribution, maybe some index funds. What they actually have is a collection of financial habits built on advice that was designed for a different economic era. The old rules of money no longer apply, and building a financial plan on top of them is the equivalent of building a house of straw.

The data paints a stark picture. Only one-third of Americans have a documented financial plan, according to the Charles Schwab Modern Wealth Survey. More alarming: the majority of those who do have a plan define financial success as “not living paycheck to paycheck” — a bar so low it would have been unthinkable to prior generations. Meanwhile, median emergency savings for U.S. adults sits at just $500, according to Empower’s 2024 Emergency Savings Study — less than one week of average household expenses.

The underlying problem is not discipline or income. The problem is the financial education, or more precisely, the lack of it. Most people have been taught that working hard, spending carefully, and trusting Wall Street with retirement savings constitutes a financial plan. In reality, this does not. It is a plan to survive, not a plan to build wealth.

A financial plan built on assets, not opinions

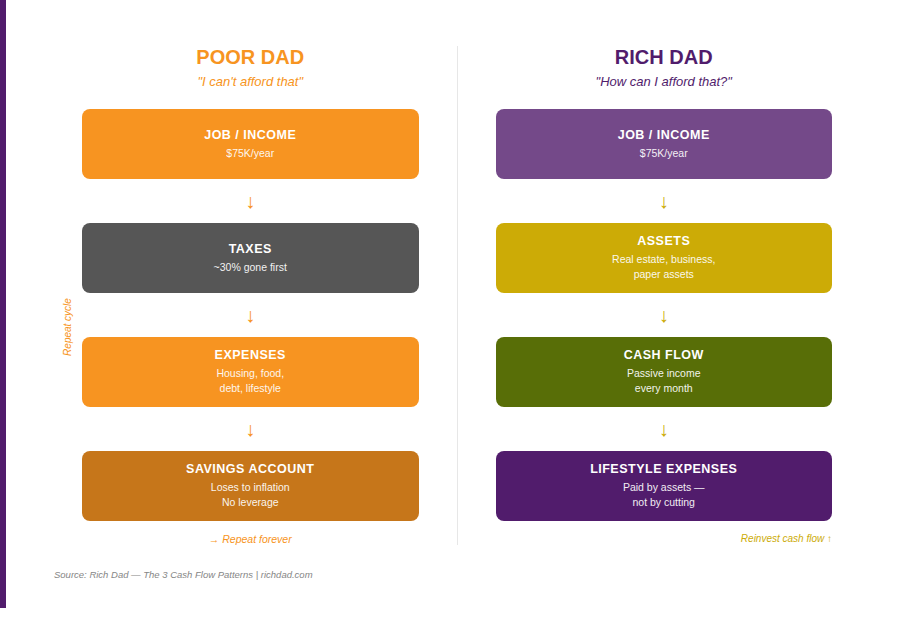

Robert Kiyosaki often contrasts two financial philosophies: poor dad’s and rich dad’s. Poor dad’s plan looked like this — earn a salary, pay taxes, pay expenses, and whatever is left goes into a savings account that quietly loses ground to inflation. Rich dad’s plan reversed the order. Income flows into assets first. Those assets generate cash flow. That cash flow covers lifestyle expenses. The difference between the two is not the size of the paycheck — it is the destination of every dollar that comes in.

Rich dad’s financial plan also draws a fundamental distinction between an asset and a liability. An asset puts money into a pocket. A liability takes money out of a pocket. A primary residence, by this definition, is a liability — it generates no monthly income and costs money every month in mortgage interest, taxes, insurance, and maintenance. This is not a popular point, but it is a financially accurate one, and it is the foundation on which a real financial plan must be built.

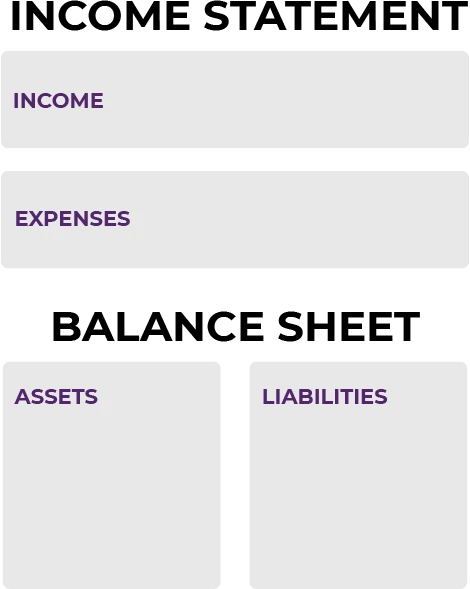

Step 1–Know where you actually stand: The personal financial statement

No financial plan can be built without an honest starting point. A tool for establishing that starting point is the personal financial statement — a two-part document that captures the complete picture of a financial life.

The first part is the income statement. It records all income flowing in — salary, rental income, dividends, business distributions — and all expenses flowing out. This is not a budget projection. It is a factual accounting of what actually happened last month. The second part is the balance sheet — a list of every asset owned and every liability owed.

The exercise is rarely comfortable. Most people discover their expense column is larger than they imagined, their liability column longer than they remembered, and their asset column considerably shorter than it should be. That discomfort is valuable. It is the first honest data a financial plan has to work with.

A detailed walkthrough and template are available at richdad.com/personal-financial-statement.

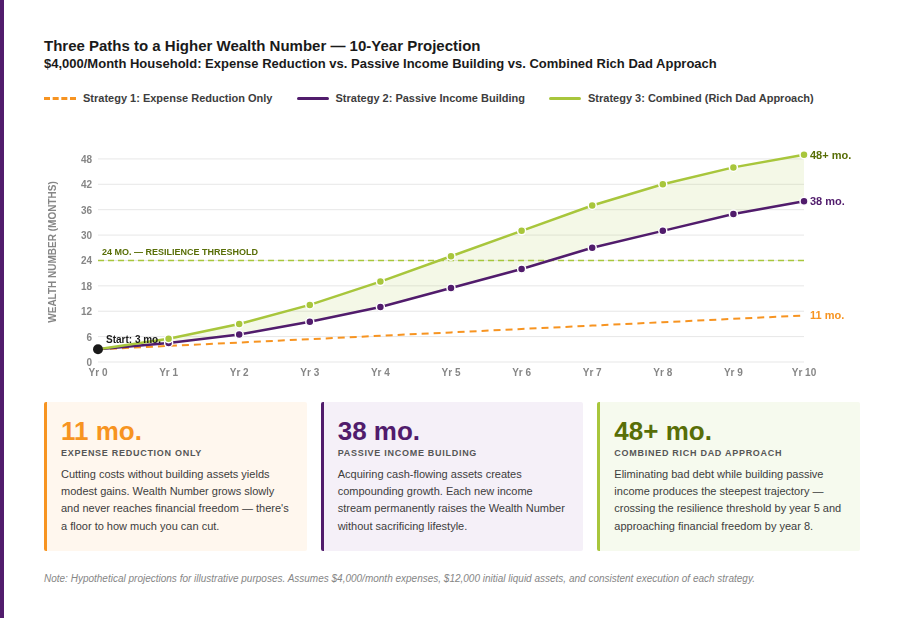

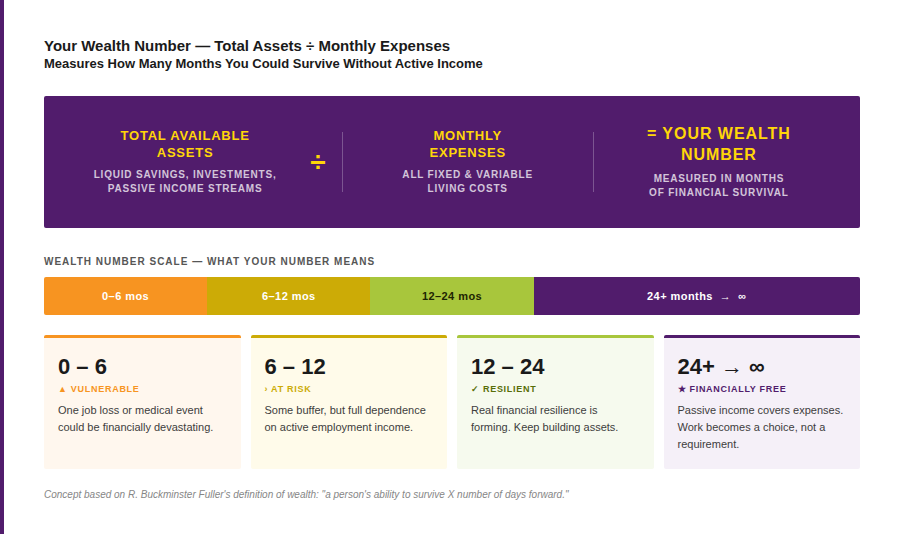

Step 2–Calculate the wealth number

Most people measure financial progress in net worth — the market value of accumulated assets minus debts. But the wealth number answers a more revealing question: if income stopped today, how many months could this household survive without changing its lifestyle?

The Wealth Number reframes the objective of a financial plan. The goal is not simply to accumulate a larger number on a brokerage statement — it is to build enough cash-flowing assets that passive income exceeds monthly expenses. At that crossover point, work becomes optional.

Step 3–Choose between cash flow and capital gains

Every investment falls into one of two categories: it either pays regularly (cash flow) or it pays once when sold (capital gain). Traditional financial planning leans heavily toward capital gains — buy assets, hold them, hope they appreciate, and sell when retirement arrives. Rich Dad’s approach favors cash flow — assets that deposit income into a bank account every month, whether the investor is working or not.

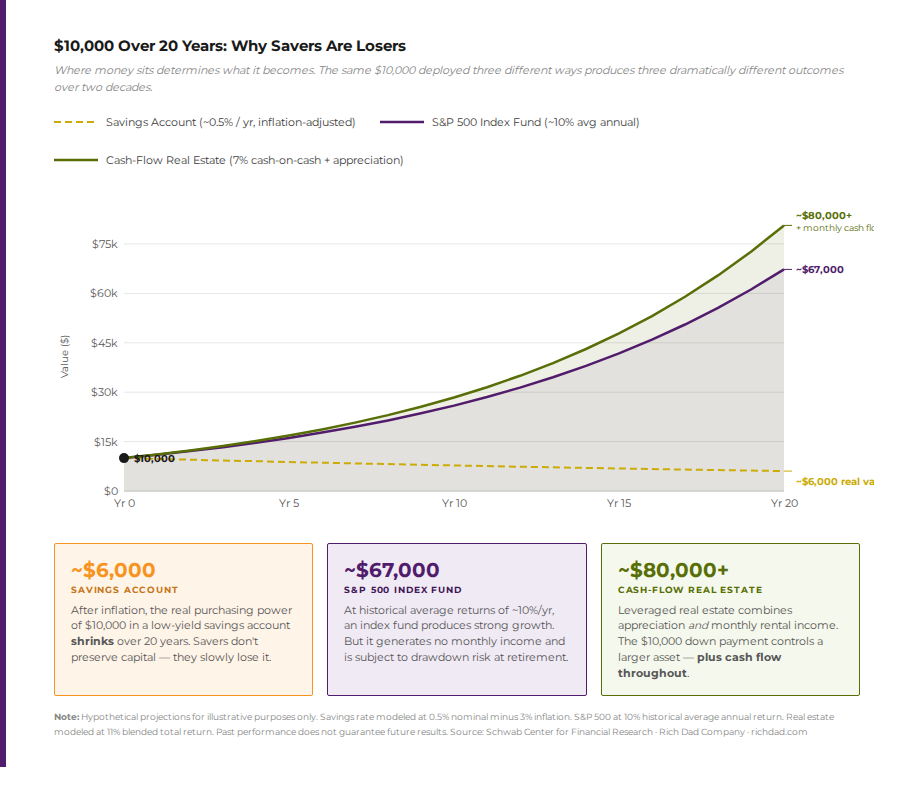

The distinction matters enormously in practice. A $500,000 retirement account invested in index funds generates no monthly income until shares are sold. A portfolio of rental properties, dividend-paying securities, or business systems generates monthly income that does not require selling anything — and therefore does not require timing the market.

The conventional advice to save more money, meanwhile, works against people in a world of persistent inflation. Every dollar sitting in a savings account earning less than the inflation rate is a dollar that is quietly losing purchasing power. Savers are losers — not because saving is wrong, but because parking money in low-yield savings accounts while inflation runs hotter is a losing strategy.

Step 4–Select the right investment vehicles

There are five broad asset classes, each with its own cash flow potential, risk profile, and tax treatment. A well-structured financial plan typically draws from more than one. The five classes are explored in depth at richdad.com/investing:

Step 5–Invest in the right kind of education

The most important asset anyone can acquire is financial education. There are three types of education relevant to a financial plan:

- Academic education — teaches reading, writing, math, and specialized disciplines. Essential for professional competence, but does not teach how money works.

- Professional education — trains specialists: doctors, lawyers, engineers. Generates high earned income, but not the financial intelligence required to manage or grow that income.

- Financial education — teaches how money flows, how assets are valued, how taxes work for and against different income types, and how to evaluate investments. This is what the other two types of education do not provide — and what a real financial plan requires.

Financial education does not come from school. It comes from reading, listening, mentorship, and doing. Robert Kiyosaki’s CASHFLOW board game was designed to teach investing mechanics through play — it can be played for free online. Rich Dad’s podcast library covers real estate, paper assets, entrepreneurship, and tax strategy across hundreds of episodes. Online courses, books, and mentorship circles each accelerate the process.

Step 6–Build the emotional intelligence to execute

Robert Kiyosaki has long argued that financial intelligence is 90% emotional and 10% technical. The technical knowledge of how to evaluate a rental property or structure an options trade can be learned in weeks. The emotional discipline to act on that knowledge — to make an offer, to commit capital, to hold through volatility — takes far longer to develop.

The three most common emotional barriers to executing a financial plan are fear, conditioning, and impatience. Fear of losing money keeps people in low-yield savings accounts long after they have the knowledge to invest. Social conditioning — the cultural belief that a stable job and a 401(k) is a sufficient financial strategy — keeps people from exploring alternatives. Impatience pushes people toward speculation rather than the slower, more reliable accumulation of cash-flowing assets.

Rich Dad’s framework for developing emotional intelligence includes financial education (which reduces fear by replacing the unknown with knowledge), games and simulations (which build decision-making muscle in low-stakes environments), and community (mentors and peers who normalize the path to financial independence). The CASHFLOW Quadrant provides a map: most people start on the left side (E and S) and the goal is to move to the right side (B and I), where income is generated by systems and assets rather than by labor.

Why tax strategy is inseparable from financial planning

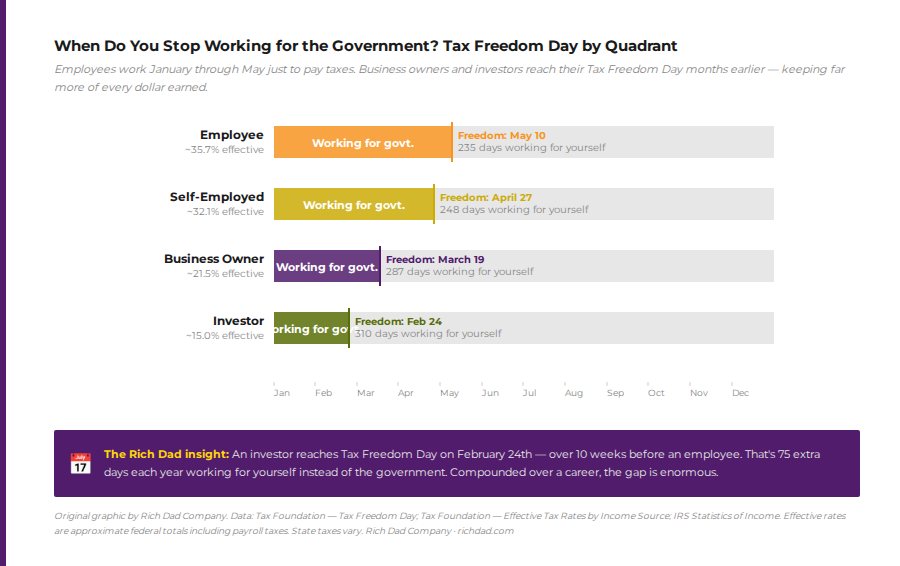

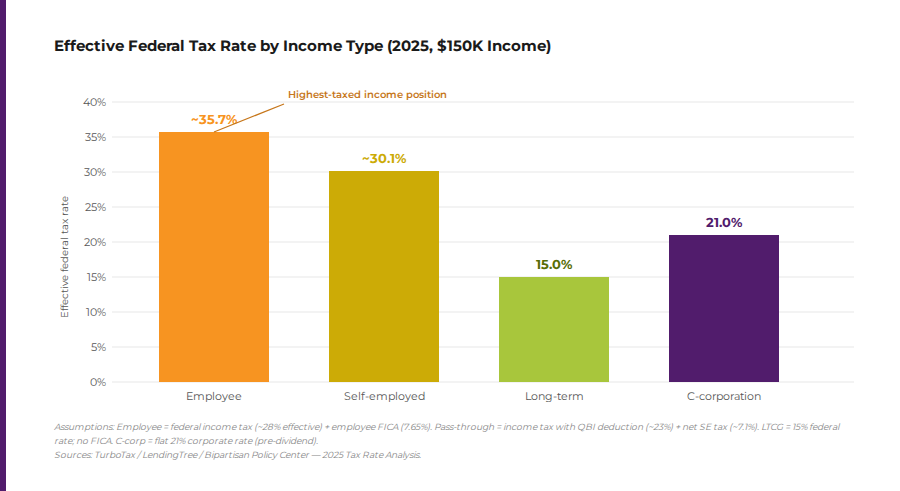

No financial plan is complete without understanding how income is taxed. The tax code treats different income types dramatically differently. An employee earning $150,000 in wages pays an effective federal tax rate of approximately 35.7% — including payroll taxes — before spending a single dollar. A sophisticated investor generating $150,000 in passive income from real estate may pay near 0%, after depreciation, deductions, and passive loss rules are applied.

Here’s a three-word tax strategy: invest, deduct, protect. Invest income into cash-flowing assets before paying taxes. Use the deductions those assets generate to reduce taxable income. Structure entities — LLCs, corporations, trusts — to protect accumulated wealth. Business owners operate in a pre-tax environment. Employees do not. This difference, compounded across decades, is one of the largest single drivers of wealth inequality.

Building a financial team — The asset most people ignore

Robert Kiyosaki has consistently taught that the rich do not do their taxes — they hire people to do them. No high-performing investor manages everything alone. A strong financial plan eventually requires a team: a CPA who specializes in real estate or business taxation, a real estate attorney, a financial mentor, and ideally a community of other investors operating in the same asset classes.

Building that team is itself a form of financial education. Each qualified advisor who joins the team brings domain expertise that a single individual could not replicate in a lifetime of self-study. The cost of that team — accountants, attorneys, advisors — is an investment in the financial plan, not a drain on it. The tax savings and deal quality that result from professional guidance typically far exceed the fees paid.

Rich Dad’s advisor network, available through richdad.com/podcasts, includes specialists in real estate, paper assets, business formation, and tax strategy — each bringing a distinct piece of the financial planning puzzle.

The six-step Rich Dad financial plan: A summary

Old advice no longer works

The financial advice most Americans receive is built for a world that no longer exists. Save more, contribute to a 401(k), diversify across mutual funds — and then hope the market performs well enough to last through retirement. This plan may have worked in a different era. In today’s environment of persistent inflation, rising tax burdens, and an economy that has eliminated the job security previous generations relied on, it is a plan that leaves most people financially exposed when the next economic disruption arrives.

This approach to financial planning is fundamentally different because its goal is fundamentally different. The objective is not to accumulate a retirement balance large enough to draw down before death. The objective is to build cash-flowing assets that generate income whether the owner works or not — income that covers monthly expenses, grows over time, and is protected from taxes through legal strategy.

The six steps outlined above do not require perfection, a high income, or a large starting balance. They require honesty, commitment to financial education, and the willingness to build something that conventional wisdom does not teach. Those who build a financial plan on this foundation will be prepared when the next big, bad wolf arrives — and it always arrives. Those who do not will be left rebuilding from scratch.

The best time to build a financial house of bricks was yesterday. The second-best time is now. Start with an honest personal financial statement, calculate the Wealth Number, and explore Rich Dad’s free financial education resources — including tools, courses, and the CASHFLOW game — at richdad.com.

FAQs

A financial plan is a structured roadmap that maps current financial reality — income, expenses, assets, liabilities — to a future financial goal. It matters because without a plan, spending and investment decisions are made reactively rather than strategically. Most people confuse a budget with a financial plan, however, while a budget manages expenses, a financial plan builds assets.

Start with a personal financial statement — an honest accounting of income, expenses, assets, and liabilities — to establish a baseline. Then calculate the Wealth Number (total assets divided by monthly expenses) to understand the current starting point. From there, choose one asset class to begin learning: real estate, paper assets, business, or commodities. Education precedes investment. Rich Dad’s free resources, CASHFLOW game, and podcast library are purpose-built starting points.

A budget tracks where money goes. A financial plan determines where money should go to build long-term wealth. Budgets focus on restricting expenses. Financial plans focus on expanding income — specifically passive income from cash-flowing assets. Cutting expenses has a floor (zero), while expanding income through asset acquisition has no ceiling.

Conventional financial planning prioritizes saving, index fund accumulation, and 401(k) contributions — all oriented toward a capital gains exit strategy at retirement. Rich Dad’s approach prioritizes cash flow over capital gains, passive income over earned income, and financial education over blind delegation to advisors. The Rich Dad framework also treats tax strategy as a core component of financial planning rather than an annual afterthought.

The Wealth Number is total available assets divided by monthly expenses — expressed in months of financial survival without active income. A Wealth Number of 3 means the household would be financially devastated within three months of a job loss. A Wealth Number of infinity means passive income permanently covers expenses and work is optional. The Wealth Number becomes the benchmark a financial plan works to improve over time.

It is valuable to have physical gold and silver as core holdings in a diversified financial plan — not as speculative positions but as stores of value and inflation hedges outside the banking system. Rich Dad specifically favors physical ownership over paper proxies such as gold ETFs, which introduce counterparty risk. The allocation size depends on individual circumstances and overall portfolio construction.

Review the personal financial statement monthly — income, expenses, assets, and liabilities shift as investments are acquired and financial habits change. The broader strategic review of goals, investment allocation, and tax strategy should happen at minimum annually, and immediately following any significant life or economic event: a major income change, a market disruption, a new investment, or a change in tax law.