Is real estate the right investment for you?

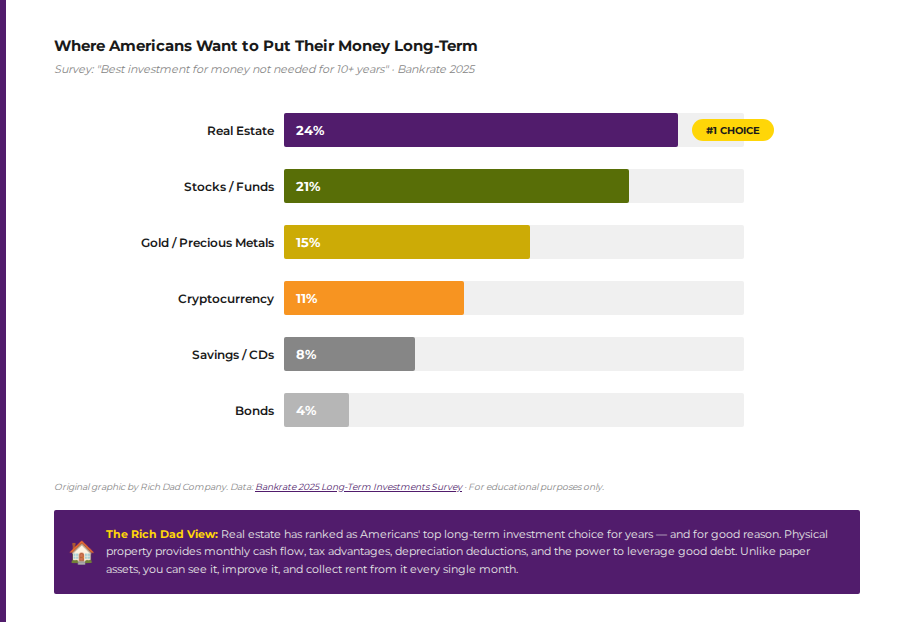

Of all the main asset types—paper assets, commodities, business ventures, cryptocurrency, and real estate—real estate has long been Americans’ top choice for long-term investing. According to a Bankrate 2025 survey, 24% of Americans cite real estate as the best investment for money not needed for at least ten years. That consensus reflects something real: property provides cash flow, tax advantages, leverage, and tangible control that most paper assets cannot replicate. But it is not a universal fit. Understanding the full picture—advantages and demands—is the first step toward choosing a strategy with confidence.

How real estate builds wealth

- Other people’s money (OPM)

In most real estate transactions, the majority of the purchase price is financed through a bank. The investor’s own capital represents a fraction of the total asset controlled—a degree of leverage unavailable in virtually any other investment class. Learn how OPM works. - Monthly cash flow

A rental property purchased and managed correctly can generate reliable monthly income that flows regardless of whether the investor shows up to work. That is a foundational distinction: money working for the investor, not the investor working for money. - Appreciation as a bonus, not a plan

While the Rich Dad philosophy does not treat appreciation as a reliable investment thesis, rising rents and increasing property values do provide supplementary upside over long holding periods. - Investor control

Unlike stocks, real estate investors can directly influence their returns—through property selection, improvements, tenant screening, refinancing, and expense management. Control reduces risk for the educated investor. - Tax advantages

Depreciation, mortgage interest deductions, 1031 exchanges, and passive loss rules are among the most powerful legal tax reduction tools available to investors. Employees have virtually none of these. - Comprehensibility

Unlike derivatives or options chains, real estate fundamentals—rent, expenses, cash flow—are legible to anyone willing to learn the numbers.

What real estate investing actually demands

- Due diligence

More than most asset classes, real estate requires upfront research: market analysis, property inspection, financial underwriting, and legal review before a single dollar is committed. Read the full pros and cons. - Illiquidity

Real estate is not a liquid asset. Getting into or out of a position can take weeks, months, or longer—a critical constraint for investors who may need rapid access to capital. - Active management

Even so-called passive rental income requires tenant management, maintenance, and ongoing financial oversight—particularly in the early stages of portfolio building.

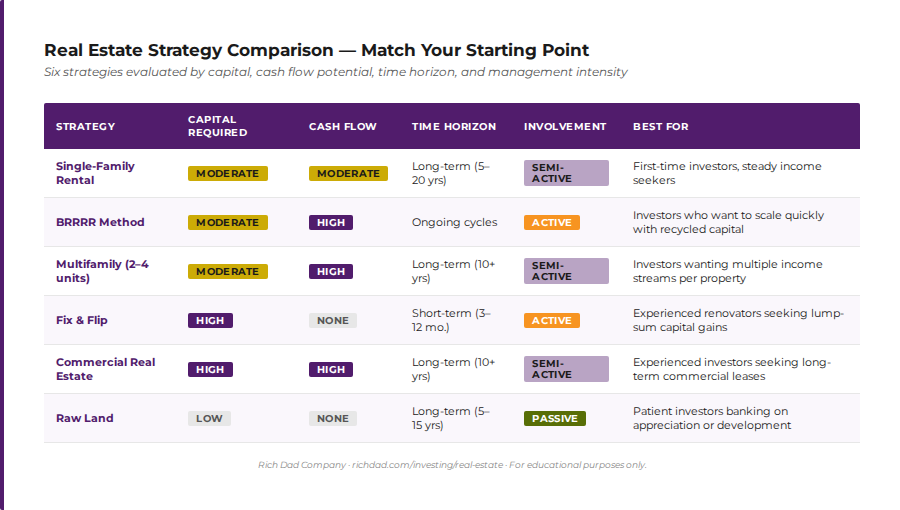

Six real estate investment strategies, compared

There is no single best real estate investment strategy—only the one that best matches an investor’s current capital position, time availability, and financial goals. The six strategies below represent the most common paths through which investors build portfolios. Some prioritize monthly cash flow; others target lump-sum capital gains. Some require deep experience; others are accessible to first-time investors willing to do the work of learning.

1. Single-family rentals — the entry point most investors start with

Single-family rental homes are properties purchased, typically renovated, and then leased to individuals or families. Tenants tend to stay longer than in apartment settings, cash flow is consistent as long as the property is occupied, and the exit market is broad—if an investor chooses to sell, the property appeals to non-investors as well as buyers looking for a home. Single-family homes also tend to hold value well in quality markets.

The critical risk is complete vacancy. When a single-family tenant vacates, cash flow drops to zero immediately. HOA fees and susceptibility to vandalism in extended vacancy periods are additional considerations. For investors building their first rental, a single-family home in a strong rental market—supported by a clear cash flow analysis—remains one of the most accessible starting strategies.

2. The BRRRR method — building a portfolio without starting over

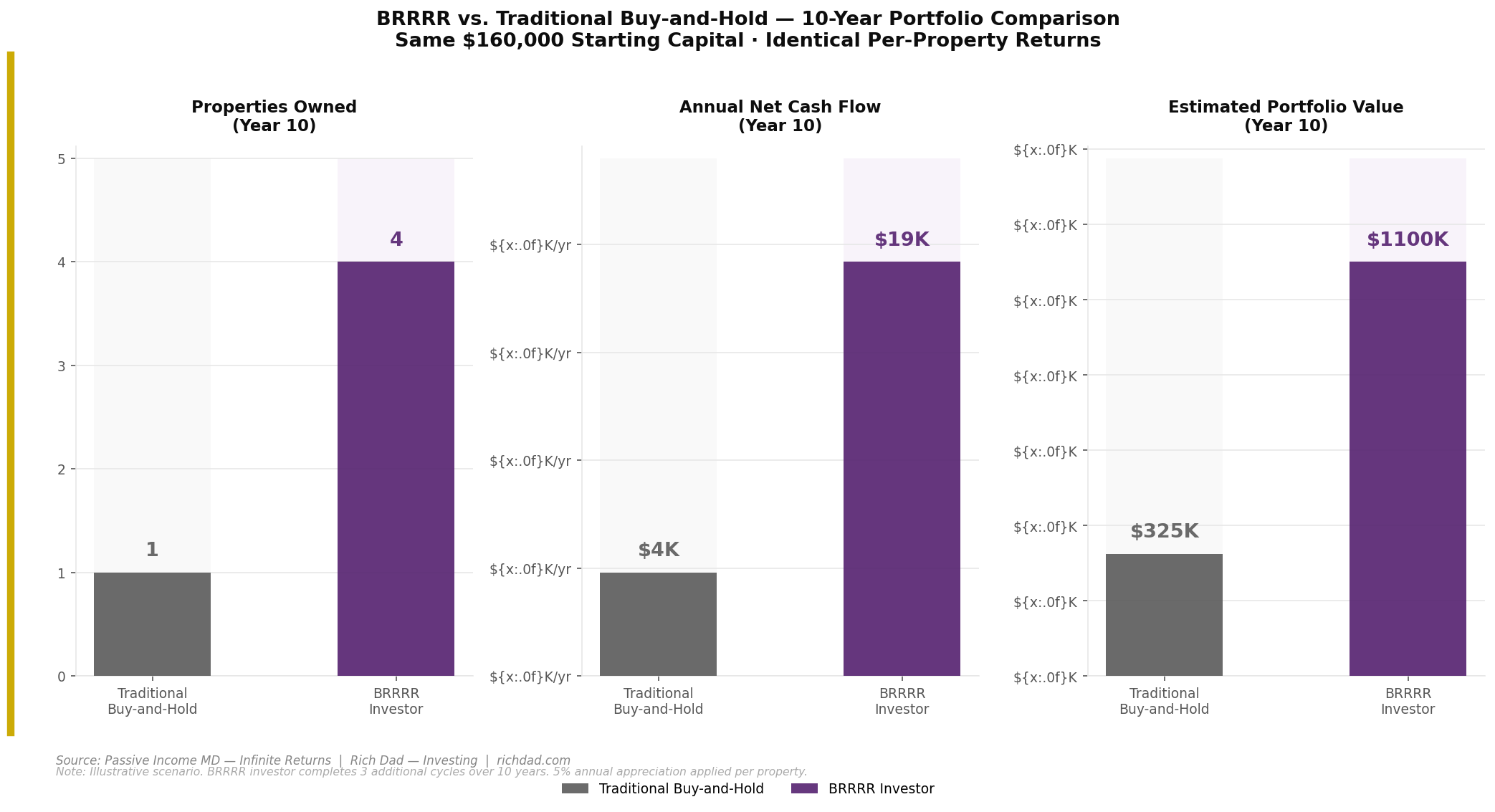

BRRRR stands for Buy, Rehab, Rent, Refinance, Repeat. The strategy involves purchasing a distressed property at a discount, renovating it to increase its appraised value, placing a tenant to generate cash flow, then executing a cash-out refinance to recover the original capital—which is redeployed into the next acquisition. Done correctly, an investor can recycle the same pool of capital across multiple properties, with each property generating ongoing monthly income and no personal capital remaining in the deal.The math is compelling, but the execution is demanding. Renovation cost overruns, appraisal shortfalls, and unfavorable refinance conditions can all prevent full capital recovery. Risk factors include contractor management, accurate after-repair value (ARV) estimation, and mortgage rate environments. BRRRR is best suited to investors with hands-on renovation experience or strong contractor networks. See how infinite returns are calculated.

3. Multifamily properties — more units, more cash flow, more cushion

Duplexes, triplexes, quadruplexes, and small apartment communities give investors multiple income streams from a single acquisition. Vacancy risk is distributed across units—one empty unit does not eliminate cash flow the way a single-family vacancy does. Maintenance costs can also be spread across more doors. Financing for small multifamily properties (under five units) remains accessible through conventional residential loan programs.

Turnover rates in multifamily properties tend to be higher than in single-family homes. Properties with five or more units require commercial financing, which carries more complexity and cost. The management burden also scales with unit count. For investors who want higher cash flow potential and built-in vacancy protection at a moderate entry point, small multifamily is often the next logical step after a first single-family rental.

4. Fix and flip — capital gains without the monthly cash flow

Fix-and-flip investors purchase undervalued or distressed homes, renovate them, and resell for a profit—typically within three to twelve months. The strategy produces lump-sum capital gains rather than ongoing monthly income, which means it functions more like earned income than passive income from a tax standpoint. The faster an investor turns projects, and the larger the margin between purchase-plus-renovation cost and sale price, the higher the return.

This is not a passive strategy. Renovation cost control, contractor management, accurate market timing, and a disciplined buy price—typically no more than 70% of after-repair value minus estimated rehab costs—determine whether a flip generates profit or loss. The Rich Dad philosophy would note: fix-and-flip produces no cash flow and no ongoing asset. Once the property is sold, the income stops. For investors who need capital to seed their rental portfolio, flipping can be a useful tool—but it should not be mistaken for the end goal.

5. Commercial real estate — long leases, higher returns, steeper entry

Commercial properties—office buildings, industrial warehouses, retail centers, and strip malls—operate on fundamentally different economics than residential real estate. Lease terms of five, ten, or fifteen years are common, providing cash flow certainty that residential landlords rarely enjoy. Cap rates on commercial properties frequently run three to six times higher than comparable residential investments. Tenants also tend to have a vested interest in maintaining the appearance of their space, reducing maintenance costs for the investor.

The entry barriers are significant. Purchase prices are higher, financing is more complex, and the management responsibilities—including navigating tenant improvement allowances, CAM reconciliations, and legal liability exposure—require experienced advisors. For investors who have built a residential portfolio and are ready to move up in complexity and return potential, commercial real estate offers a compelling next step. For beginners, it is the wrong starting point.

6. Raw land — the simplest entry, the longest game

Undeveloped land is real estate in its most basic form. It can be purchased and held for appreciation, or acquired with a development plan and built out for sale or rental. Entry prices are often lower than improved properties, competition from other investors is thinner, and day-to-day management demands are minimal. In the right location—near expanding infrastructure, employment hubs, or growing residential zones—land can appreciate substantially over time.

Land investing carries meaningful risks that offset its simplicity. There is no cash flow during the holding period. Zoning ordinances can change, sometimes dramatically affecting land value. Environmental issues—including soil contamination or protected land designations—can emerge unexpectedly and suppress value. Tax advantages are fewer than for improved real estate. Land is best suited to patient investors who have already established cash flow from other sources and are willing to hold for multi-year appreciation cycles.1. Single-family rentals — the entry point most investors start with

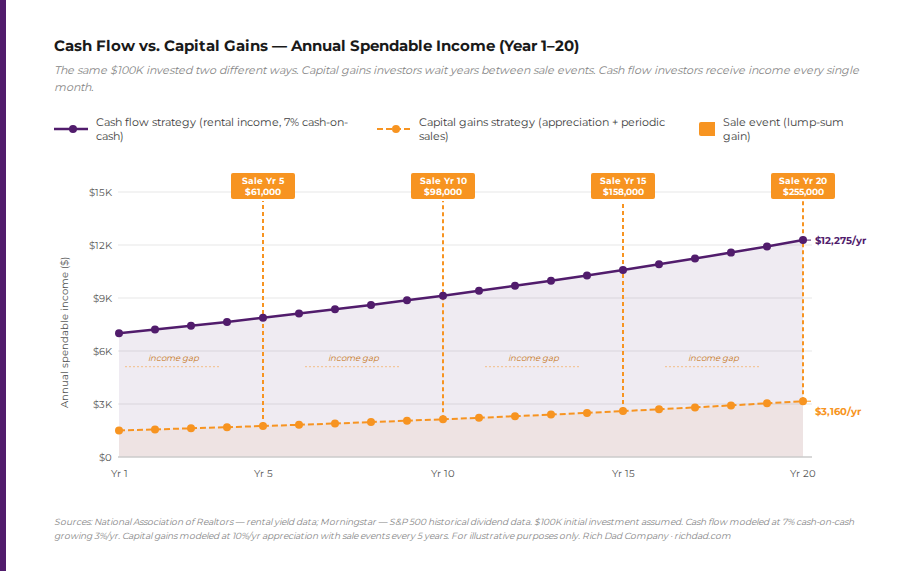

Cash flow vs. appreciation – why to prioritize the former

A persistent misconception in real estate investing is that appreciation—the increase in a property’s market value over time—is the primary wealth-building mechanism. In the Rich Dad framework, appreciation is a bonus, never a plan. A property that produces strong monthly cash flow will build wealth whether or not values rise. A property purchased exclusively for appreciation provides no income during the holding period, ties up capital, and creates a liquidity crisis if values decline or the investor needs cash.

The distinction becomes most visible when comparing cash flow and capital gains side by side over time. Capital gains investors wait years between sale events to realize income—and in the intervals, they collect very little. Cash flow investors receive income every single month, which compounds as it is reinvested into additional assets. It is also worth noting that the tax treatment of passive income is dramatically more favorable than earned income or short-term capital gains, a further argument for prioritizing cash flow strategies.

The formula every cash flow investor needs before writing a check

Every real estate strategy worth pursuing begins with the same evaluation: does the property produce positive monthly cash flow? That calculation is not complicated, but it must be honest. Gross rental income minus all operating expenses—mortgage principal and interest, property taxes, insurance, maintenance reserves, vacancy allowance, and property management fees—equals net monthly cash flow. If the number is negative, the property is not a cash flow investment. It is a liability dressed as an asset.

Robert Kiyosaki’s definition of an asset is simple: something that puts money in your pocket. A property that consumes more each month than it produces is, by that definition, a liability—not an asset. Before evaluating any of the six strategies above, an investor should be able to run this formula accurately and honestly for any property under consideration.

Using other people’s money; why real estate leverage is unique

One of the most powerful advantages of real estate investing—and one that distinguishes it from virtually every other asset class—is the ability to control a large asset with a relatively small amount of personal capital. A 20% down payment controls 100% of a property’s appreciation and cash flow. That leverage, when deployed on a cash-flowing property, means the investor’s effective return on invested capital is multiplied by the ratio of debt to equity.This is what we call using other people’s money (OPM)—a principle that applies not just to bank financing but also to private money, seller financing, and refinancing vehicles like the BRRRR method. The caveat is critical: leverage amplifies losses just as powerfully as gains. An investor who uses maximum leverage without understanding the cash flow math, the local market, and the financing terms is speculating, not investing. Education precedes leverage.

How to align a real estate investment strategy to your goals

Choosing the right real estate investment strategy is not about finding the most sophisticated or the highest-return approach. It is about matching a strategy to the honest reality of where an investor stands today: how much capital is available, how much time can be committed, what experience exists, and what the specific income goal is. An investor who chooses a commercial real estate strategy with no track record and insufficient capital is not being ambitious—they are being underprepared.

It’s important to match strategy to current reality, then building toward more advanced approaches as capital, knowledge, and team capacity grow. For most investors beginning the journey, the sequence is logical: start with a single-family or small multifamily rental to learn the fundamentals, build cash flow, and develop the property management skills and financial discipline that more complex strategies require. Explore real estate cash flow strategies.

A few practical filters for evaluating which strategy fits now:

- Capital available

Fix-and-flip and commercial real estate require significant upfront capital or access to hard money financing. BRRRR and single-family rentals are more accessible entry points. - Time horizon

Short-term capital goals favor fix-and-flip or BRRRR cycling. Long-term wealth accumulation favors buy-and-hold rental strategies and commercial real estate. - Active vs. passive preference

Renovation-based strategies (fix-and-flip, BRRRR) are highly active. Stabilized rental properties can move toward semi-passive with property management in place. Land is the most passive, but also the least income-producing. - Risk tolerance

Complete vacancy risk is highest in single-family. BRRRR carries renovation and refinance risk. Fix-and-flip carries market timing risk. Commercial carries lease-up and credit risk. No strategy is without risk—only educated risk management.

The strategy that works is the one that starts

Every real estate investor who has built meaningful passive income started somewhere. They chose a starting strategy—not the perfect one, but an informed one—and they learned by doing. Robert has emphasized throughout his career that financial education reduces risk. The investor who understands how to calculate cash flow, evaluate a market, underwrite a deal, and manage a property is categorically less exposed than the investor who enters the same market without that foundation.

The six strategies covered here—single-family rentals, BRRRR, multifamily, fix-and-flip, commercial, and land—all work. The question is not which one is best in the abstract. The question is which one is best for this investor, right now, with what they know and what they have. That is the only relevant calculation.

For investors ready to go deeper, richdad.com/investing/real-estate/ provides a full library of resources covering property evaluation, cash flow analysis, tax strategy, and portfolio-building frameworks.

FAQs

Single-family rental homes are generally the most accessible starting strategy for new investors. The financial fundamentals are straightforward, financing is available through conventional lenders, and the exit market is broad. Small multifamily properties (duplexes and triplexes) offer a step up in cash flow potential with manageable added complexity. The most important factor is not the property type—it is the investor’s willingness to learn the cash flow formula, study the local market, and run the numbers honestly before purchasing.

BRRRR stands for Buy, Rehab, Rent, Refinance, Repeat. The strategy involves purchasing a distressed property below market value, renovating it to increase its appraised value, placing a tenant to generate cash flow, and then executing a cash-out refinance to recover the original capital. That capital is then deployed into the next acquisition, allowing an investor to scale a portfolio without continuously injecting new capital. The strategy requires accurate renovation budgeting, a reliable contractor network, and careful attention to refinance conditions.

A primary residence is generally not an investment—it is a liability. A home puts money out of the owner’s pocket every month through mortgage payments, taxes, insurance, and maintenance. It produces no monthly income. Appreciation is not guaranteed and cannot be accessed without either selling or taking on additional debt. This is why your house is not an asset.

Cash flow is the monthly income a property produces after all expenses are paid. Appreciation is the increase in a property’s market value over time. The Rich Dad philosophy prioritizes cash flow because it is measurable, consistent, and taxed at favorable rates. Appreciation is a bonus — it may or may not occur, and it cannot be accessed without selling the property or refinancing. Investors who purchase exclusively for appreciation are speculating on future market conditions, not investing based on current fundamentals.

The required capital depends heavily on the strategy chosen and the local market. Conventional financing for a single-family rental typically requires a 20–25% down payment plus closing costs and a reserve fund. In many markets, that translates to $40,000–$80,000 for an entry-level rental property. BRRRR deals may require similar upfront capital, but the refinance step recovers much of it. Raw land can be acquired for significantly less in certain markets. The critical point: capital without education is the most expensive way to invest in real estate. Financial literacy reduces the cost of every mistake.

Real estate investors have access to some of the most powerful legal tax reduction tools in the U.S. tax code: depreciation (the ability to deduct the paper decline in a property’s value over 27.5 years for residential), mortgage interest deductions, passive loss rules, the 1031 exchange (which allows capital gains to be deferred indefinitely when reinvesting in like-kind properties), and cost segregation for accelerated depreciation. These advantages do not apply to employees. They are available to investors—and represent one of the primary reasons the Rich Dad framework emphasizes moving income from the left side of the CASHFLOW Quadrant to the right.