Blog | Personal Finance

Millennial Money: Saving vs Investing

Attention millennials: The time to start investing is now! Here are three things to get you headed in the right direction.

Rich Dad Personal Finance Team

March 14, 2023

Summary

-

Millennials are saving their money more than investing it.

-

Antiquated advice is proving to be fruitless for millennials and their money.

-

Financial advice can change the direction of millennial money.

When it comes to money and investing, millennials are a different beast than generations that came before them.

Studies show that millennials are saving a bit more than Gen X and baby boomers did, and their attitudes towards investing were heavily shaped by the rapid change of society and technology, coupled with the collapse of trusted institutions as they grew up. As David Brooks recently wrote in “The Atlantic”:

The emerging generations today enjoy none of that sense of security. They grew up in a world in which institutions failed, financial systems collapsed, and families were fragile. Children can now expect to have a lower quality of life than their parents, the pandemic rages, climate change looms, and social media is vicious. Their worldview is predicated on threat, not safety. Thus the values of the Millennial and Gen Z generations that will dominate in the years ahead are the opposite of Boomer values: not liberation, but security; not freedom, but equality; not individualism, but the safety of the collective; not sink-or-swim meritocracy, but promotion on the basis of social justice

(“America is Having a Moral Convulsion”, October 2020)

In a 2020 article by “The Wall Street Journal”, millennials report the following:

-

They feel more financially burdened than their parents and grandparents

-

They are putting off big decisions like buying a home because of uncertainty

-

“More than half of millennials surveyed feel overwhelmed by financial obligations, compared with 39% of Gen Xers and 31% of boomers”

-

“Building up an emergency fund is a focus for 60% of those between the ages of 23 and 38, compared with a little over half of both prior generations”

-

“Mistrust of financial institutions runs through 37% of millennials surveyed, compared with 29% of Generation X and 22% of baby boomers”

-

And perhaps most important…”half of millennials say they want to invest but have no idea where to begin, compared with 32% of Generation X and less than 20% of baby boomers”

(“A Guarded Generation: How Millennials View Money and Investing”, March 2020)

All and all, this adds up to a generation that is on the verge of a $24 trillion wealth transfer from the Baby Boomers to them with no real financial IQ, no plan and even a fear of investing, and a scarcity mindset that tells them they won’t have enough money for emergencies if they do invest.

Saving vs investing millennial money

The old advice to save money has echoed from generation to generation throughout history —and it is still being echoed today. Seeing an uptick in savings is nice, but this saving is not matched by an increase in financial education (of course, if it were, there’d be less saving!).

Unfortunately, the little benefit saving money could have for millennials is erased by the fact that they severely lack true financial education. Here are some reasons why saving money isn’t the best idea:

The (lack of) interest you earn on savings.

Interest rates on savings throughout much of the world are extremely low, almost nonexistent in some parts. Your savings account is actually a loan to your bank. The bank takes the money from your savings account and loans it out to its customers at a much higher interest rate than they pay you. You basically finance your bank’s business for a ridiculously low rate of return on your money.

If you were going to invest your money into a new electric-car start-up company, would you accept a return of 1 percent or less for your investment? Probably not. Yet, that’s what happens when you put your money into your bank’s savings account.

Inflation

Governments who fear that their countries will fall into a depression are printing money to artificially prop up the economy and give the illusion that the economy is stronger than it really is. The problem with this funny money flooding the world, however, is that it will lead to inflation — possibly even high inflation. What does inflation mean in everyday terms? It means that your dollar buys less — your favorite brand of shoes or jeans will cost you many more dollars, euros, yen, or pesos in the future than they do today.

Why would printing money lead to inflation? Here is a simplified explanation: Let’s imagine that there is only $100 in the world. And in this world, there are only five products available. That would mean that, on average, each product would cost $20.

The world government decides to print more money, thus putting more money into the world economy. It prints an additional $900. However, that money does not go to create more products or to grow the economy. It is used to pay off debt and prop up failing banks and businesses. So nothing new is created.

Now, instead of $100 circulating in the economy, there is $1,000. Yet, there are still only five products available. Those five products are no longer valued at $20 each, but are now valued at $200 each. That is how inflation works, and that is the result of the government printing more and more money.

Worthless money

If inflation, especially high inflation, does occur, then it costs you much more to buy the same items you purchase today. Instead of $3 for a loaf of bread, you may be shelling out $12, for example. That dollar, euro, yen, or peso that you saved would then be worth only one-quarter of what it was previously worth.

Another example is what happened in Zimbabwe back in the early 2000s. In 1983, one US dollar was equivalent to one Zimbabwean dollar. Two decades later and it took 669 billion Zimbabwean dollars to equal that same one US dollar.

The problem with saving money is, of course, that as it sits in savings, gaining very little to no interest, it doesn’t grow at the pace of inflation. Your money becomes worth less and less.

By investing, however, you can put your money in assets that hedge against inflation by growing in worth as inflation grows.

Millennial money and saving

Saving money should only be considered as a short term proposition to take you towards your next investment.

How difficult do you think it would be to find an investment that delivered a rate of return better than the 1 percent that your bank’s savings account is earning you? It wouldn't be difficult at all. All it takes is a bit of financial education and a willingness to take a risk — even a small one.

Today, if you’re a millennial whose primary retirement strategy has been to tuck your money away into a savings account, it’s time to start thinking differently.

Below are a few tips to get you started.

Millennial money investing advice #1: Why saving more returns less

One of rich dad’s most important lessons was, “You need to turn a surplus into an expense.”

What does that mean?

Most people consider a surplus of cash as an asset. After they pay for their monthly expenses, they put the remaining money in the bank to later spend it on liabilities.

However, here at Rich Dad we don’t consider that extra cash as an asset. We define an asset as anything that puts money in your pocket regardless of whether you're working or not. Rather than consider the extra cash as an asset, we view it as an expense in the form of charity, investing in cash flowing assets, and savings.

This is what millennials ought to be doing. For every dollar that comes in every month, take 10% and place it into a savings account. Before you do anything else, take an additional 20% and put 10% toward investing in assets and the remaining 10% toward charity. We call it the Pay Yourself First system.

Millennial money investing advice #2: Your financial future is determined with your expense column

Millennials have come to realize that the world doesn’t care about their grades. It cares about their financial report card.

What’s a financial report card?

Simply put, an income statement quickly shows you how your monthly income (paycheck from a job, tips, wages, for examples) compares to your expenses like rent, car payment, insurance, Netflix, phone bill, etc.

To see where you’re going to be in the future, you don’t need to look much further than your expense column.

When you look at most people’s expense columns, you’ll see them littered with payments to banks and credit card companies. In each case, none of those expenses go toward anything that creates money and only things that take money out of your pocket. Those are called liabilities.

Millennial money investing advice #3: Acquire assets that pay for liabilities

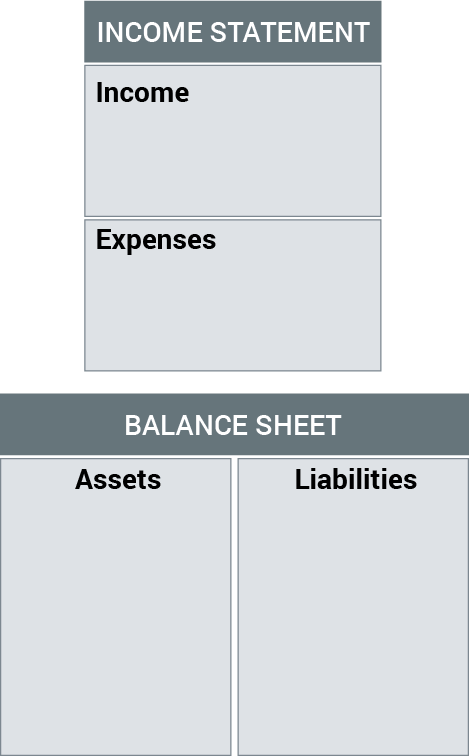

While most budgeting spreadsheets and tools instruct you to list your monthly income and expenses, there’s more to understanding your financial future than that.

Rich dad teaches the other half of the equation which is the balance sheet.

Remember, an asset is anything that puts money in your pocket, regardless of whether you work for it or not. Dividends from a stock, rental income from a real estate investment, or residuals earned from book sales are all different forms of assets.

A liability, however, is anything that takes money out of your pocket. While many people consider their home to be an asset, it’s a liability. Not only do you have the mortgage to eventually pay off, but the property taxes, utilities, and maintenance will always take money out of your pocket.

Here’s the key for millennials to understand: acquire assets that will pay for your liabilities. If you want a new car or a bigger house, acquire a new asset to pay for them. Not only will you have the new car or house, but you’ll have an asset that keeps flowing cash.

Millennial money investing advice #4: Prepare for retirement by spending

When times get tough, most people stop spending on charity, investing, and saving. The rich figure out ways to make more money by spending more money on assets, even when times are tough.

If you must, hire a bookkeeper to hold you accountable. Stick to the Pay Yourself First system as mentioned above to prevent you from straying away and defaulting to old behaviors, like putting money in a savings account.

Millennial money investing advice #4: Perfect the 3 E’s

So how do you become a successful investor?

Rich dad said “The rich get richer partly because they invest differently than others. They invest in things that are not offered to the poor and the middle class. Most importantly, however, they have a different educational background. If you have the right financial education, you will always have plenty of money.”

Rich dad often spoke of a simple formula for investing success that he called the three E’s.

Education

Most people understand reading, writing, and arithmetic. But those who are financially successful also have a different kind of education—financial education.

Financial education is the foundation for building wealth. You know you are financially smarter when you can tell the difference between:

-

Good debt and bad debt

-

Good losses and bad losses

-

Good expenses and bad expenses

-

Tax payments versus tax incentives

-

Corporations you work for versus corporations you own

-

How to build a business, how to fix a business, and how to take a business public

-

The advantages and disadvantages of stocks, bonds, mutual funds, business, real estate, and insurance products, as well as the different legal structures

If you want to learn more about the basics of financial education, read my post, “15 Must Have Financial Education Lessons to Gain True Financial Literacy.”

Experience

A successful investor has a plan, is focused, and plays to win. This doesn’t mean that you won’t fail. Failure is part of the game. What separates the winners from the losers when it comes to investing is the ability to take the experiences, both successes and failures, and to learn from them to get better and better. That is what I mean by experience.

Most people do not learn from their successes and failures. Instead, they jump from one thing to another hoping one will stick. Hot tips don’t make you rich, experience does. And experience is the surest way to build the confidence you need for long-term investing success.

For millennials who want to start investing, this is especially important. If you are like many in your generation who are fearful and have a scarcity mindset, you will never be a successful investor. In order to become a successful investor, you need to try, fail, learn, and do it all over again until you’ve won the game. The best part is this doesn’t require trust in institutions like big banks and Wall Street. It simply requires trust in yourself. And that is the most important trust you can build.

Excess cash

Like the millennials who were surveyed by Twine, when most people hear they need excess cash to be a successful investor, they check out. You’ll often hear them say things like, “I’m living from paycheck to paycheck,” or, “I’ll never have enough money to really invest well.”

The problem is that people hear excessive cash instead of excess cash. Remember, there is nothing wrong with starting small. It is through small investments that are successful that you can grow to larger and larger investments.

Summary

It’s time to abandon the old rules of money. Though placing money aside for emergencies is wise advice for any generation, it shouldn’t be the cornerstone of your retirement planning. Before you start acquiring cash flowing assets, make sure you continue to invest in your greatest asset—your financial education.

Once you understand how to read your personal financial statement and the power between the income statement and balance sheet, you’ll discover a new confidence in your ability to take charge of your financial future, and use your millennial money to your advantage.

Original publish date:

October 09, 2018